Table of Contents

Overview

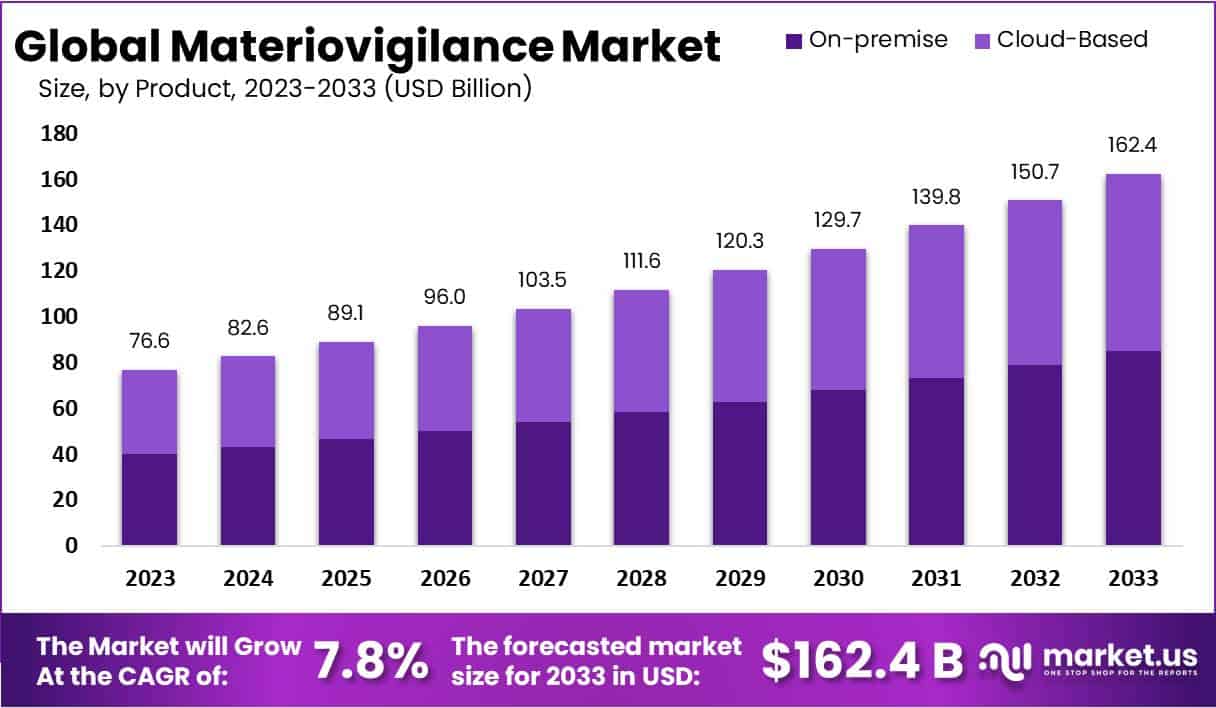

The Global Materiovigilance Market is projected to reach USD 162.4 billion by 2033, growing from USD 76.6 billion in 2023 at a CAGR of 7.8% (2024–2033). The market expansion is driven by stricter international regulations and enhanced post-market surveillance guidance from the World Health Organization (WHO). WHO defines vigilance as a key regulatory function and promotes national reporting systems. These global frameworks strengthen manufacturer accountability and create consistent monitoring practices that drive continuous reporting and data sharing.

In the European Union, materiovigilance is integrated within the Medical Devices Regulation (MDR) and the In Vitro Diagnostic Regulation (IVDR). The European Commission mandates rapid detection and correction of device issues to safeguard patients. Standardized Medical Device Coordination Group (MDCG) guidelines further ensure consistent reporting across the region. Similarly, the United Kingdom’s Medicines and Healthcare products Regulatory Agency (MHRA) has updated its vigilance framework for 2025, reinforcing clarity in incident reporting and expanding data accuracy. These regulatory updates increase investments in surveillance platforms and compliance infrastructure.

In the United States, the Food and Drug Administration (FDA) plays a central role through Medical Device Reporting (MDR) and postmarket surveillance programs. The FDA receives over two million device-related reports annually, reflecting both market scale and data volume. Section 522 surveillance orders encourage the use of real-world evidence, enhancing proactive risk management and data-driven safety evaluation. The rising complexity of device ecosystems further supports the need for robust analytics and systematic vigilance programs across manufacturers.

Emerging markets are also advancing. India’s Materiovigilance Programme (MvPI), led by the Indian Pharmacopoeia Commission, focuses on expanding awareness, training, and structured reporting. Strengthened networks and local vigilance centers are improving incident data collection and corrective actions. Global participation in WHO’s feedback mechanisms encourages international data exchange, enabling lower- and middle-income nations to develop effective vigilance systems and harmonize with global standards.

Digitalization and transparency trends are reshaping materiovigilance. The rise of software as a medical device (SaMD) requires vigilance for cybersecurity, data errors, and usability risks. Regulators emphasize continuous safety monitoring, public communication, and cross-jurisdictional alignment. As manufacturers integrate global post-market systems, demand grows for interoperable platforms, trained personnel, and advanced analytics. Collectively, these factors establish a robust ecosystem that supports safer medical technologies and long-term market growth.

Key Takeaways

- 1. The Materiovigilance Market is projected to expand at a 7.8% CAGR, increasing from US$ 76.6 billion in 2023 to US$ 162.4 billion by 2033.

- 2. On-premise delivery modes led in 2023, securing 52.3% of the market share due to their enhanced reliability and localized control advantages.

- 3. Cloud-based delivery modes followed closely, recognized for offering superior scalability, operational flexibility, and cost-effective integration within healthcare monitoring systems.

- 4. Diagnostic applications dominated with a 32.6% market share in 2023, highlighting growing vigilance toward the safety and performance of diagnostic materials.

- 5. Therapeutic, surgical, and research applications contributed significantly, reflecting broad adoption of materiovigilance practices across multiple medical domains.

- 6. Original Equipment Manufacturers (OEMs) held a commanding 46.8% market share in 2023, driven by their regulatory compliance and product safety responsibilities.

- 7. Contract Research Organizations (CROs) and Business Process Outsourcing (BPO) firms also played pivotal roles, offering specialized materiovigilance and compliance support services.

- 8. Market expansion is primarily driven by stringent regulatory frameworks and a rising number of adverse event reporting cases globally.

- 9. North America led with a 46.2% market share, valued at approximately US$ 35.3 billion in 2023, supported by robust reporting systems.

- 10. Future growth opportunities are expected from increasing cloud-based solution adoption, untapped regional markets, and expanding strategic collaborations in the healthcare sector.

Regional Analysis

In 2023, North America led the global materiovigilance market, capturing a significant 46.2% market share with a valuation of USD 35.3 billion. The region’s leadership was supported by a well-established healthcare infrastructure featuring advanced research institutions and modern medical facilities. This robust foundation enabled effective materiovigilance operations and rapid response to safety concerns. Strong investments in innovation and healthcare modernization further reinforced the region’s dominant market presence and capacity for systematic monitoring of medical materials.

North America’s success was also driven by stringent regulatory frameworks and compliance standards. These regulations ensured the highest levels of product safety and post-market surveillance. The presence of well-defined guidelines from authorities such as the U.S. FDA strengthened market accountability. Consistent oversight and reporting mechanisms fostered trust among manufacturers, healthcare providers, and patients. Such regulatory vigilance encouraged transparency and quality assurance, creating a secure environment for materiovigilance practices across medical and healthcare institutions.

Technological advancement remained a key catalyst in North America’s materiovigilance growth. The adoption of innovative medical devices and materials required constant safety monitoring and risk evaluation. Increasing awareness among healthcare professionals and the public further accelerated incident reporting and data collection. Collaborative efforts among regulatory agencies, hospitals, and industry stakeholders enhanced the region’s overall materiovigilance framework. This cooperative approach ensured proactive risk management, enabling North America to remain at the forefront of global medical safety surveillance.

Segmentation Analysis

In 2023, the Materiovigilance market exhibited strong segmentation by delivery mode. The On-premise mode dominated with a 52.3% share, driven by its reliability and control advantages. Healthcare professionals preferred localized systems that ensured data security and regulatory compliance. Conversely, Cloud-based solutions showed notable growth, supported by flexibility and real-time collaboration. Their scalability and lower costs appealed to organizations pursuing digital transformation. Both modes are expected to evolve further, with Cloud solutions gaining traction while On-premise systems retain preference among data-sensitive users.

The Materiovigilance market’s application segmentation in 2023 highlighted Diagnostic Applications as the leading category, accounting for 32.6% of total market share. This dominance reflected the critical role of diagnostics in ensuring medical material safety and performance. Therapeutic and Surgical Applications also contributed significantly, underscoring the importance of vigilance in diverse medical uses. Additionally, Research Applications demonstrated steady advancement, emphasizing innovation in safe material utilization. Together, these segments reinforced the market’s focus on ensuring the reliability and safety of medical materials across varied domains.

From an end-user perspective, the Original Equipment Manufacturers (OEMs) segment held a major share of 46.8% in 2023, emphasizing its central role in maintaining device safety. Contract Research Organizations (CROs) contributed significantly through robust research and compliance monitoring. The Business Process Outsourcing (BPO) segment also advanced, offering efficiency-driven Materiovigilance solutions. Meanwhile, smaller participants under the “Others” category introduced innovative methodologies. Collectively, these segments shaped a dynamic market structure, highlighting the growing commitment to safety, regulatory adherence, and operational excellence in the Materiovigilance ecosystem.

Key Market Segments

Delivery Mode

- On-premise

- Cloud-Based

Application

- Diagnostic Application

- Therapeutic Application

- Surgical Application

- Research Application

- Others

End Users

- Contract Research Organization

- Business Process Outsourcing

- Original Equipment Manufacturers

- Others

Key Players Analysis

The Materiovigilance Market is shaped by companies that emphasize quality, compliance, and technological advancement. These organizations play a vital role in ensuring patient safety and regulatory adherence through advanced monitoring systems. Among them, AssurX stands out for its robust quality management and compliance solutions. The company focuses on automation and integration, enhancing the traceability of medical devices. Its commitment to continuous innovation and adaptability positions it as a key contributor to improving efficiency and transparency in Materiovigilance operations.

Technological innovation and compliance-driven solutions are central to the Materiovigilance ecosystem. In this context, Sparta Systems plays a significant role through its advanced risk management and quality control platforms. The company’s integrated systems streamline reporting, documentation, and compliance processes for medical device manufacturers. With its emphasis on digital transformation and data accuracy, Sparta Systems enhances regulatory responsiveness and operational consistency. Its solutions are widely adopted, strengthening the overall reliability and regulatory compliance of the global Materiovigilance framework.

Digital transformation and data intelligence have become crucial factors driving market competitiveness. Oracle Corporation exemplifies this trend by offering advanced enterprise technology solutions tailored for Materiovigilance. Its cloud-based infrastructure and AI-powered analytics support real-time monitoring and global compliance management. Oracle’s expertise in system integration enhances efficiency and transparency across data networks. By providing scalable and secure platforms, the company ensures improved coordination among regulatory authorities and manufacturers, strengthening the overall effectiveness of the Materiovigilance ecosystem.

Regulatory compliance and process optimization are also key factors shaping the market. Xybion Corporation has established a strong presence with its specialized compliance software designed for medical device surveillance. The company emphasizes data accuracy, documentation integrity, and adherence to international reporting standards. Its customer-focused approach and ability to tailor solutions to specific regulatory needs enhance its market position. Along with other participants such as Sarjen Systems, MDI Consultants, QVigilance, Qserve, and ZEINCRO, Xybion contributes to a dynamic, collaborative, and innovation-driven Materiovigilance environment.

Market Key Players

- AssurX

- Sparta Systems

- Oracle Corporation

- Xybion Corporation

- Sarjen Systems

- MDI Consultants

- QVigilance

- Qserve

- ZEINCRO

Conclusion

The global materiovigilance market is steadily evolving as medical device safety and regulatory compliance become global priorities. Growth is supported by strong frameworks from agencies such as the WHO, FDA, and the European Commission, which emphasize continuous monitoring and transparent reporting. Digital transformation, data analytics, and cloud adoption are further enhancing vigilance efficiency and global collaboration. As awareness and regulatory stringency rise, manufacturers and research organizations are increasingly investing in advanced surveillance systems. This ongoing integration of technology, compliance, and international cooperation ensures a safer healthcare environment and positions materiovigilance as a cornerstone of modern medical device management.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)