Table of Contents

Overview

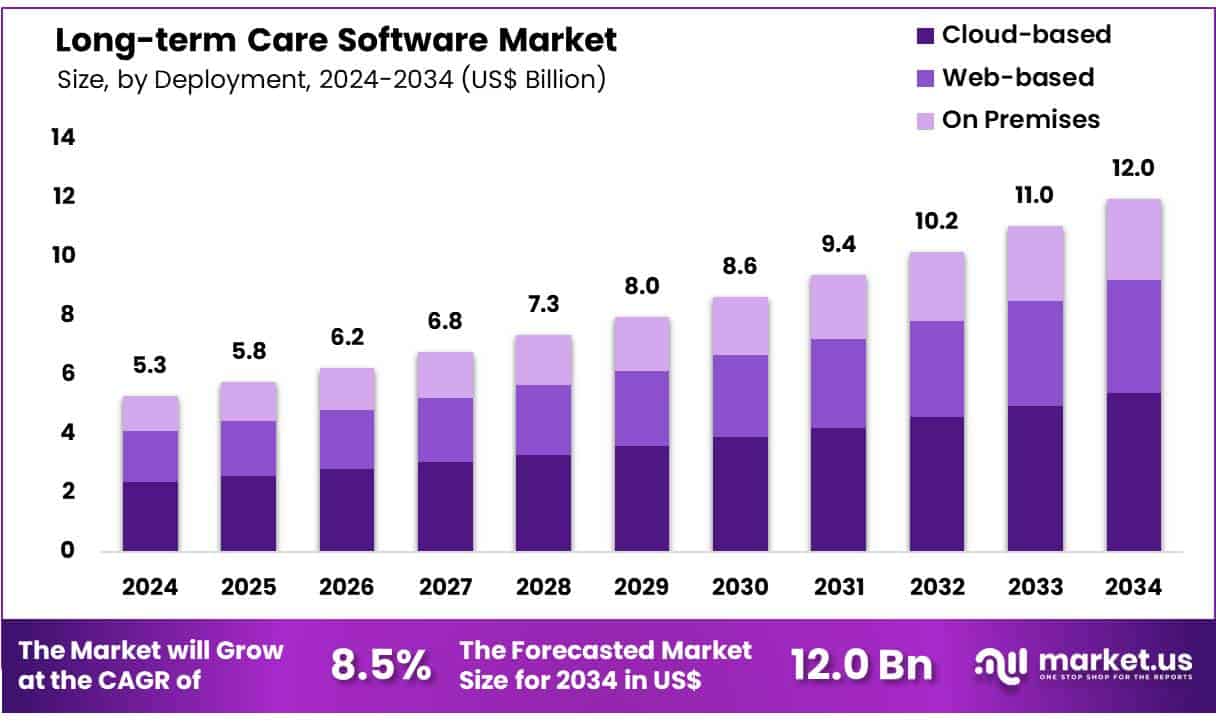

New York, NY – June 24, 2025 – Global Long-term Care Software Market is expected to reach a value of US$ 12.0 Billion by 2034, growing from US$ 5.3 Billion in 2024, with a compound annual growth rate (CAGR) of 8.5% during the forecast period from 2025 to 2034. In 2024, North America led the market, achieving over 52.0% share with a revenue of US$ 2.8 Billion.

The adoption of Long-term Care (LTC) Software is transforming how senior care providers manage operations, compliance, and resident well-being. Designed specifically for skilled nursing facilities, assisted living communities, and continuing care retirement centers, this software automates administrative tasks, streamlines clinical workflows, and ensures regulatory compliance.

The software integrates electronic health records (EHR), billing, care planning, medication management, and staff scheduling into a unified platform. This digitization helps reduce documentation errors, improve care coordination, and ensure accurate reimbursement under CMS guidelines. With cloud-based access and data analytics capabilities, providers can monitor care quality in real time and make informed decisions.

Growing demand for cost-effective eldercare, increasing regulatory oversight, and a shortage of skilled healthcare workers are accelerating the adoption of LTC software solutions. The Centers for Medicare & Medicaid Services (CMS) has also encouraged digitization in long-term care to enhance patient safety and data transparency.

Key Takeaways

- In 2024, the global long-term care software market generated revenue of US$ 5.3 billion and is projected to reach US$ 12.0 billion by 2034, expanding at a compound annual growth rate (CAGR) of 8.5% over the forecast period.

- By Application, Electronic Health Records (EHR) emerged as the leading segment in 2024, accounting for 28.4% of the total market share, driven by the growing emphasis on digital patient records and clinical efficiency.

- By Deployment, the market is categorized into cloud-based, web-based, and on-premises solutions. Among these, cloud-based deployment held a dominant share of 44.9%, reflecting the industry’s shift toward scalable and remotely accessible technologies.

- By End User, the market is segmented into Home Care Agencies, Hospice Care Facilities, Nursing Homes, Assisted Living Facilities, and Others. Home Care Agencies led the segment with a 31.1% share in 2024, supported by the increasing demand for personalized, home-based long-term care.

- By Region, North America maintained a leading position in the global market, capturing a 52.0% share in 2024, attributed to advanced healthcare infrastructure and early adoption of digital health technologies.

Segmentation Analysis

- Application Analysis: In 2024, the Electronic Health Records (EHR) segment held the largest market share at 28.4% in the long-term care software market. EHR systems enhance clinical operations by securely storing patient data, streamlining workflows, and improving regulatory compliance. These solutions offer real-time access, support interoperability, and reduce administrative errors. Despite implementation challenges, such as integration and data privacy concerns, global efforts like Europe’s centralized access and India’s ABDM are reinforcing EHR adoption for improved patient outcomes and care coordination.

- Deployment Analysis: The cloud-based segment led the deployment category with a revenue of US$ 2.4 billion in 2024. This growth is attributed to rising demand for scalable, secure, and cost-efficient healthcare IT solutions. Cloud platforms support real-time data access, regulatory compliance, and seamless EHR integration. Despite concerns around data security and transition costs, cloud solutions are gaining traction, particularly in developing countries. Interoperability innovations such as MEDITECH’s Traverse Exchange Canada demonstrate the growing role of cloud systems in long-term care modernization.

- End User Analysis: Home care agencies emerged as the dominant end-user segment in 2024, capturing 31.1% of the market share. The preference for in-home care, especially among elderly and chronically ill patients, is driving demand for software that enables efficient patient monitoring, record management, and telehealth integration. Cloud-based platforms support personalized care through real-time data and workflow automation. With rising chronic disease prevalence and the need for regulatory compliance, home care agencies are increasingly investing in digital solutions to enhance care quality and operational efficiency.

Market Segments

Application

- Electronic Health Records (EHR)

- Electronic Medication Administration Record (eMAR)

- Revenue Cycle Management (RCM)

- Resident Care

- Staff Management

- Remote Patient Monitoring System

- Clinic Decision Support System

- E-Prescribing

- Real-Time Location System

- Billing, Invoicing, and Scheduling Software

- Others

Deployment Type

- Cloud-based

- Web-based

- On Premises

End-User

- Home Care Agencies

- Hospice Care Facilities

- Nursing Homes

- Assisted Living Facilities

- Others

Regional Analysis

In 2024, North America accounted for 52.0% of the global long-term care software market, driven by a rapidly aging population, high chronic disease burden, and strong demand for digital healthcare solutions.

The U.S., with over 65,000 licensed long-term care facilities, is at the forefront, supported by robust healthcare infrastructure, technological innovation, and favorable regulatory policies. Growing adoption of AI, interoperability, and remote monitoring tools further positions the region for continued expansion and improved patient care outcomes.

Emerging Trends

- Interoperability Enhancement: The exchange of electronic patient data across care settings is being prioritized. However, as of 2017, fewer than 20 percent of nursing homes could share health information electronically with outside providers, underscoring a critical need for more robust interfaces and standardized data formats.

- Cloud-based, Software-as-a-Service (SaaS) Models: Deployment of long-term care solutions in the cloud has been accelerated. This approach is being adopted because it allows for rapid updates, reduced on-site IT overhead, and scalable licensing tied to facility size.

- Artificial Intelligence and Predictive Analytics: Machine-learning modules are increasingly being embedded to forecast risks such as patient falls, pressure ulcer development, and potential hospital readmissions. Early adopters report that predictive alerts can be generated 24–48 hours in advance of clinical deterioration.

- Mobile Point-of-Care Documentation: Tablet and smartphone applications are being rolled out to replace paper charts at the bedside. These mobile tools permit real-time entry of vital signs, care notes, and medication administration, improving timeliness and accuracy of records.

- Integrated Cybersecurity and Compliance: As regulatory scrutiny tightens, new software releases include built-in encryption, role-based access controls, and audit-trail functionality to comply with HIPAA and CMS quality-reporting mandates.

Use Cases

- Automated Quality Reporting: Starting January 1, 2025, skilled nursing facilities will be required to submit quality-measure data on 100 percent of their residents regardless of payer through the CMS Skilled Nursing Facility Quality Reporting Program. This change addresses the fact that 54 percent of Medicare beneficiaries were enrolled in Medicare Advantage plans as of February 2024 and were previously not captured in SNF quality submissions.

- Medication-Error Reduction: Long-term care software with electronic medication administration records and barcode-scanning modules is being used to mitigate prescribing and monitoring errors. Patients on five or more medications have been shown to experience errors at a rate of 30.1 percent over a 12-month period; digitized medication workflows can intercept many of these errors before they reach the patient.

- Telehealth and Remote Monitoring: Integration of telehomecare platforms allows clinicians to monitor vital signs and manage chronic conditions (e.g., heart failure, COPD, diabetes) from afar. Care plans are dynamically adjusted based on threshold alerts, reducing unnecessary clinic visits and enabling early intervention.

- Regulatory Compliance and Audit Support: Software-driven dashboards aggregate data for federal and state surveys, including CMS’s Appendix PP nursing home requirements. Automated flagging of missing documentation and real-time reporting facilitate survey readiness and reduce citation risk.

- Care Coordination Across Settings: Long-term care records are now being exchanged with hospitals, home health agencies, and specialists via standardized ADT (Admission-Discharge-Transfer) messaging. This ensures that care transitions such as post-acute discharge plans are communicated instantly, reducing information gaps and preventing adverse events.

Conclusion

The global long-term care (LTC) software market is undergoing a significant digital transformation, driven by the growing demand for efficient eldercare, regulatory compliance, and workforce optimization. Integration of EHR, cloud-based deployment, AI-driven analytics, and telehealth is streamlining clinical and administrative processes across home care agencies, nursing homes, and assisted living facilities.

With North America leading adoption and CMS regulations pushing for data transparency, the market is poised for steady expansion. Enhanced interoperability, predictive alerts, and automated compliance tools are improving care quality, safety, and operational outcomes. This positions LTC software as a critical enabler of future-ready, patient-centered long-term care.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)