Table of Contents

Overview

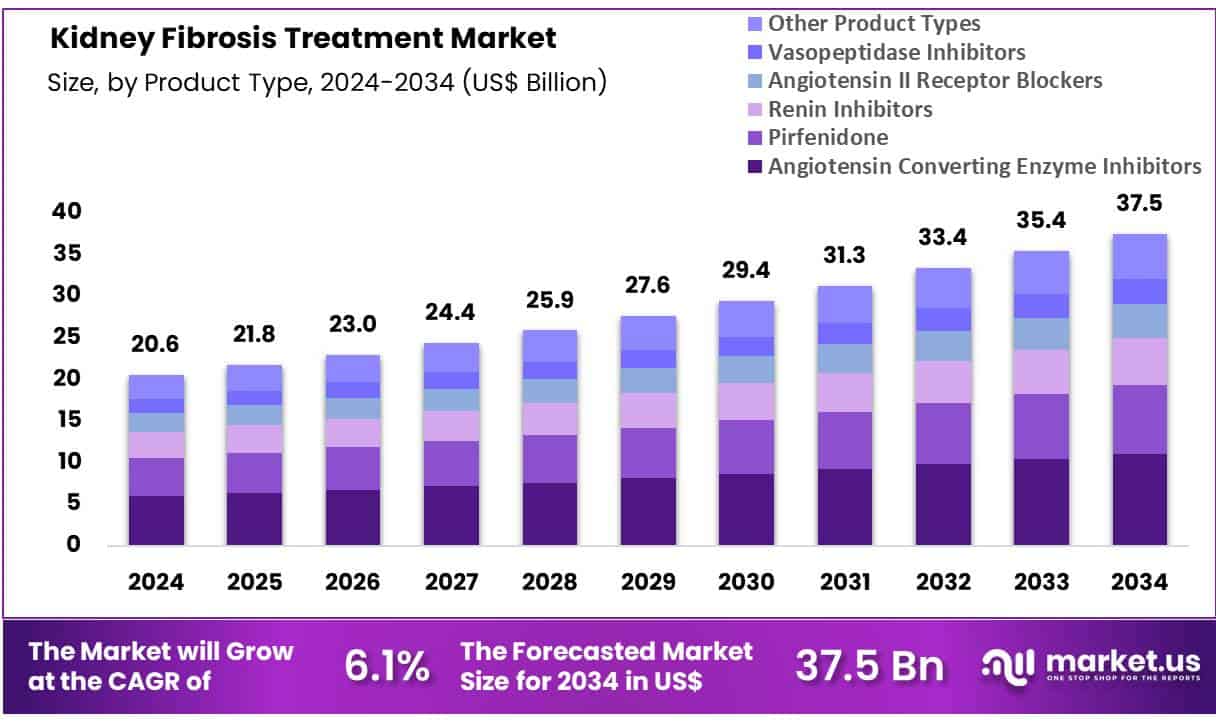

New York, NY – June 09, 2025 – Global Kidney Fibrosis Treatment Market was valued at US$ 20.6 Billion in 2024 and is expected to grow at a CAGR of 6.1% from 2024 to 2034. In 2024, North America led the market, achieving over 36.8% share with a revenue of US$ 7.6 Billion.

The global kidney fibrosis treatment market is witnessing steady growth, driven by the increasing prevalence of chronic kidney disease (CKD) and diabetic nephropathy. Kidney fibrosis, a hallmark of progressive renal failure, results from prolonged inflammation and tissue scarring, leading to irreversible damage. With over 850 million people affected by kidney diseases worldwide, there is a pressing demand for effective antifibrotic therapies.

Recent innovations in molecular targeting have enabled the development of novel agents, including TGF-β inhibitors, CCR2 antagonists, and epigenetic modulators, which show promise in slowing fibrotic progression. Moreover, the rise in clinical trials evaluating the safety and efficacy of these compounds reflects growing R&D investment from biopharmaceutical companies and academic institutions.

North America currently dominates the market due to early diagnosis rates, reimbursement frameworks, and access to advanced biologics. However, Asia-Pacific is expected to exhibit rapid growth, supported by increasing healthcare expenditure and improved screening for CKD-related complications.

Regulatory approvals, such as the FDA’s fast-track designation for promising fibrosis treatments, are accelerating clinical translation. Additionally, patient-centric initiatives by nephrology associations are fostering awareness and encouraging early intervention. As fibrosis continues to challenge renal health globally, the kidney fibrosis treatment market is poised for transformative breakthroughs that aim to delay disease progression and improve quality of life.

Key Takeaways

- In 2024, the global kidney fibrosis treatment market was valued at USD 20.6 billion and is projected to reach approximately USD 37.5 billion by 2034, expanding at a compound annual growth rate (CAGR) of 6.1% during the forecast period.

- The angiotensin converting enzyme (ACE) inhibitors segment emerged as the leading treatment category, accounting for 29.1% of the total market revenue.

- By end-use, the hospitals segment dominated the market, capturing 61.4% of the overall revenue share in 2024.

- Regionally, North America held the largest market share, contributing to over 36.8% of the global revenue, supported by advanced healthcare infrastructure and high adoption of innovative therapies.

Segmentation Analysis

- Product Type Analysis: Angiotensin-converting enzyme (ACE) inhibitors play a critical role in kidney fibrosis treatment due to their proven antifibrotic effects. These agents slow disease progression in conditions like diabetic nephropathy by reducing mesenchymal transformation and boosting antifibrotic microRNAs. Research, including murine models cited in Nephrology Dialysis Transplantation, confirms nephroprotective effects, with ramipril outperforming candesartan in reducing fibrotic markers such as TGF-β and CTGF. ACE inhibitors remain central in preserving renal function and improving patient outcomes.

- End-User Analysis: In 2024, hospitals held a dominant 61.4% share of the global kidney fibrosis treatment market. Hospitals are preferred for managing complex cases, offering access to nephrologists, surgeons, and advanced diagnostic tools like MRI and CT scanners. Their role extends to dialysis, transplant readiness, and acute care services. Additionally, hospitals often act as research hubs, supporting clinical trials and innovation in renal therapies. This comprehensive care model makes hospitals the cornerstone of kidney fibrosis management.

Market Segments

Product Type

- Angiotensin Converting Enzyme Inhibitors

- Pirfenidone

- Renin Inhibitors

- Angiotensin II Receptor Blockers

- Vasopeptidase Inhibitors

- Other Product Types

End-User

- Hospitals

- Clinics

- Home Based Treatment

Regional Analysis

North America continues to lead the global kidney fibrosis treatment market, supported by its advanced healthcare infrastructure and robust medical research ecosystem. The region is home to major pharmaceutical firms, academic centers, and clinical research institutions actively developing and testing innovative therapies for renal fibrosis. One such example includes Esbriet (pirfenidone), developed by Genentech, Inc., which is undergoing clinical evaluation for its potential use in kidney fibrosis treatment beyond its current indication in idiopathic pulmonary fibrosis.

The high prevalence of underlying conditions such as diabetes and hypertension significantly contributes to the region’s disease burden. According to the U.S. Centers for Disease Control and Prevention (CDC), over 1.4 million new cases of diabetes were diagnosed in adults aged 18 and older in 2019. Additionally, more than 130 million adults in the United States are living with diabetes or prediabetes, further increasing the risk of chronic kidney disease and fibrosis.

The growing aging population in North America also plays a key role in disease prevalence, as renal fibrosis is more common in older adults. These factors collectively fuel demand for advanced kidney fibrosis therapies, reinforcing North America’s dominant position in the global market.

Emerging Trends

- Repurposing of Diabetes Drugs: Medications originally approved for diabetes such as SGLT2 inhibitors (e.g., empagliflozin, dapagliflozin) and GLP-1 receptor agonists (e.g., semaglutide) are now being studied for their ability to slow kidney scarring. These agents improve kidney blood flow and reduce harmful pressure inside small filtering units, which may delay fibrosis progression.

- RNA-Targeted Therapies: Small non-coding RNAs, particularly microRNAs (miRNAs), have been identified as key regulators of fibrotic pathways. Therapies designed to block or mimic specific miRNAs are in development to interrupt signaling that leads to scar tissue formation in the kidney.

- Extracellular Vesicle Approaches: Tiny particles released by cells called extracellular vesicles—are being explored as natural delivery systems for anti-fibrotic molecules. Early studies suggest these vesicles can carry protective factors to injured kidney cells, reducing inflammation and collagen buildup.

- Oxidative Stress Modulation: Therapies targeting oxidative stress pathways—such as inhibitors of soluble epoxide hydrolase (sEH) and enhancers of cytoglobin expression are emerging. By lowering harmful free radicals and inflammatory signals, these approaches aim to block the cascade that drives fibrotic scarring.

Use Cases

- Renin-Angiotensin System (RAS) Inhibitors

- Drugs: ACE inhibitors (e.g., captopril at 50–100 mg/day; enalapril at 10–20 mg/day) and ARBs (e.g., losartan at 50–100 mg/day; valsartan at 80–160 mg/day).

- Role: First-line therapy to reduce pressure in kidney filtering units and slow fibrosis. Hyperkalemia occurs in up to 5–10% of patients.

- SGLT2 Inhibitors

- Drugs: Empagliflozin (10–25 mg/day), canagliflozin (100–300 mg/day), dapagliflozin (5–10 mg/day).

- Role: Restore normal tubular feedback, reduce protein in urine, and lower progression risk by approximately 30%. Diabetic ketoacidosis is a noted safety concern in about 1–2% of cases.

- GLP-1 Receptor Agonists

- Drugs: Dulaglutide (0.75–1.5 mg/week), semaglutide (0.25–1.0 mg/week), liraglutide (0.6–1.8 mg/day).

- Role: Inhibit fibrotic signaling, promote sodium excretion, and improve kidney blood flow. These agents have demonstrated up to a 15% reduction in markers of fibrosis in early trials.

- Mineralocorticoid Receptor Antagonists (MRAs)

- Drug: Finerenone at 10–20 mg/day.

- Role: Reduce proteinuria and slow decline in glomerular filtration rate, with an observed 18% risk reduction for kidney failure events in clinical studies. Hyperkalemia affects about 10–12% of treated patients.

- DPP-4 Inhibitors

- Drugs: Sitagliptin (100 mg/day), linagliptin (5 mg/day), vildagliptin (100 mg/day).

- Role: Primarily used in diabetes, these agents have shown potential to reduce proteinuria and inflammation, with early trials indicating a 10–15% decrease in fibrosis markers.

Conclusion

The kidney fibrosis treatment market is advancing steadily, driven by a growing burden of chronic kidney disease and diabetes. Innovations in antifibrotic therapies, including targeted agents like ACE inhibitors, SGLT2 inhibitors, and RNA-based treatments, are enhancing disease management. North America’s leadership is supported by strong healthcare infrastructure and early access to novel drugs.

Emerging research on oxidative stress and extracellular vesicles further diversifies the treatment landscape. With increasing clinical trials and regulatory support, the market is positioned for significant growth, offering promising avenues to slow disease progression, improve patient outcomes, and meet the rising global demand for effective renal therapies.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)