Table of Contents

Overview

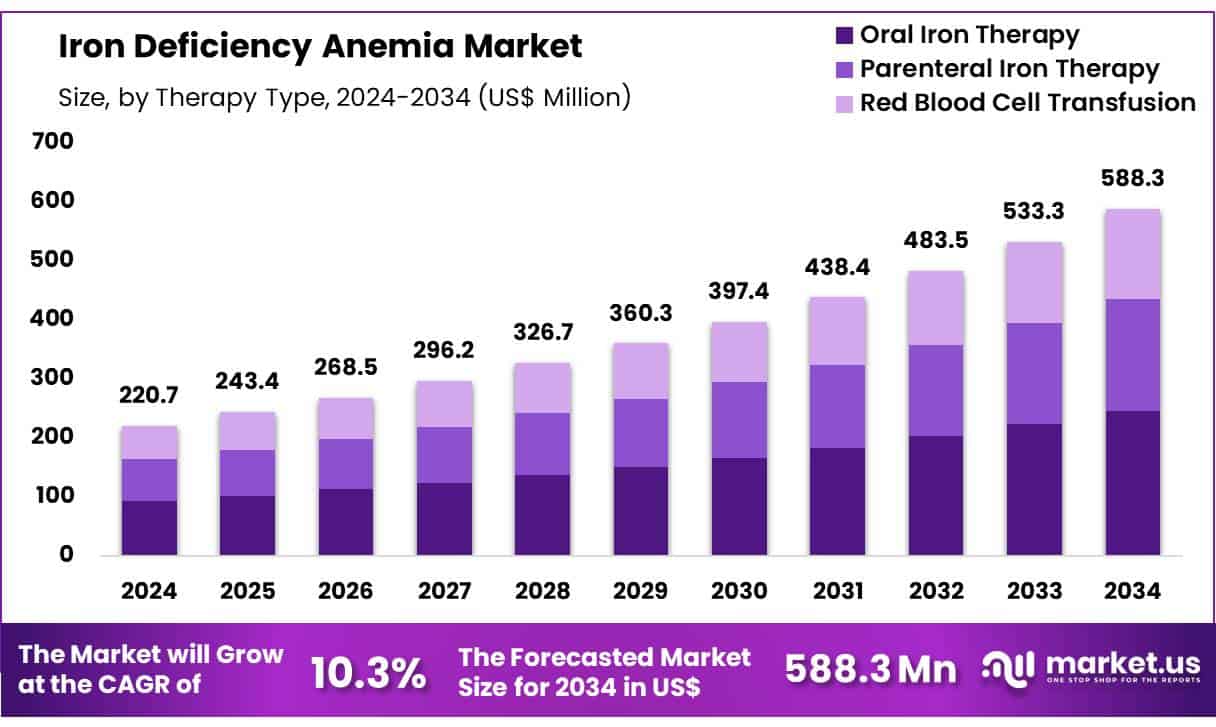

New York, NY – June 06, 2025 – Global Iron Deficiency Anemia Market size is expected to be worth around US$ 588.3 Million by 2034 from US$ 220.7 Million in 2024, growing at a CAGR of 10.3% during the forecast period 2024 to 2034.

Iron Deficiency Anemia (IDA) continues to pose a significant global public health concern, affecting millions, particularly women, children, and individuals with chronic diseases. IDA occurs when the body lacks sufficient iron to produce healthy red blood cells, leading to reduced oxygen transport, fatigue, weakness, and impaired cognitive function. According to the World Health Organization (WHO), over 30% of the global population is anemic, with iron deficiency being the most common cause.

The condition is prevalent in both developing and developed nations, though risk factors differ. In low-income regions, poor dietary intake, parasitic infections, and limited healthcare access are primary contributors. In contrast, blood loss from menstruation, gastrointestinal disorders, and poor iron absorption are more common causes in industrialized countries. Pregnant women, infants, and adolescent girls are particularly vulnerable due to increased iron demands.

Healthcare organizations emphasize early screening, iron-rich diets, and supplementation as critical preventive strategies. Fortification of staple foods and community-level awareness campaigns are being scaled to address the widespread burden. Efforts by the Centers for Disease Control and Prevention (CDC) and WHO aim to reduce anemia rates through coordinated nutritional programs and maternal health initiatives. Iron Deficiency Anemia remains a manageable condition if diagnosed early and treated effectively. Continued public health action is vital to improving outcomes and reducing the global disease burden.

Key Takeaways

- In 2024, the global Iron Deficiency Anemia market generated a revenue of approximately US$ 220.7 million. It is projected to expand at a compound annual growth rate (CAGR) of 10.3%, reaching a value of around US$ 588.3 million by 2034.

- By Therapy Type, the market is segmented into Oral Iron Therapy, Parenteral Iron Therapy, and Red Blood Cell Transfusion. Among these, Oral Iron Therapy dominated the segment in 2024, accounting for a significant market share of 41.9%, due to its cost-effectiveness and ease of administration.

- In terms of Therapy Area, the market is categorized into Obstetrics and Gynecology, Renal Diseases, Congestive Heart Failure (CHF), Oncology, Inflammatory Bowel Disease, and Others. The Obstetrics and Gynecology segment emerged as the leading contributor, holding a notable 27.5% share, driven by the high prevalence of anemia among women of reproductive age and pregnant women.

- By Patient Demographics, the market is divided into Adults, Geriatric, and Pediatric groups. Adults constituted the largest segment, with a 45.9% revenue share, reflecting the growing diagnosis and treatment of iron deficiency among working-age populations.

- Regarding Distribution Channel, the market is split into Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies. Hospital Pharmacies led this segment, capturing 48.9% of the total share, owing to increased inpatient treatment rates.

- By End-User, the market includes Hospitals, Specialty Clinics, Home Care Settings, and Others. Hospitals accounted for the largest share, contributing 38.7%, due to their comprehensive treatment capabilities.

- Regionally, North America held a dominant position in 2023, securing 45.5% of the global market share, driven by advanced healthcare infrastructure and heightened awareness of anemia management.

Segmentation Analysis

- Therapy Type Analysis: In 2024, Oral Iron Therapy led the Iron Deficiency Anemia (IDA) market with a 41.9% share. This dominance is due to its affordability, over-the-counter availability, and ease of use. Widely prescribed for mild to moderate cases, formulations like ferrous sulfate and ferric citrate remain standard. FDA approvals such as oral ferric maltol have boosted the segment further, offering alternatives with fewer side effects and matching the efficacy of intravenous iron without requiring hospital administration.

- Therapy Area Analysis: Obstetrics and Gynecology held a 27.5% share in the IDA market, driven by high anemia prevalence in pregnant and menstruating women. Increased iron demands during pregnancy, childbirth, and menstruation fuel this segment. According to NCBI, anemia was present in over 62% of maternal cases, leading to complications like low birth weight and premature delivery. Government iron supplementation programs are key growth drivers. Renal, oncology, and IBD-related anemia also contribute due to treatment-related iron loss and poor absorption.

- Patient Analysis: The Adults segment led the IDA market with a 45.9% share in 2024. The high burden of anemia among women of reproductive age, pregnant individuals, and patients with chronic conditions such as CKD and IBD drives this dominance. Factors such as poor diet, menstrual blood loss, and iron depletion contribute significantly. The Geriatric population also shows rising demand due to chronic illnesses and reduced absorption, while Pediatric cases are managed primarily through national supplementation and nutrition programs.

- Distribution Channel Analysis: Hospital Pharmacies held the largest market share of 48.9% in the IDA sector, attributed to the high volume of prescriptions for severe anemia requiring advanced care like intravenous iron or transfusions. These facilities also serve complex cases involving CKD and cancer. Retail Pharmacies follow, supporting moderate anemia cases via OTC oral supplements. Online Pharmacies are rapidly expanding due to rising digital access, offering convenience, cost savings, and growing consumer preference for at-home supplement purchasing.

- End-User Analysis: Hospitals were the leading end-users in the IDA market in 2024, holding a 38.7% share. Their dominance is linked to the need for intensive care, parenteral therapy, and blood transfusions in severe anemia cases. They serve as treatment centers for patients with chronic conditions, such as renal failure and cancer-related anemia. Specialty Clinics also contribute significantly, offering focused care in fields like nephrology, oncology, and obstetrics. Home Care settings are emerging, especially for long-term anemia management and oral supplementation.

Market Segments

Therapy Type

- Oral Iron Therapy

- Parenteral Iron Therapy

- Red Blood Cell Transfusion

Therapy Area

- Obstetrics and Gynecology

- Renal Diseases

- Congestive Heart Failure (CHF)

- Oncology

- Inflammatory Bowel Disease

- Others

Patient

- Adults

- Geriatric

- Pediatric

Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

End-User

- Hospitals

- Specialty Clinics

- Home Care Setting

- Others

Regional Analysis

North America holds the leading position in the global Iron Deficiency Anemia (IDA) market, supported by high healthcare expenditure, advanced medical infrastructure, and a rising burden of chronic diseases such as chronic kidney disease (CKD) and cancer. The United States dominates the region, with widespread use of intravenous (IV) iron therapies, increasing awareness, and active pharmaceutical innovation.

Strong regulatory support and product approvals also contribute to market expansion. For example, in June 2023, the U.S. Food and Drug Administration (FDA) approved INJECTAFER (ferric carboxymaltose injection) by Daiichi Sankyo, Inc. and American Regent, Inc., for treating iron deficiency in adult patients with heart failure classified as NYHA class II/III, aimed at improving exercise capacity.

Europe represents the second-largest market for IDA. The region benefits from national healthcare initiatives, iron supplementation programs, and iron fortification in staple foods. Countries such as Germany, the United Kingdom, and France are key contributors to regional growth. Increased demand for IV iron therapy among pregnant women and elderly populations, coupled with well-established clinical guidelines and access to anemia management services, strengthens Europe’s position in the global market.

Emerging Trends

Iron deficiency anemia continues to affect large segments of the population, particularly women of reproductive age and young children. In 2023, 30.7 percent of women aged 15–49 years and 35.5 percent of pregnant women experienced anemia worldwide. It is noted that nearly 39.8 percent of children aged 6–59 months were anemic in 2019. Such high prevalence has prompted governments and health agencies to prioritize iron status monitoring.

Surveillance and data driven tools are being adopted to track iron deficiency anemia more closely. In the United States, efforts to use electronic health records (EHR) for first trimester pregnancy anemia surveillance have been assessed for feasibility. Globally, a WHO Micronutrients Survey Analyser tool has been developed to harmonize hemoglobin and ferritin data for better policy planning. Meanwhile, mortality from iron deficiency anemia among older adults in the U.S. rose from 3.42 to 5.00 deaths per 100,000 population between 1999 and 2019.

Intervention strategies have evolved with a stronger focus on supplementation and dietary approaches. A recent Cochrane Review found that daily iron supplementation of 9–90 mg in pregnant women reduced the risk of anemia at term by 70 percent and iron deficiency by 57 percent. Socioeconomic disparities remain evident: individuals at the highest poverty level had more than double the anemia rates compared with those at the lowest poverty level (females 18.7 percent vs. 8.1 percent; males 8.7 percent vs. 3.5 percent). Daily iron supplementation programs for women and adolescent girls continue to be recommended to reduce iron deficiency without significant side effects.

Use Cases

Clinical screening protocols have been expanded to identify iron deficiency anemia early. In the United States, 9.3 percent of individuals aged two and older were anemic between August 2021 and August 2023, with females (13.0 percent) affected more than males (5.5 percent). Among teenage girls aged 12–19, 17.4 percent were anemic, while women aged 20–59 had a 14.0 percent rate. Guidelines now recommend routine hemoglobin screening during prenatal visits and in primary care, especially for high risk groups.

Public health supplementation programs are widely used to prevent and treat iron deficiency anemia. Daily iron supplementation for pregnant women has been shown to lower low birthweight risk from 10.2 percent to 8.4 percent when compared to no supplementation. In many countries, prenatal care includes iron tablets (60–120 mg per day) with counseling on dietary improvements to ensure adequate iron intake. School based deworming and iron fortified foods are also provided in regions with high anemia burdens.

Digital surveillance and data harmonization tools are used to inform policy and program design. The feasibility of using EHRs for anemia, iron deficiency, and iron deficiency anemia surveillance among first trimester pregnancies has been explored to improve maternal health tracking. Additionally, the WHO Micronutrients Survey Analyser enables standardized analysis of biomarkers (hemoglobin, ferritin, iodine) across populations, supporting national nutrition plans. Such tools aid in identifying regions with the greatest needs and in evaluating program impact over time.

Educational and workplace health initiatives leverage anemia data to address developmental and productivity concerns. Iron deficiency anemia has been linked to poor cognitive and motor development in children and reduced work capacity in adults. As a result, nutrition education for parents and employees often includes information on iron rich foods (e.g., legumes, red meat, leafy greens) and the importance of regular hemoglobin testing. Workplace wellness programs in some areas offer on site hemoglobin checks to facilitate early detection and timely intervention.

Conclusion

Iron Deficiency Anemia (IDA) remains a critical yet preventable global health challenge. It disproportionately affects women, children, and those with chronic illnesses, yet advancements in diagnostics, supplementation, and digital surveillance are enabling better management. Early screening, nutritional interventions, and targeted public health programs especially among high-risk groups are proving effective in reducing prevalence and improving outcomes.

Regional initiatives, such as FDA-approved therapies and WHO monitoring tools, are enhancing treatment access and data-driven policymaking. With continued global collaboration and sustained investment in prevention, IDA can be significantly reduced, improving quality of life and economic productivity worldwide.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)