Table of Contents

Overview

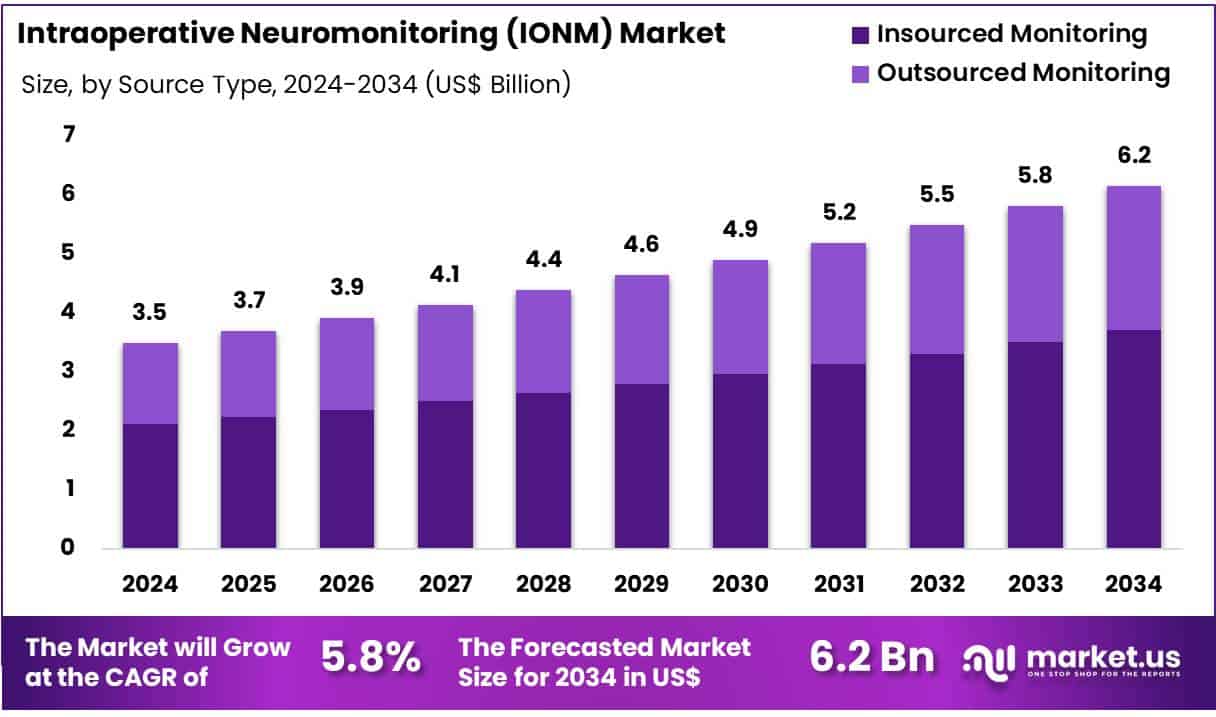

New York, NY – June 30, 2025 – The Global Intraoperative Neuromonitoring (IONM) Market size is expected to be worth around US$ 6.2 Billion by 2034 from US$ 3.5 Billion in 2024, growing at a CAGR of 5.8% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 47.2% share with a revenue of US$ 1.7 Billion.

Intraoperative Neuromonitoring (IONM) is gaining prominence as a vital technology in improving surgical outcomes and patient safety. IONM involves the continuous assessment of the nervous system during complex surgeries, such as spinal, orthopedic, neurosurgical, and vascular procedures. By monitoring neural pathways in real time, IONM enables surgeons to identify and prevent potential nerve damage, thereby reducing the risk of postoperative complications such as paralysis, loss of motor function, and sensory deficits.

The adoption of IONM has expanded significantly due to advancements in monitoring technologies and growing awareness of its clinical value. Techniques such as somatosensory evoked potentials (SSEP), motor evoked potentials (MEP), and electromyography (EMG) are frequently employed to track neural function and support intraoperative decision-making.

Healthcare providers globally are increasingly integrating IONM services to enhance surgical precision and comply with patient safety standards. This growth is supported by rising surgical volumes, increasing prevalence of spine and neurological disorders, and the demand for minimally invasive interventions.

IONM services are delivered by skilled neurophysiologists and technologists in coordination with surgeons and anesthesiologists, ensuring a multidisciplinary approach to surgical care. As technology evolves and the importance of nerve preservation in surgery becomes more evident, IONM is expected to remain a cornerstone in the pursuit of safer and more effective surgical procedures.

Key Takeaways

- In 2024, the global Intraoperative Neuromonitoring (IONM) market was valued at US$ 3.5 billion and is projected to grow at a compound annual growth rate (CAGR) of 5.8%, reaching approximately US$ 6.2 billion by 2033.

- By product type, the market is categorized into systems, services, and accessories. Among these, systems accounted for the largest share, contributing 45.5% of the market revenue in 2023.

- Based on source type, the market is segmented into outsourced monitoring and insourced monitoring. Insourced monitoring dominated the segment, capturing 60.3% of the total market share.

- In terms of application, the IONM market is divided into spinal surgery, orthopedic surgery, neurosurgery, ENT surgery, vascular surgery, and others. Spinal surgery emerged as the leading application, holding a 34.7% share of global revenues.

- The end-user landscape includes hospitals and ambulatory surgical centers, with hospitals maintaining a dominant position, accounting for 69.8% of the market share in 2023.

- Regionally, North America led the global market, contributing 47.2% of the overall revenue share in 2023, driven by advanced healthcare infrastructure, higher surgical volumes, and early adoption of neuromonitoring technologies.

Segmentation Analysis

- Product Type Analysis: The systems segment accounted for 45.5% of the market share in 2023, driven by the rising need for advanced monitoring tools that support surgical precision. These systems offer real-time neural feedback, especially critical in neurosurgery and spinal procedures. Technological advancements such as enhanced signal accuracy and miniaturization, along with integration with robotics and imaging platforms, are expected to boost adoption. As healthcare facilities emphasize safety and efficiency, demand for IONM systems is projected to increase significantly.

- Source Type Analysis: Insourced monitoring dominated the market with a 60.3% share, reflecting the preference for in-house neuromonitoring teams in surgical settings. This model provides greater control, improved communication, and better patient outcomes. Hospitals and surgical centers are increasingly adopting insourced services for higher consistency and responsiveness during procedures. The growing emphasis on clinical quality, cost-effectiveness, and real-time decision-making is expected to drive continued growth in the insourced monitoring segment of the IONM market.

- Application Analysis: The spinal surgery segment led with a 34.7% revenue share, supported by the rising incidence of spinal disorders such as herniated discs and scoliosis. Intraoperative neuromonitoring is essential in these surgeries to prevent nerve damage and ensure surgical accuracy. As minimally invasive spine surgeries grow in popularity, demand for IONM is expected to rise further. The need for real-time neural feedback in complex spinal procedures continues to drive expansion in this application segment.

- End-user Analysis: Hospitals accounted for 69.8% of the IONM market, reflecting their central role in performing high-risk surgeries. These institutions are increasingly integrating neuromonitoring into surgical protocols to improve patient safety and reduce complications. The growing volume of spinal, orthopedic, and neurosurgical procedures necessitates continuous neural assessment, which hospitals are well-equipped to deliver. As healthcare systems expand surgical capabilities and adopt advanced technologies, hospital-based IONM services are anticipated to witness sustained growth.

Market Segments

By Product Type

- Systems

- Services

- Accessories

By Source Type

- Outsourced Monitoring

- Insourced Monitoring

By Application

- Spinal Surgery

- Orthopedic Surgery

- Neurosurgery

- ENT Surgery

- Vascular Surgery

- Others

By End-user

- Hospitals

- Ambulatory Surgical Centers

Regional Analysis

North America led the Intraoperative Neuromonitoring (IONM) market in 2023, capturing a revenue share of 47.2%. This dominance is attributed to the widespread adoption of surgical procedures that carry a high risk of nerve damage. Regulatory support from the U.S. Food and Drug Administration (FDA) has significantly contributed to market growth. The FDA has cleared several IONM systems between 2022 and 2024, enabling broader hospital use.

Simultaneously, the National Institutes of Health (NIH) has supported research on IONM’s effectiveness, including studies focused on reducing neurological complications during spinal surgeries. In FY 2023, the NIH allocated over US$1.3 billion in grants for surgical and gene therapy-related research, underscoring IONM’s clinical relevance.

The Asia Pacific region is expected to record the highest CAGR over the forecast period. This growth is driven by an increasing number of complex surgical procedures, growing awareness of patient safety, and government-led healthcare improvements. Countries like Japan and South Korea are promoting surgical innovations, including IONM.

Initiatives by Japan’s Ministry of Health, Labour and Welfare (MHLW) support the integration of advanced medical technologies, while the rising burden of neurological disorders across the region further accelerates market adoption.

Emerging Trends

The adoption of intraoperative neuromonitoring (IONM) has expanded rapidly in the past decade. Between 2008 and 2014, the number of cases in which IONM of central and peripheral nervous electrical activity was employed rose from 31,762 to 125,835 a 296 % increase which reflects its growing acceptance in complex surgical procedures. Similarly, national data indicate that IONM use grew from just 1 % of all monitored cases in 2007 to 12 % by 2011, underscoring a steady year-on-year rise in its integration into operating rooms.

Integration of advanced technologies is shaping the next phase of IONM evolution. Explainable artificial intelligence (XAI) models are being developed to classify motor-evoked potential signals, with the aim of improving warning criteria and enhancing patient safety during high-risk neurosurgical and orthopedic interventions.

Additionally, AI algorithms have demonstrated the ability to detect intraoperative adverse events such as bleeding (n = 7), vessel injury (n = 1), and perfusion deficiencies (n = 1) with high sensitivity and specificity, supporting real-time decision making in the OR. Remote monitoring capabilities are also expanding; Medicare’s Local Coverage Determination for intraoperative neurophysiological testing now recognizes the value of off-site interpreting physicians to identify and prevent neural complications in real time.

Use Cases

In spinal and peripheral nerve surgeries, IONM is routinely employed to reduce the risk of neural injury. By 2014, a total of 125,835 cases utilized central and peripheral monitoring, compared to 31,762 in 2008. Use rates vary by patient socioeconomic status: monitoring is performed in 78.1 % of patients from high-income zip codes versus 19.9 % in low-income areas.

During thyroid and cranial procedures, somatosensory- and motor-evoked potentials guide the surgeon in preserving function. Surveys show that 60 % of practitioners always use IONM in thyroid surgeries, while 36 % use it selectively. This practice has been linked to reduced postoperative vocal cord paralysis and improved functional outcomes.

For real-time remote interpretation, a qualified neurologist monitors data streams off-site, communicating findings to the OR team. This model complies with Medicare requirements and has been implemented in hundreds of cases annually, ensuring continuous expert oversight even when in-person specialists are unavailable.

In AI-assisted adverse event detection, algorithms analyzed data from 2,982 studies and identified seven bleeding events, one vessel injury, and one thermal damage incident, achieving a pooled detection odds ratio of 14.74 (95 % CI 4.7–46.2). This capability supports early intervention and may further reduce complication rates in high-volume surgical centers.

Conclusion

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)