Table of Contents

Overview

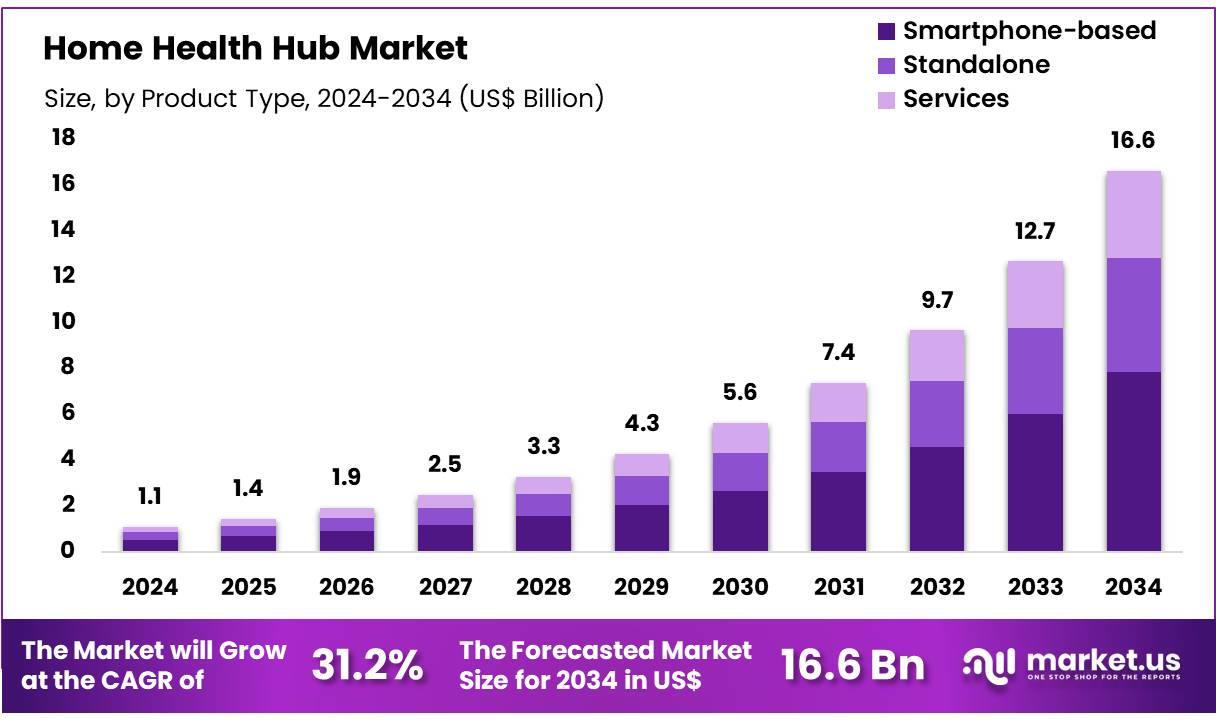

New York, NY – Dec 03, 2025 – Global Home Health Hub Market size is expected to be worth around US$ 16.6 Billion by 2034 from US$ 1.1 Billion in 2024, growing at a CAGR of 31.2% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 39.5% share with a revenue of US$ 0.4 Billion.

A new digital platform, Home Health Hub, has been introduced to support the growing demand for remote patient monitoring and in-home healthcare coordination. The platform has been developed to streamline patient management, enhance communication, and improve health outcomes through an integrated digital ecosystem. The launch reflects the rising need for connected care solutions as healthcare providers continue to expand virtual and home-based care services.

Home Health Hub has been designed to connect patients, caregivers, and clinicians through a centralized interface. The platform enables real-time monitoring of vital parameters, medication adherence tracking, and seamless data sharing across care teams. The adoption of automated alerts and standardized reporting formats is expected to support timely interventions and reduce avoidable hospital visits.

The growth of digital health adoption has been driven by increasing chronic disease prevalence, rising healthcare costs, and a shift toward value-based care models. The introduction of Home Health Hub aligns with these market dynamics, offering a scalable solution that supports personalized and continuous care. The platform’s interoperability with electronic health records and medical devices strengthens its utility for healthcare systems seeking to improve operational efficiency.

The launch of Home Health Hub is anticipated to facilitate improved patient engagement, better care continuity, and enhanced provider productivity. The platform is positioned to contribute to the broader transformation of home healthcare delivery, as demand for remote and technology-enabled services continues to rise globally.

Key Takeaways

- In 2024, the Home Health Hub market recorded revenue of US$ 1.1 billion, supported by a CAGR of 31.2%, and is projected to reach US$ 16.6 billion by 2034.

- The market by product type is categorized into smartphone-based, standalone, and services, with smartphone-based solutions accounting for the highest share of 47.3% in 2024.

- Based on patient monitoring type, the market is segmented into high-acuity, moderate-acuity, and low-acuity, where high-acuity monitoring represented a significant 42.8% share.

- By end user, the market is divided into hospitals, home care agencies, and healthcare payers. The hospital segment remained dominant, contributing 53.6% of total revenue in 2024.

- Regionally, North America led the global Home Health Hub market with a 39.5% market share in 2024.

Regional Analysis

North America as the Leading Region in the Home Health Hub Market

North America accounted for the largest revenue share of 39.5%, driven by the strong preference for aging in place and the growing use of remote patient monitoring technologies. The U.S. Census Bureau reports a steady rise in the population aged 65 and above, a demographic group that consistently favors home-based care models.

In addition, the Centers for Medicare & Medicaid Services (CMS) continue to support home healthcare through multiple initiatives aimed at promoting cost-efficient and patient-centered care. The expanding availability of connected medical devices capable of transmitting health data to home-based hubs further strengthens market adoption, enabling improved chronic disease management and reducing the frequency of hospital visits.

Asia Pacific Expected to Record the Highest CAGR

The Asia Pacific region is projected to exhibit the fastest CAGR during the forecast period, supported by a rising geriatric population and increasing awareness of the advantages associated with home-based healthcare. Japan, in particular, has a rapidly aging society, generating substantial demand for remote monitoring and independent-living solutions.

Growing utilization of telehealth services and wider penetration of smart home technologies across the region are anticipated to accelerate the adoption of home health management systems. Moreover, government-led initiatives aimed at enhancing healthcare accessibility and affordability are expected to contribute positively to the market’s overall expansion.

Emerging Trends

- Expanded Telehealth Coverage in Home-Based Care: Recent CMS innovation models have broadened telehealth eligibility to include home health visits and remote patient monitoring. This development has enabled home health hubs to be integrated into Medicare care pathways, supporting continuous monitoring beyond conventional clinical environments.

- Design Thinking Tailored to Older Adults: The development of home health hub platforms is increasingly influenced by design thinking approaches focused on older adult needs. Iterative prototypes based on direct input from individuals aged 65 and above are improving usability, cognitive support, and functional accessibility.

- Focus on Accessibility for People with Disabilities: New WHO–ITU accessibility guidelines are encouraging the creation of home health hub solutions that support users with disabilities. An estimated 1.3 billion people worldwide may benefit as telehealth platforms become interoperable with a wider range of assistive technologies.

- Global Digital Health Strategy Alignment: The WHO Global Strategy on Digital Health (2020–2025) is guiding nations toward interoperable standards for remote monitoring technologies. Home health hubs are being positioned as essential components in digital health architectures to strengthen data exchange, safety, and compliance.

Frequently Asked Questions on Home Health Hub

- How does a Home Health Hub work?

The hub aggregates patient health data from connected devices and forwards it to healthcare systems through secure communication channels. This continuous data flow enables proactive clinical oversight, supports intervention planning, and helps improve long-term patient outcomes through timely decision-making. - What conditions are commonly monitored using Home Health Hubs?

Home health hubs are commonly used for chronic disease monitoring, including diabetes, hypertension, respiratory disorders, and cardiovascular diseases. Continuous data tracking supports earlier detection of irregularities, helping reduce hospitalizations and enhancing treatment adherence. - What are the key components of a Home Health Hub?

Typical components include sensors, wearable monitors, communication modules, and a central software platform. These elements work together to gather patient data, ensure secure transmission, and present actionable insights to clinicians for effective care coordination. - What are the benefits of using a Home Health Hub?

The primary benefits include reduced hospital visits, improved chronic disease management, enhanced patient engagement, and better resource utilization for healthcare providers. The technology facilitates cost savings through improved monitoring efficiency and optimized clinical intervention patterns. - How secure is patient data on Home Health Hubs?

Patient data is protected through advanced encryption protocols and regulatory-compliant frameworks. Continuous oversight ensures data confidentiality, while access controls and authentication mechanisms minimize security risks and help maintain patient trust in digital care solutions. - What are the major segments of the Home Health Hub Market?

The market is typically segmented by product type, connectivity, end-user, and application. Remote monitoring hubs, telehealth platforms, and integrated communication systems represent the core product categories serving hospitals, home care providers, and individual patients. - Which regions are leading the Home Health Hub Market?

North America holds a dominant share due to advanced digital infrastructure, high healthcare spending, and supportive reimbursement systems. Europe shows strong adoption, while Asia-Pacific exhibits rapid growth driven by expanding telemedicine adoption and increasing chronic disease burdens.

Conclusion

The Home Health Hub market is positioned for robust long-term expansion as demand for connected, home-based care continues to rise. Growth has been supported by increasing chronic disease prevalence, aging populations, and broader adoption of digital health technologies. The platform’s interoperability, real-time monitoring capabilities, and alignment with value-based care models have strengthened its relevance for healthcare providers.

Regional momentum remains strong, with North America leading and Asia Pacific projected to accelerate rapidly. Overall, the market is expected to benefit from sustained investments in telehealth, enhanced accessibility standards, and continued emphasis on patient-centered, technology-enabled home healthcare delivery.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)