Table of Contents

Overview

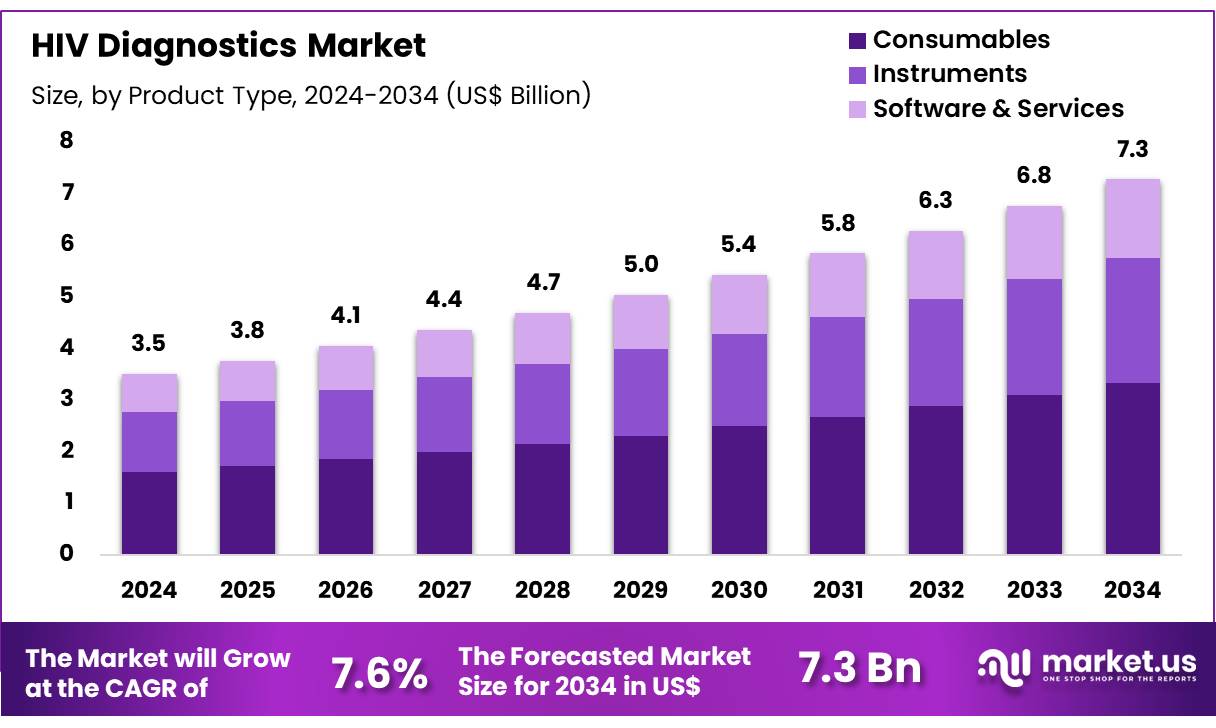

New York, NY – Nov 04, 2025 – Global HIV Diagnostics Market size is expected to be worth around US$ 7.3 billion by 2034 from US$ 3.5 billion in 2024, growing at a CAGR of 7.6% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 39.6% share with a revenue of US$ 1.4 Billion.

The global HIV diagnostics market has been witnessing steady expansion, driven by rising disease burden, increased public health initiatives, and continuous advancements in testing technologies. The prevalence of HIV infections remains a significant global health concern, and early diagnosis is considered critical for effective disease management and prevention. The market size has been growing due to enhanced awareness programs and broader adoption of routine screening protocols across healthcare systems worldwide.

The growth of the market can be attributed to technological innovation, including rapid point-of-care (POC) tests, molecular diagnostics, and home-based testing solutions. These advancements have enabled faster, more accurate, and accessible HIV screening, particularly in low-resource settings. Government organizations, non-profits, and global health agencies have been actively supporting testing campaigns, contributing to increased uptake of HIV diagnostics.

The HIV diagnostics market is expected to continue developing, supported by ongoing research, supportive governmental initiatives, and rising demand for early detection solutions. Strengthening outreach, innovation, and affordability is anticipated to further accelerate market expansion and enhance global testing accessibility. This sustained progress highlights the ongoing commitment toward combating HIV and improving patient outcomes worldwide.

Key Takeaways

- In 2024, the HIV diagnostics market generated revenue of US$ 5 billion and recorded a compound annual growth rate of 7.6%. The market is forecasted to reach US$ 7.3 billion by 2034.

- The market is categorized by product type into instruments, consumables, and software & services. Consumables accounted for the largest share in 2024, representing 45.8% of the overall market.

- Based on test type, the market includes viral load tests, antibody tests, CD4 tests, early infant diagnosis, and viral identification. Antibody tests contributed the highest share in this segment, holding 38.6% of the market.

- In terms of end users, the industry is segmented into diagnostic laboratories, hospitals, and other healthcare facilities. Diagnostic laboratories emerged as the leading end-user group, with a revenue share of 52.4% in 2024.

- From a regional perspective, North America dominated the market, capturing 39.6% of total revenue in 2024.

Regional Analysis

North America has been leading the HIV diagnostics market, accounting for 39.6% of the revenue share. This dominance can be attributed to continuous technological advancements in diagnostic testing, heightened awareness regarding early HIV detection, and persistent public health initiatives aimed at lowering transmission rates. Increased emphasis on preventive healthcare and routine screening among high-risk groups has supported strong adoption of advanced testing solutions.

Rapid, point-of-care diagnostic tools offering quick and accurate results have played a significant role in accelerating market expansion across the region. Strategic initiatives, such as Roche’s partnership with The Global Fund under its Global Access Program, have further contributed to progress by improving access to HIV diagnostics in resource-constrained settings.

These efforts have focused on strengthening laboratory systems, enhancing testing capabilities, and improving healthcare waste management infrastructure, collectively reinforcing broader HIV control strategies. Growing testing accessibility and sustained investments in healthcare infrastructure continue to support market growth in North America.

Asia Pacific is projected to register the fastest growth rate during the forecast period. Rising HIV prevalence, improving healthcare access, and increasing adoption of advanced diagnostic technologies are key drivers. Countries including India, China, and Thailand, which face notable HIV burdens, are expected to witness a surge in demand for testing solutions. According to data cited by The Indian Express in August 2022, approximately 24.01 million individuals in India were living with HIV, underscoring the urgency for effective diagnostics.

Government initiatives promoting early detection and treatment, expanding rapid testing availability, and targeted screening programs among high-risk groups are expected to accelerate market adoption. Strengthening healthcare infrastructure and growing public awareness are anticipated to further support market expansion, contributing to improved HIV management and prevention across the region.

Emerging Trends

- Expansion of HIV self-testing (HIVST) policies: The adoption of HIV self-testing has expanded significantly, supported by global guidelines. A total of 102 countries now have formal HIVST policies, and 63 nations have implemented routine programs designed to reach populations that are difficult to access through conventional testing services.

- Increase in rapid diagnostic test (RDT) procurement: Procurement of HIV rapid diagnostic tests in low- and middle-income countries has been rising. Between 2022 and 2027, annual procurement volumes are projected to range between 592 million and 838 million kits, indicating strong and sustained demand across global markets.

- Higher awareness of HIV status: Testing initiatives in communities and healthcare facilities have strengthened status awareness among affected populations. In 2023, approximately 86% of individuals living with HIV globally knew their HIV status, demonstrating considerable improvement in testing coverage and outreach efforts.

- Integration of testing with prevention services: HIV testing is increasingly integrated with preventive healthcare services. Self-testing has become a routine component for initiating, continuing, or restarting pre-exposure prophylaxis (PrEP), enabling improved prevention and ensuring timely linkage to care for individuals at higher risk.

Use Cases

- Community-based RDT deployment in LMICs: Large-scale procurement plans in low- and middle-income countries support community access to HIV testing. Over the next five years, an estimated 592 million to 838 million rapid diagnostic test kits will be supplied to clinics and outreach teams to improve testing coverage.

- Targeted testing for adolescent girls: Specialized programs target adolescent girls, a high-risk population group. In fiscal year 2023, PEPFAR provided HIV testing services to more than 7 million adolescent girls and distributed over 650,000 self-test kits to support early diagnosis and prevention.

- Multi-channel testing strategy in Tanzania: Tanzania has adopted a blended testing model to expand reach. Between October 2021 and March 2023, PEPFAR facilitated 5,856,460 HIV tests through facility-based services, mobile units, and index testing programs, demonstrating the effectiveness of mixed-delivery strategies.

- Pediatric HIV screening efforts by CDC: Pediatric screening campaigns have intensified to detect HIV in children early. In 2023, the CDC conducted more than 3.5 million HIV tests among children under 15 years of age, successfully linking over 300,000 young patients to appropriate treatment and care pathways.

Frequently Asked Questions on HIV Diagnostics

- Why is early HIV diagnosis important?

Early HIV diagnosis allows timely access to antiretroviral therapy, improving patient health outcomes and reducing virus transmission. Early detection also helps healthcare systems manage and monitor disease spread more effectively, supporting prevention and treatment strategies. - What types of HIV diagnostic tests are commonly used?

Common HIV diagnostic tests include antibody tests, antigen/antibody combination tests, nucleic acid tests, and rapid point-of-care screening. Each test evaluates different biological markers, providing varying degrees of accuracy and turnaround time for effective diagnosis. - Who should undergo HIV testing?

HIV testing is recommended for individuals at high risk of exposure, including those with unprotected sexual contact, needle sharing, or known exposure to an infected person. Routine testing is also encouraged for pregnant women and sexually active individuals. - What are rapid HIV tests?

Rapid HIV tests provide diagnosis within minutes by detecting antibodies or antigens through blood or oral fluid samples. These tests are widely used in clinics, community programs, and emergency settings to support timely screening and early treatment. - Which segment dominates the HIV diagnostics market?

Consumables hold a leading position due to consistent demand for test kits, reagents, and assay materials. Diagnostic laboratories also represent a significant share as centralized facilities enable accurate, large-volume HIV testing and continuous surveillance. - Which regions lead the HIV diagnostics market?

North America leads the market, supported by advanced healthcare systems, widespread screening, and research investment. Asia Pacific is projected to grow fastest, driven by high disease burden, expanding healthcare access, and increasing adoption of rapid diagnostics. - What is the future outlook for the HIV diagnostics market?

The market is expected to experience steady growth due to technological innovation, increased government initiatives, and rising demand for early detection. Adoption of point-of-care solutions and digital diagnostic tools will further improve testing accessibility and efficiency.

Conclusion

The HIV diagnostics market is positioned for sustained expansion, supported by strong public health initiatives, rapid technological progress, and increased global awareness regarding early detection. Growing adoption of point-of-care solutions, self-testing programs, and integration of diagnostics into prevention platforms continues to strengthen testing accessibility.

High-burden regions, particularly Asia Pacific, are expected to drive future growth through targeted government programs and improved healthcare infrastructure. Rising procurement of rapid test kits, especially in low- and middle-income countries, further indicates robust market momentum.

Continued investment, strategic collaborations, and innovation in testing technologies will remain essential in reducing HIV transmission and enhancing patient outcomes worldwide.