Table of Contents

Overview

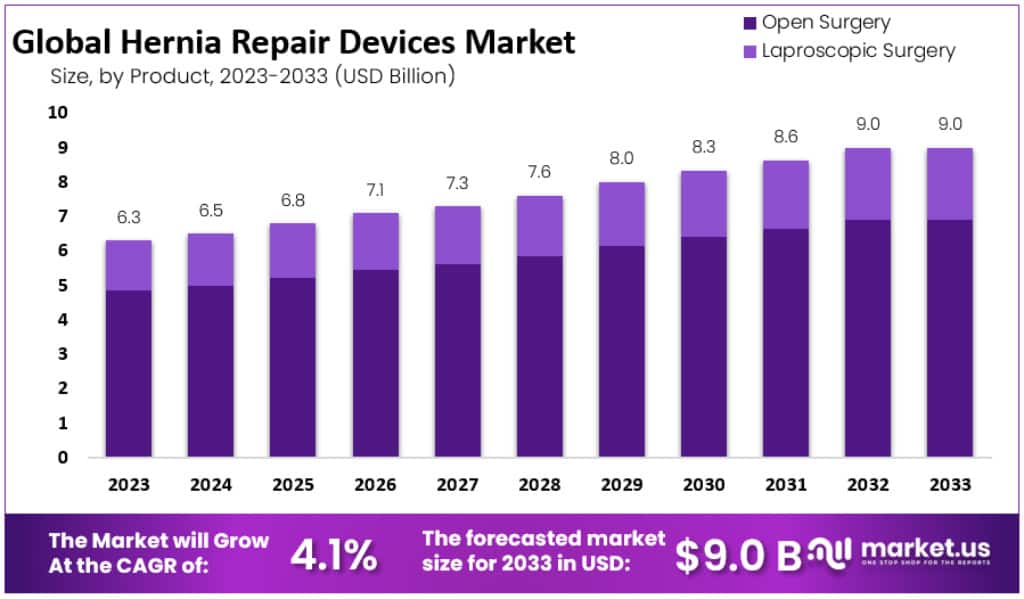

The Global Hernia Repair Devices Market is expected to reach USD 9 billion by 2033, rising from USD 3.3 billion in 2023. This growth reflects a CAGR of 4.1% during the forecast period. The rising disease burden, lifestyle-related risk factors, and aging demographics remain critical factors supporting steady procedure volumes worldwide. The hernia repair space continues to evolve with technological advancements, minimally invasive methods, and broader healthcare access across both developed and emerging economies.

The prevalence of hernia cases has been increasing over recent decades. In 2021, about 6.75 million people aged 45 and above were diagnosed with hernias. This points to a large pool of recurrent surgical candidates. Population growth and aging are key drivers of this absolute rise in cases, even as age-standardized rates have shown a decline. Obesity further adds to the burden, as a body mass index of 30 or more nearly doubles hernia risk. In morbidly obese patients, symptoms appear more frequently, reinforcing long-term demand for both primary and repeat repair procedures.

Minimally invasive and robotic surgeries are gaining a strong foothold in hernia repair. These approaches are associated with shorter hospital stays, reduced wound complications, and quicker recovery. Health policy initiatives, such as the U.K. NHS plan to expand robotic surgeries significantly by 2035, will drive further adoption. While research is still evaluating long-term recurrence rates for robotic repair, patient preference for minimally invasive options and investments in robotic systems ensure robust demand for related consumables, including meshes, trocars, and fixation devices.

Another critical market driver is the ongoing migration of surgeries to ambulatory surgical centers (ASCs). In the United States, ASC visits have grown by around 300% over the past two decades. More than 30% of 70 million annual procedures are now performed in ASCs. The ASC market itself is projected to expand at a 6% CAGR through 2030. This shift favors same-day hernia repair and strengthens demand for cost-effective meshes and fixation devices designed for outpatient use.

Innovations and Expanding Access in Hernia Care

Mesh-based repair techniques remain the gold standard in hernia surgery. Tension-free mesh approaches are associated with significantly lower recurrence rates compared to suture repair, ensuring consistent use in practice. Product innovation continues to push the market forward, with lightweight macroporous polypropylene and self-fixating meshes gaining popularity. New fixation methods such as absorbable tacks and glues are also being adopted. These advancements highlight the sector’s focus on improving patient outcomes and reducing surgical-site complications.

A growing emphasis is being placed on biosynthetic and reinforced biologic meshes. Early- and mid-term clinical evidence suggests these options can lower recurrence rates and surgical-site complications. Their adoption is building a premium segment within the market. Reinforced biologics and bioresorbable products with improved mechanical properties represent key areas of ongoing research. Such innovations strengthen replacement cycles and ensure continued device demand. Material science remains a critical field shaping the long-term trajectory of hernia repair products.

The global expansion of healthcare access also plays a significant role in market growth. Emerging economies are prioritizing health system modernization, expanding capacity in general surgery. National-level strategies to reduce surgical backlogs, particularly in the post-pandemic environment, are increasing access to procedures like hernia repair. Initiatives to develop ambulatory centers in the U.S. and robotic capacity in countries like the U.K. further enhance the ability of systems to manage patient volumes efficiently.

Together, these factors point to a favorable environment for the hernia repair devices market. A combination of growing disease prevalence, obesity-related risks, and rising surgical capacity provides a strong foundation for steady growth. The adoption of minimally invasive and robotic methods will continue to drive consumable demand. Meanwhile, product innovations and clinical advancements create opportunities for premium segments. The integration of modern care facilities in emerging markets ensures broader accessibility and sustained device utilization. The market’s long-term growth is therefore underpinned by both structural drivers and technological progress.

Key Takeaways

- The global hernia repair devices market is forecasted to expand from USD 3.3 billion in 2023 to nearly USD 9 billion by 2033.

- This expansion is anticipated at a compound annual growth rate of 4.1% during the forecast period from 2023 to 2033.

- The introduction of mesh in hernia repair procedures can lower hernia recurrence risks significantly, reducing the likelihood of reoperation by up to 50%.

- In 2023, hernia mesh dominated the market with a 76.1% share, comprising two major categories: biologic mesh and synthetic mesh.

- Open surgery remained the leading procedural method in 2023, commanding a 76.9% share, while laparoscopic surgery accounted for the remaining proportion.

- Inguinal hernia procedures represented the largest segment, contributing 67.5% of the market, confirming it as the most common hernia requiring surgical repair.

- Asia Pacific is projected to record the fastest revenue growth, with a forecast compound annual growth rate of 4.2% throughout the period.

- North America dominated the global market in 2023, generating USD 3.3 billion in revenue and securing a 52.4% regional market share.

- Medtronic maintained market leadership with an estimated 30% share, underlining its strong presence and competitive advantage in the hernia repair devices sector.

- High hernia mesh repair costs, ranging between USD 100 and USD 3,000, continue to limit accessibility for patients in lower-income regions globally.

Regional Analysis

North America accounted for the largest share of 52.4% in 2023. The dominance was supported by the presence of leading players in the market. Rising healthcare spending and favorable regulatory approvals from the FDA further accelerated growth. A sedentary lifestyle, an increasing elderly population, and higher recurrence rates of hernia cases were also important drivers. The region’s advanced healthcare infrastructure, coupled with strong demand for innovative medical devices, ensured a favorable environment for growth of the hernia repair devices market in North America.

The Asia Pacific region recorded the fastest revenue growth during the forecast period. Rising medical tourism, affordable healthcare services, and increasing adoption of advanced technologies were the primary growth factors. The region also benefitted from expanding healthcare reimbursement policies, which improved treatment access. Asian countries, particularly India and China, presented significant growth opportunities due to their large patient base. The strong demand for cost-effective hernia repair devices, together with government support for healthcare development, positioned Asia Pacific as a high-potential market.

The rising prevalence of untreated and undiagnosed hernia cases in Asia Pacific further enhanced growth prospects. A substantial patient population base increased the demand for hernia repair procedures across hospitals and clinics. Continuous improvements in healthcare infrastructure also supported the adoption of new treatment methods. Favorable government initiatives, combined with increasing private sector investments, played a critical role in market expansion. The combination of demand growth, affordability, and accessibility ensured strong momentum, making Asia Pacific a key contributor to global hernia repair device revenue growth.

Segmentation Analysis

In 2023, hernia mesh dominated the hernia repair devices market with a strong 76.1% share. This category is divided into biologic and synthetic mesh. Biologic mesh is valued for its compatibility with human tissues, while synthetic mesh is preferred for its durability and lower cost. Both types are critical in lowering hernia recurrence rates and enabling faster recovery. The remaining share is held by fixation devices, including sutures, tack applicators, and glue applicators, each meeting diverse surgical preferences and procedural demands.

Open surgery was the leading procedure type, capturing 76.9% of the market in 2023. This traditional method, involving a larger incision, remains popular due to its simplicity and effectiveness in treating complex or larger hernias. It continues to be favored by surgeons for its reliability and familiarity. Laparoscopic surgery accounted for the remaining share, offering a less invasive alternative. Its benefits include reduced pain, quicker recovery, and minimal scarring, though it requires advanced skills, reflecting the growing trend toward minimally invasive techniques.

By surgery type, inguinal hernia procedures held the largest share at 67.5% in 2023. The high prevalence of this condition, particularly among men, drives strong demand for repair devices in this segment. Umbilical hernias, common in infants and some adults, also contributed significantly. Incisional hernias, often resulting from prior abdominal surgeries, are becoming notable due to rising surgical volumes. Femoral hernias, though less frequent, remain relevant, especially among older women. Other rare types collectively support market demand, as each requires tailored devices for effective treatment and patient recovery.

Key Players Analysis

The global hernia repair devices market is dominated by a small group of established companies. Medtronic leads with around 30% market share, supported by its strong brand reputation, extensive product portfolio, and global distribution. Ethicon Inc., a subsidiary of Johnson & Johnson, holds a significant position with its widely adopted Prolene mesh product. BD also maintains a strong presence, offering reliable Bard hernia repair devices. These companies continuously invest in research and development to maintain their competitive edge and expand their product pipelines.

Other key market participants include Atrium, W. L. Gore & Associates, LifeCell International, and B. Braun SE. Each contributes with specialized solutions targeting diverse clinical needs in hernia repair procedures. Their focus on innovative surgical meshes, biologic grafts, and minimally invasive devices helps them sustain relevance. Strategic alliances and product launches are frequently employed to strengthen market penetration. Their regional expansion strategies also ensure that products reach emerging economies, where demand for advanced hernia repair treatments continues to grow.

Additional companies such as Baxter, Cook, and Herniamesh S.r.l. also play important roles in shaping competition within the industry. While their market share is relatively smaller, these firms maintain a focus on niche product offerings and cost-effective solutions. Innovation in mesh technology, patient safety improvements, and enhanced biocompatibility remain key priorities. Collectively, the presence of these established and emerging players drives steady market growth. Continuous advancements in surgical techniques and device innovation are expected to further support the market’s competitive landscape in the coming years.

FAQ

Q1. What are hernia repair devices?

Hernia repair devices are medical tools used during surgery to strengthen weak tissue in the abdominal wall. These include surgical mesh, sutures, tacks, and fixation systems. Surgical mesh is the most common device as it lowers the chances of hernia recurrence compared to simple stitches. Devices vary depending on surgical technique, such as open, laparoscopic, or robotic repair. Their role is to provide reinforcement, reduce strain on tissue, and support healing. Proper device choice improves patient outcomes and reduces complications.

Q2. What are the main types of surgical mesh?

Surgical mesh can be divided into synthetic and biologic types. Synthetic mesh is usually made from polypropylene or polyester. Biologic mesh is made from processed animal or human tissue. Mesh also differs by absorbability. Absorbable mesh breaks down over time, while non-absorbable remains permanently to provide lasting support. Composite meshes combine both properties. Mesh design varies in weight, porosity, and coating, which affect tissue integration and risk of complications. The type selected depends on the patient’s condition and surgery.

Q3. When is mesh used versus non-mesh hernia repair?

Mesh repair is used when the hernia is large or complex. It lowers the risk of recurrence compared to sutures alone. Non-mesh or suture repair may be chosen when the hernia is small or when mesh poses a risk. Examples include patients with infection, poor tissue healing, or allergies. The decision is based on hernia type, location, and patient history. Surgeons evaluate risks and benefits before recommending the method. Both approaches aim to restore abdominal wall strength and reduce recurrence.

Q4. What are risks or complications of hernia repair devices?

Complications may include infection, pain, mesh movement, and scar tissue formation. In some cases, mesh may shrink or erode, causing intestinal obstruction or organ perforation. Chronic pain and hernia recurrence are also possible risks. Most adverse events are uncommon but may occur when mesh is not suitable or when surgical technique is poor. Careful selection of mesh type, proper fixation, and surgeon experience reduce risks. Patients are advised to report unusual symptoms quickly for timely diagnosis and treatment.

Q5. How safe and effective is mesh in hernia repair?

Mesh repair is considered safe and widely used because it reduces hernia recurrence. Studies show mesh is more effective than sutures in preventing hernia return. Risks exist, but most patients experience improved outcomes. Complications like pain or infection are rare when the device and technique are appropriate. Long-term success depends on proper patient selection, mesh type, and surgeon skill. Despite concerns, mesh remains a standard tool in hernia surgery worldwide. Most patients recover well with fewer recurrences after mesh repair.

Q6. Does mesh show up or interfere with imaging?

Mesh visibility on imaging depends on the material used. Synthetic meshes may appear on X-rays or CT scans, while biologic meshes are less visible. Some meshes contain coatings or metallic markers to help identify them on scans. Mesh does not usually block imaging or interfere with diagnosis. Patients are encouraged to keep records of the device brand and type. This information is important if future surgery or imaging is needed. Surgeons and radiologists can then provide safer, accurate assessments.

Q7. What questions should patients ask about hernia devices?

Patients should ask about the hernia type, treatment options, and whether mesh or sutures will be used. They should ask about the specific mesh brand, material, and whether it is absorbable or permanent. It is important to discuss risks like recurrence, infection, or chronic pain. Questions about recovery time and possible complications should be raised. Patients should also ask how the device will affect future surgeries. Clear communication with the surgeon ensures informed choices and helps improve surgical outcomes.

Q8. Why were some hernia mesh products recalled?

Certain hernia mesh products were recalled due to safety concerns. Issues included mesh shrinkage, breaking, or migrating after surgery. These failures caused complications such as pain, infection, or recurrence. Some recalls were voluntary, while others followed regulatory actions. Recalls led to lawsuits and greater public concern about mesh safety. Most recalled products had design flaws or unsuitable coatings. Regulatory agencies now monitor device safety more closely. Manufacturers are required to provide stronger clinical evidence before releasing new hernia repair products.

Q9. What is the current size of the hernia repair devices market?

The global hernia repair devices market was valued at around USD 3.3 Billion in 2023. This figure represents revenue from surgical mesh, fixation devices, and other supporting tools. Growth is driven by high surgical demand worldwide. Hospitals and surgical centers are the largest users of these products. Market size reflects both elective and emergency procedures across multiple hernia types. Increased healthcare spending and awareness have also supported expansion. The figure is expected to rise steadily in the coming years.

Q10. What is the projected growth rate of the market?

The hernia repair devices market is projected to grow at a compound annual growth rate of about 4.1% from 2024 to 2033. The market value is expected to reach approximately USD 9 billion by 2033. Growth is supported by rising hernia cases, aging population, and wider adoption of minimally invasive surgery. New mesh technologies and fixation systems will also boost demand. Despite cost and safety concerns, strong surgical need ensures consistent expansion. Emerging economies are expected to show faster growth.

Q11. What are the main product segments?

The market is divided into mesh devices and fixation products. Mesh accounts for the largest share due to its wide use in most hernia surgeries. Fixation devices include sutures, tacks, and glue systems. The market is also segmented by procedure type: open, laparoscopic, and robotic surgeries. Another division is by hernia type, including inguinal, ventral, umbilical, and femoral hernias. End users include hospitals, ambulatory surgical centers, and specialty clinics. Each segment reflects different demand patterns, influenced by healthcare infrastructure and affordability.

Q12. What drives market growth?

Several factors drive market growth. Rising hernia cases from aging, obesity, and abdominal surgeries increase surgical demand. Adoption of minimally invasive approaches such as laparoscopic and robotic repair is growing. Innovations in mesh, like lightweight or biologic options, boost adoption. Improved fixation technologies also support growth. Awareness campaigns and favorable reimbursement further encourage surgeries. Expanding healthcare access in emerging markets contributes to higher demand. Altogether, these drivers create strong momentum for hernia repair devices across global healthcare systems and markets.

Q13. What challenges limit growth?

The market faces challenges such as high device costs and expensive minimally invasive procedures. Concerns about mesh safety and complications limit patient acceptance. Public perception, influenced by recalls and lawsuits, creates restraint. Regulatory differences across regions also slow product approvals. In developing countries, limited access to advanced devices is a barrier. Skilled surgeon availability for laparoscopic and robotic methods remains uneven. Together, these factors create hurdles that may restrict growth pace, despite the strong demand for hernia repair solutions.

Q14. Who are the major players in the market?

Leading companies include Medtronic, Ethicon Inc., BD, Atrium, W. L. Gore & Associates, Inc., LifeCell International Pvt. Ltd., B. Braun SE, Baxter, Cook, Herniamesh S.r.l., Other Key Players. These firms dominate the market with large product portfolios and global reach. They focus on mesh innovation, advanced fixation devices, and expanding distribution networks. Competition is strong, with emphasis on product safety, clinical outcomes, and regulatory approvals. Strategic partnerships, acquisitions, and new product launches remain key approaches for these leading companies.

Q15. Which regions lead the market?

North America, especially the U.S., dominates the market with a 52.4% share in 2023, valued at USD 3.3 billion. Growth is supported by advanced healthcare infrastructure and reimbursement systems. Europe also holds a strong share due to widespread hernia cases and adoption of new technologies. The Asia-Pacific region is projected to grow fastest, driven by rising healthcare spending, awareness, and surgical capacity. Emerging economies in Asia and Latin America show increasing demand for minimally invasive hernia repair. Regional growth trends vary depending on cost and accessibility.

Q16. How did COVID-19 impact the market?

COVID-19 slowed elective surgeries, including hernia repair, leading to reduced device demand in 2020. Hospitals prioritized emergency care, delaying planned procedures. Supply chain disruptions also affected availability of devices. After restrictions eased, surgical backlogs increased demand, helping recovery. Many hospitals now prioritize minimally invasive methods to reduce hospital stays. Safety measures and infection control gained more importance. Although the pandemic caused short-term decline, it also accelerated adoption of new techniques. Post-pandemic, the market is showing strong signs of recovery.

Q17. What opportunities exist in the market?

Future opportunities lie in developing biologic and bioabsorbable meshes, which reduce complications. Adhesive fixation and novel anchoring systems are gaining attention. Robotics and imaging-guided devices present growth potential. Manufacturers are also focusing on making cost-effective products for emerging markets. Increasing use of patient data and surgical planning tools improves outcomes. Stronger regulatory frameworks and post-market surveillance build trust. As healthcare systems expand access, demand for safe, advanced, and affordable hernia repair devices will continue to increase globally.

Conclusion

The hernia repair devices market is set for steady expansion, driven by growing patient needs, rising obesity, and wider access to advanced surgical care. Demand is further strengthened by the preference for minimally invasive and robotic procedures, which enhance recovery outcomes and encourage higher adoption of consumables. Mesh remains the cornerstone of hernia repair, while biologic and bioresorbable innovations are opening opportunities in premium product segments. At the same time, expanding healthcare infrastructure in emerging economies ensures broader treatment availability. Together, these trends create a stable outlook for the industry, with long-term growth supported by innovation, demographics, and continuous improvements in surgical practices.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)