Table of Contents

Overview

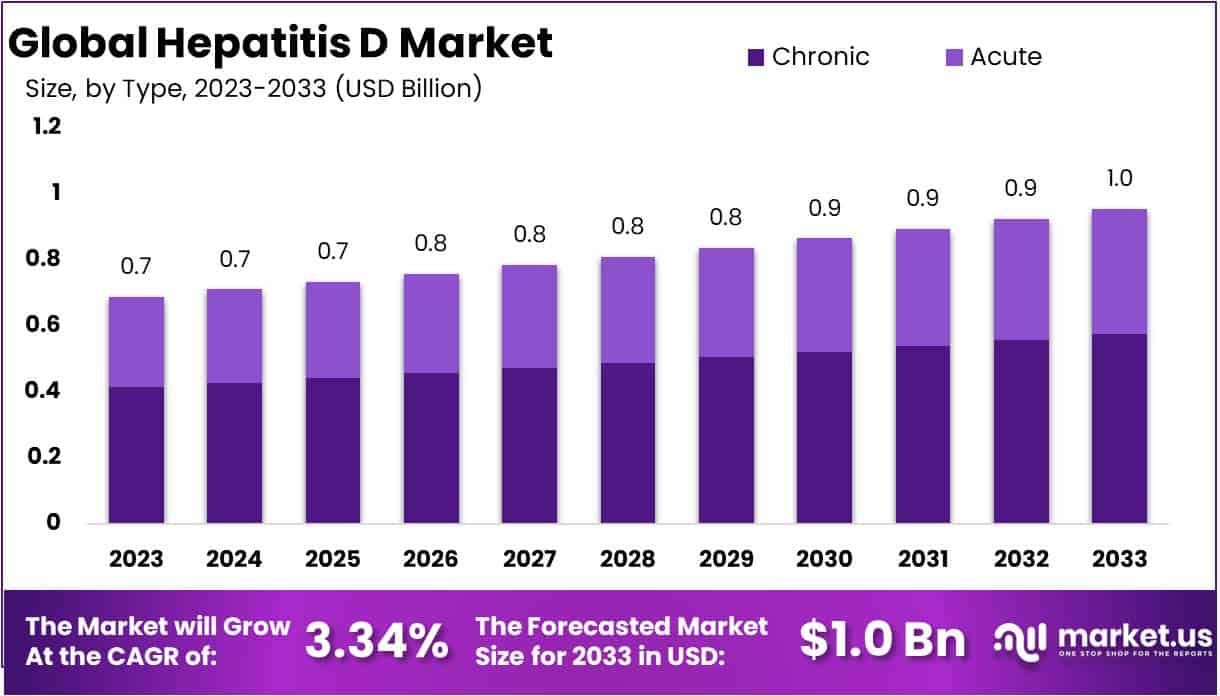

The Global Hepatitis D Market is projected to reach USD 1 billion by 2033, rising from USD 0.7 billion in 2023. A CAGR of 3.34% is anticipated during the forecast period. Growth has been supported by wider disease awareness and improved screening initiatives. More individuals are being tested for viral hepatitis, which has increased the identification of Hepatitis D cases. This trend has strengthened the need for effective treatment pathways and reliable diagnostic practices across healthcare systems.

Market expansion has also been influenced by stronger Hepatitis B vaccination programs. Because Hepatitis D occurs only in individuals with Hepatitis B, screening of high-risk groups is becoming more structured. Vaccination initiatives are improving early detection and prevention strategies. These efforts have encouraged demand for monitoring technologies and public health interventions designed to reduce disease complications and improve patient tracking.

Significant progress in clinical research has further supported market growth. Multiple investigational therapies are being developed to control viral replication and improve long-term outcomes. Investment from biotechnology companies and research institutions has increased, accelerating innovation in antiviral treatments. Regulatory bodies are offering faster review processes for promising drug candidates, and this is expected to enhance future product availability and encourage competitive therapeutic development.

Advances in diagnostic technology are playing a crucial role in shaping the sector. Modern molecular tests and sensitive assay systems enable early and accurate detection. Early diagnosis reduces disease progression risks and improves care outcomes. As laboratories and hospitals adopt these technologies, the demand for advanced testing equipment continues to rise. Expanded diagnostic capacity also supports national and global surveillance programs targeting viral hepatitis control.

Rising healthcare expenditures and supportive government initiatives are reinforcing market stability. Countries are investing in improved treatment access, better testing facilities, and broader public health education. International health agencies continue to classify Hepatitis D as a priority concern, prompting stronger surveillance frameworks. In addition, the shift toward patient-centered care has encouraged higher diagnosis rates. Patients now benefit from improved access to information, community support networks, and emerging therapeutic options, which collectively strengthen overall market growth.

Key Takeaways

- The market is projected to reach nearly USD 1 Billion by 2033, rising from USD 0.7 Billion in 2023 with a steady 3.34% CAGR.

- The chronic hepatitis D segment accounted for 60.2% of revenues in 2023, reflecting its strong dominance across global clinical management and treatment needs.

- Blood tests maintained priority among healthcare providers, enabling this diagnostic method to lead the market due to accuracy, accessibility, and widespread clinical adoption.

- Hospital pharmacies emerged as the primary distribution channel, supported by their reliable access to specialized therapies and integration within established patient care pathways.

- Growing Hepatitis D infection rates increased the demand for therapeutic interventions, contributing significantly to overall market expansion across major healthcare systems.

- High treatment costs and notable medication side effects created barriers that are anticipated to restrict broader market penetration in the near future.

- North America captured 52.4% of global revenues in 2023, benefiting from advanced healthcare infrastructure, strong awareness levels, and established diagnostic capabilities.

Regional Analysis

North America accounted for a significant revenue share of 52.4% in the global Hepatitis D treatment market in 2023. The region’s position has been supported by the rising burden of hepatitis D in specific population groups. High-risk communities, including individuals with chronic hepatitis B infection, have shown elevated disease incidence. This has increased the demand for diagnostic tests and treatment access. The expanding patient base has reinforced market strength. Consistent screening efforts have further supported growth. Overall, the region’s dominance has remained stable.

High-prevalence pockets within North America have strengthened the need for efficient therapeutic solutions. Communities with higher injection drug use have shown growing vulnerability. This pattern has created additional pressure on healthcare systems to provide timely care. Increased disease awareness has also influenced testing volumes. These conditions have contributed to a robust market environment. The rising adoption of advanced treatment approaches has supported revenue expansion. The overall trend indicates sustained demand. As a result, the regional market has demonstrated consistent upward movement.

Advanced healthcare infrastructure has played a central role in maintaining regional leadership. The presence of well-established hospitals and clinics has improved access to specialized care. Skilled healthcare professionals and modern diagnostic capabilities have supported efficient disease management. Availability of advanced therapeutic interventions has strengthened patient outcomes. Investment in clinical services has enhanced treatment adoption. These advantages have supported continuous market expansion. Ongoing improvements in healthcare delivery have further reinforced growth. Consequently, North America has continued to demonstrate strong performance in recent years.

Segmentation Analysis

The chronic hepatitis D segment continues to lead the global market, with a revenue share of 60.2% in 2023. This dominance can be attributed to persistent infection patterns and long-term liver inflammation linked to hepatitis D virus. The condition progresses over time and increases demand for continuous medical care. Severe complications such as cirrhosis, liver failure, and hepatocellular carcinoma require consistent monitoring and treatment. Limited antiviral options further increase the need for disease management. Global prevalence has been estimated at 0.80% in the general population and 13.02% among HBV carriers.

The diagnosis landscape is primarily driven by blood tests, which hold the largest revenue share in the global hepatitis D market. Clinicians rely on these tests to detect anti-HDV IgG and IgM levels, enabling accurate identification of infection. This method provides reliable confirmation and supports timely intervention. The preference for blood-based diagnostics is supported by accessibility and clinical accuracy. Other diagnostic methods, including elastography and liver biopsy, remain relevant but secondary. As a result, blood tests continue to influence market performance through widespread adoption and strong clinical utility.

Hospital pharmacies represented 71.5% of the distribution channel share in 2023 and continue to dominate the market. This position is supported by structured systems for managing complex treatment regimens and maintaining proper storage conditions. Professional staff ensure accurate dosing and adherence monitoring. Collaboration between hospitals and specialists further strengthens treatment outcomes. These facilities provide reliable access to essential therapies and enhance patient confidence. Retail and online pharmacies remain present but hold smaller shares. Overall, hospital pharmacies contribute significantly to global hepatitis D market expansion through integrated service delivery.

Key Players Analysis

The competitive landscape of the Hepatitis D market has been shaped by continuous efforts to expand product portfolios and strengthen research capabilities. Companies have adopted structured strategies to sustain their global presence. These strategies have included investments in advanced antiviral research and the integration of new therapeutic technologies. As a result, the market has remained fragmented and dynamic. Major contributors such as Merck & Co., Gilead Sciences, and Eiger BioPharmaceuticals have reinforced leadership through consistent development activities and targeted innovation programs.

Intense competition has been observed due to the entry of emerging biotechnology firms seeking to challenge established players. These firms are required to navigate strong brand dominance and extensive distribution networks controlled by global leaders. Strategic partnerships and collaborative development programs have been used widely to strengthen positions within this market. Companies including Antios Therapeutics, GlaxoSmithKline, and Janssen Pharmaceuticals have utilized these strategies to enhance pipeline strength, secure technological advantages, and address evolving clinical demands in Hepatitis D treatment.

A strong focus on mergers, acquisitions, and technology-based alliances has supported continuous market growth. These approaches have helped companies expand therapeutic portfolios and accelerate product commercialization. The development of targeted therapies and novel antiviral drugs has been prioritized to address unmet clinical needs. Firms such as Amega Biotech, Hepion Pharmaceuticals, and PharmaEssentia Corporation have invested in clinical research frameworks that enhance treatment efficacy. This strategic direction has contributed to improved competitiveness and broader global outreach across key regions.

Growing emphasis on cost-efficient manufacturing and expanded geographic coverage has further shaped market performance. Companies have implemented scalable production systems and wider distribution channels to secure competitive advantages. This expansion trend has been supported by collaborations with regional suppliers and enhanced regulatory compliance initiatives. Organizations including Apotex Corp., Aurobindo Pharma, Zydus Pharmaceuticals, and Mylan N.V. have leveraged these strategies to broaden product access. Their efforts have strengthened market penetration and supported the overall advancement of Hepatitis D therapeutic solutions.

Challenges

1. Limited Awareness and Late Diagnosis

Awareness of Hepatitis D remains low in many regions. Patients and healthcare providers often do not recognize early symptoms. As a result, diagnosis typically occurs at advanced stages of the disease. Late detection reduces the effectiveness of available treatments and slows patient recovery. The delay also increases the risk of complications, which places a higher burden on healthcare systems. Limited knowledge among clinicians further reduces testing rates and prevents timely intervention. These factors contribute to lower treatment uptake and weaker market growth. Improving awareness and screening programs is therefore essential for strengthening early diagnosis and expanding the overall market potential.

2. Small Patient Pool

Hepatitis D can occur only in individuals already infected with Hepatitis B. This creates a restricted patient population from the start. Because the pool is small, the market demand for treatments remains limited. Many cases also stay undiagnosed due to poor testing practices. The reduced number of confirmed patients lowers commercial interest for drug developers and decreases investment in new therapies. Pharmaceutical companies often view such small segments as high-risk due to uncertain returns. This limits innovation and slows the introduction of advanced treatment options. The narrow patient base therefore remains a major challenge for long-term market expansion.

3. High Treatment Costs

Existing therapies for Hepatitis D remain expensive for many patients. High treatment costs limit access, especially in low-income and middle-income countries. Patients often face financial barriers that delay or prevent treatment initiation. Healthcare systems in resource-constrained regions may also struggle to fund advanced therapies. Limited reimbursement policies further reduce affordability and discourage adoption. When fewer patients can afford treatment, overall market growth slows. The price burden also affects physicians’ decisions, as they may hesitate to recommend costly solutions. Reducing treatment costs and improving funding mechanisms will be essential to increase patient access and support broader market development.

4. Limited Approved Therapies

The number of approved therapies for Hepatitis D remains very small. This lack of targeted treatment options limits physicians’ ability to manage the disease effectively. Patients often rely on older or less effective therapies, which do not address all clinical needs. The shortage of innovative solutions creates major gaps in care and increases the disease burden. Limited treatment choices also reduce confidence among healthcare providers and restrict adoption rates. Pharmaceutical companies face challenges when entering a market with few established products and uncertain demand. Expanding the availability of approved therapies is therefore crucial to improving clinical outcomes and supporting market growth.

5. Complex Disease Biology

Hepatitis D is considered one of the most severe viral hepatitis infections. Its biology is highly complex and difficult to study. This makes drug development a slow and costly process. Researchers face challenges in understanding disease progression, immune responses, and viral behavior. These scientific barriers extend clinical timelines and increase regulatory requirements. As a result, fewer companies are willing to invest in new therapies. Complex disease characteristics also limit the success of clinical trials and delay product approvals. These factors collectively slow innovation and restrict the introduction of advanced treatments in the global market.

6. Regional Disparities in Healthcare Access

Access to Hepatitis D testing and treatment varies widely across regions. High-income countries typically have better diagnostic facilities and trained professionals. In contrast, low- and middle-income regions face shortages of specialists, laboratories, and screening programs. These gaps lead to late diagnoses and poor disease management. Limited resources reduce awareness, testing frequency, and treatment availability. Uneven access restricts patient outcomes and slows overall market development. Geographic disparities also influence product adoption and commercial performance, as companies face inconsistent demand across markets. Strengthening healthcare infrastructure and improving regional capacity are essential for reducing gaps and supporting long-term market growth.

Opportunities

1. Rising Focus on Early Screening Programs

Early screening programs for viral hepatitis are gaining strong attention worldwide. Governments and healthcare agencies are promoting these programs to reduce long-term disease burdens. Increased screening for Hepatitis B often leads to higher detection of Hepatitis D. This shift supports improved patient identification at earlier disease stages. Better diagnosis also increases the likelihood of timely medical intervention. As awareness grows, more patients are expected to enter treatment pathways. The expansion of national screening frameworks is shaping a favorable environment for diagnostic companies. As a result, significant opportunities are emerging for technology providers and drug developers.

2. Growing Investment in Antiviral Research

Investment in antiviral research continues to rise as companies respond to unmet clinical needs. Pharmaceutical firms are allocating larger budgets to develop effective Hepatitis D therapies. Many research programs are exploring new molecules and treatment pathways. These investments improve the likelihood of discovering therapies with stronger safety and efficacy profiles. Advancements in virology and immunology also support faster drug development. Stronger pipelines create a competitive environment that encourages innovation. As new candidates move into advanced clinical stages, the market is expected to benefit from greater therapeutic diversity. This trend supports long-term growth prospects across global markets.

3. Increasing Adoption of Novel Mechanisms

New therapeutic mechanisms are being explored to manage Hepatitis D more effectively. These mechanisms target the virus in ways that differ from traditional therapies. Early clinical findings show promising improvements in patient outcomes. Developers are also focusing on approaches that can reduce disease complications. Regulatory bodies are increasingly receptive to innovative treatments that address unmet needs. As more novel mechanisms progress through trials, approval prospects strengthen. These advancements may reshape clinical practice by introducing more targeted and durable treatment options. The market is likely to expand as clinicians adopt therapies that deliver measurable benefits.

4. Expansion in High-Burden Regions

Regions with high disease prevalence, such as parts of Asia, Eastern Europe, the Middle East, and Africa, present strong market potential. Many of these areas are improving their healthcare systems. Expanded access to diagnostic tools and antiviral drugs is becoming more common. Rising awareness encourages earlier medical consultation and testing. Public and private stakeholders are investing in disease management programs. These efforts are expanding treatment capacity and creating favorable market conditions. As infrastructure strengthens, demand for advanced Hepatitis D therapies is expected to grow. Companies entering these regions may experience significant commercial gains.

5. Growing Support from Health Organizations

International health organizations are increasing their involvement in viral hepatitis control. These groups support national programs with funding and technical guidance. Awareness campaigns highlight the risks of untreated Hepatitis D and promote early diagnosis. Policies encouraging improved screening and treatment access are being implemented across several countries. Partnerships between governments and global agencies are creating stronger care frameworks. These initiatives raise overall patient engagement in healthcare systems. As adoption of recommended guidelines expands, treatment rates are expected to rise. This supportive environment offers significant opportunities for pharmaceutical and diagnostic companies.

6. Rising Interest in Combination Therapies

Combination therapies are attracting strong interest in the management of Hepatitis D. Researchers believe that combining multiple mechanisms may improve patient response. Early studies show the potential for better viral suppression and reduced relapse rates. Pharmaceutical companies are designing regimens that pair novel agents with existing standards of care. Combination approaches may address limitations seen in single-agent therapies. These strategies are also gaining attention from regulators seeking improved clinical outcomes. As evidence grows, clinicians may shift toward multi-component treatment plans. This trend is expected to open new commercial pathways and support long-term market growth.

Conclusion

The global Hepatitis D market is expected to show steady growth, supported by stronger screening programs, rising awareness, and ongoing advances in diagnostic and treatment options. Demand has been influenced by early testing efforts and wider adoption of modern healthcare practices. Continued investment in antiviral research is creating space for new and more effective therapies. Supportive government actions and improved access to clinical care are also strengthening overall market performance. Although challenges remain due to limited treatment choices and high costs, ongoing innovation and expanding healthcare capacity are expected to create a more favorable environment for long-term market development.

View More

Hepatitis B Diagnostic Tests Market || Hepatitis C Market || Non-Alcoholic Steatohepatitis Treatment Market || Hepatitis A Vaccine Market

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)