Table of Contents

Overview

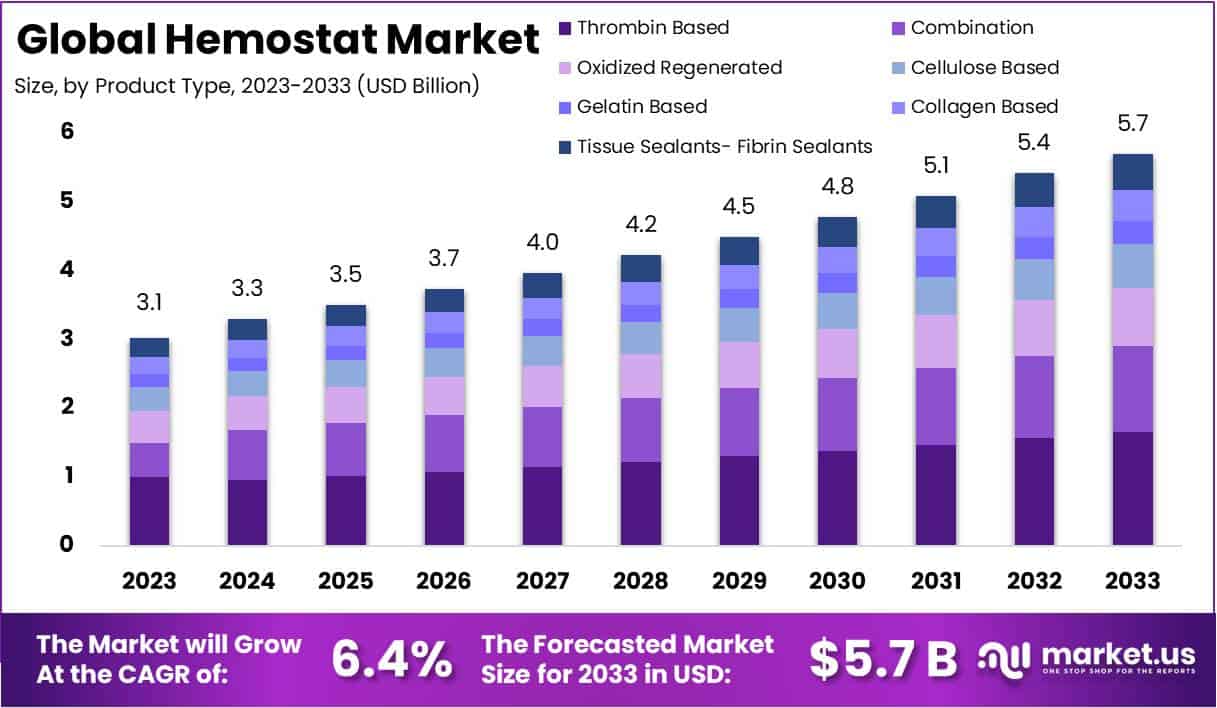

New York, NY – Jan 12, 2026 – The Global Hemostat Market size is expected to be worth around USD 5.7 Billion by 2033, from USD 3.1 Billion in 2023, growing at a CAGR of 6.4% during the forecast period from 2024 to 2033.

A hemostat is a fundamental surgical and medical instrument designed to control bleeding during clinical procedures. Its primary function is to clamp blood vessels or tissues, thereby preventing excessive blood loss and improving procedural safety. Hemostats are widely used across hospitals, clinics, emergency care settings, and surgical centers, reflecting their essential role in modern healthcare practices.

The basic formation of a hemostat consists of three main components: the jaws, the shanks, and the locking mechanism. The jaws are typically serrated to provide a firm grip on blood vessels or tissues. The shanks connect the jaws to the handles and allow precise manipulation by the clinician. The locking mechanism, often a ratchet system, enables the instrument to remain securely closed without continuous hand pressure, supporting efficiency during procedures.

Hemostats are commonly manufactured from high-grade stainless steel to ensure durability, corrosion resistance, and compatibility with repeated sterilization. Variations in size, curvature, and jaw design are available to meet different procedural requirements, ranging from minor wound management to complex surgical interventions.

The importance of hemostats has increased with the rising volume of surgical procedures and the growing emphasis on patient safety and blood loss management. Their consistent performance contributes to reduced operative risks, improved visibility for clinicians, and better clinical outcomes.

Overall, the hemostat remains a cornerstone instrument in medical practice. Its simple yet effective design continues to support a wide range of healthcare applications, reinforcing its long-standing value within the global medical device landscape.

Key Takeaways

- Market Growth Outlook: The global Hemostat Market is projected to attain a valuation of USD 5.7 Billion by 2033, registering a steady CAGR of 6.4% over the forecast period from 2024 to 2033.

- Leading Product Category: Thrombin-based hemostats accounted for the largest product share in 2023, representing approximately 28.9% of total market revenue.

- Formulation Segment Leadership: Matrix and gel hemostats emerged as the leading formulations in 2023, collectively capturing about 37.7% of the market, reflecting strong clinical adoption.

- Dominant Indication Segment: Surgical applications dominated the market landscape in 2023, contributing more than 61.4% of the overall market share.

- Key Application Area: Orthopedic surgery stood out as the primary application segment in 2023, accounting for over 38.6% of market demand.

- Major End-User Segment: Hospitals remained the largest end users of hemostats in 2023, holding a significant 49.2% market share due to high procedural volumes.

- Regional Market Leadership: North America led the global Hemostat Market in 2023 with a 48.1% share, supported by advanced healthcare infrastructure and a high prevalence of chronic conditions.

Hemostat Statistics

- Trauma-Related Bleeding Mortality: Uncontrolled bleeding accounts for approximately 43% of civilian trauma-related fatalities and nearly 90% of trauma-associated deaths in military environments, underscoring the critical need for effective hemostatic interventions.

- FDA Approvals Landscape: To date, 54 hemostatic agents have received approval from the U.S. Food and Drug Administration, reflecting sustained innovation and progress in bleeding management over the last six decades.

- Composition of Hemostatic Agents: Protein-based therapies, including fibrinogen, thrombin, and recombinant coagulation factors, represent nearly 89% of all FDA-approved hemostatic agents, highlighting their central role in current treatment strategies.

- Gene Therapy Advancements: Recent FDA approvals of gene therapies for Hemophilia A and Hemophilia B illustrate a significant shift toward long-term and potentially curative hemostatic treatment modalities.

- Primary Hemostasis Mechanism: Primary hemostasis is characterized by platelet adhesion and aggregation at the site of vascular injury, resulting in the formation of an initial platelet plug that limits blood loss.

- Secondary Hemostasis Process: Secondary hemostasis involves activation of the coagulation cascade, leading to fibrin mesh formation that stabilizes and reinforces the platelet plug to achieve durable bleeding control.

- Market Innovation Trends: The hemostat market is increasingly driven by advanced therapeutic approaches, with growing emphasis on recombinant proteins and gene-based therapies.

- Clinical Trial Focus: Cell and gene therapies constitute approximately 33.3% of active clinical trials within the hemostat segment, indicating strong research momentum toward next-generation treatment solutions.

- Routes of Administration: Intravenous delivery remains the dominant administration route, utilized by nearly 79% of approved hemostatic agents to ensure rapid systemic availability in acute care settings.

- Research and Development Activity: More than 550 active clinical trials are currently evaluating novel hemostatic agents, reflecting robust ongoing efforts to enhance treatment efficacy, safety, and clinical outcomes.

Regional Analysis

In 2023, North America maintained a dominant position in the global hemostats market, accounting for more than 48.1% of total revenue and generating approximately USD 1.33 Billion in market value. This leadership was supported by a high prevalence of chronic diseases, strong adoption of advanced medical technologies, and a well-established healthcare system. Within the region, the United States represented the primary market, followed by Canada, driven by high surgical volumes and robust hospital infrastructure.

Europe is expected to account for a substantial share of the global hemostats market, supported by an aging population, increasing numbers of surgical procedures, and rising healthcare expenditure. The region’s growth is led by United Kingdom, Germany, and France, which benefit from advanced healthcare systems and strong clinical adoption.

The Asia Pacific region is anticipated to witness the fastest growth, driven by a growing burden of chronic diseases, expanding patient populations, and ongoing improvements in healthcare infrastructure across emerging economies.

Latin America is projected to contribute a meaningful share to the global market, supported by rising healthcare investments, increasing chronic disease incidence, and infrastructure expansion, particularly in Brazil and Mexico.

Meanwhile, Middle East and Africa is expected to hold a comparatively smaller market share due to limited healthcare spending and infrastructure. However, increasing investments, improving access to care, and growing awareness of advanced medical technologies are expected to support gradual market growth over the forecast period.

Emerging Trends

- Surgical Bleeding Management: Hemostats are widely used when conventional methods such as sutures or ligatures are inadequate. Their application supports rapid hemostasis, reduces operative time, and lowers the risk of intraoperative and postoperative complications.

- Orthopedic Surgery Applications: In orthopedic procedures, hemostatic agents are essential for controlling bleeding from bone surfaces and surrounding soft tissues, enabling improved surgical visibility and supporting accelerated patient recovery.

- Cardiovascular Surgical Procedures: Hemostats play a critical role in cardiovascular surgeries by ensuring precise control of bleeding from blood vessels and cardiac tissues, thereby enhancing procedural safety and clinical outcomes.

- Trauma and Emergency Settings: In trauma care, hemostatic agents are used to rapidly control hemorrhage resulting from acute injuries, contributing to patient stabilization and reducing the risk of hemorrhagic shock.

- Gastrointestinal Surgical Interventions: Hemostatic sprays, powders, and gels are applied in gastrointestinal procedures to manage bleeding in anatomically challenging or minimally accessible areas, improving procedural efficiency and outcomes.

- Dental and Oral Surgeries: Hemostats are commonly utilized in dental procedures to control bleeding from gingival and oral tissues, supporting patient comfort and improving procedural effectiveness.

- Gynecological Surgical Use: In gynecological surgeries, hemostatic agents are employed to manage bleeding from delicate and highly vascular tissues, facilitating faster recovery and minimizing postoperative risks.

- Neurosurgical Procedures: During neurosurgery, hemostats enable precise bleeding control in the brain and spinal regions, where protection of critical structures is essential for patient safety.

- Plastic and Reconstructive Surgery: In cosmetic and reconstructive procedures, hemostatic agents help minimize bleeding, swelling, and bruising, contributing to improved aesthetic outcomes and higher patient satisfaction.

Frequently Asked Questions on Hemostat

- What is a hemostat and what is its primary function?

A hemostat is a medical device or material used to control bleeding by promoting blood clot formation. It is widely applied during surgical procedures, trauma care, and wound management to achieve rapid and effective hemostasis. - What are the main types of hemostats available?

Hemostats are broadly categorized into mechanical, active, passive, and flowable types. These products differ in composition and mechanism, including collagen, gelatin, cellulose, and thrombin-based formulations, depending on clinical application requirements. - In which medical procedures are hemostats commonly used?

Hemostats are commonly used in general surgery, cardiovascular surgery, orthopedic procedures, dental surgeries, and emergency trauma care. Their use is critical in reducing blood loss, improving surgical visibility, and minimizing postoperative complications. - How do topical hemostats differ from systemic agents?

Topical hemostats act locally at the bleeding site to accelerate clotting, while systemic agents influence the overall coagulation pathway through bloodstream circulation. Topical products are preferred due to targeted action and lower systemic risk. - Are hemostats safe for routine clinical use?

Hemostats are generally considered safe when used according to clinical guidelines. Regulatory approvals and extensive clinical testing ensure biocompatibility, controlled absorption, and minimal adverse reactions across a wide range of surgical and wound care settings. - What factors are driving growth in the hemostat market?

Market growth is primarily driven by rising surgical volumes, increasing trauma cases, and growing adoption of advanced wound care solutions. Technological advancements and expanding healthcare infrastructure in emerging economies further support sustained market expansion. - Which end-use segments dominate the hemostat market?

Hospitals represent the dominant end-use segment due to high surgical throughput and trauma admissions. Ambulatory surgical centers and specialty clinics are also gaining importance, supported by the global shift toward minimally invasive and outpatient procedures. - What regional trends are observed in the global hemostat market?

North America leads the market due to advanced healthcare systems and high procedure volumes. Asia-Pacific is experiencing rapid growth, supported by expanding medical tourism, improving healthcare access, and increasing investments in surgical care infrastructure.

Conclusion

The global hemostat market continues to demonstrate steady expansion, supported by rising surgical volumes, increasing trauma incidence, and a strong emphasis on effective blood loss management. Technological advancements, including recombinant proteins and gene-based therapies, are strengthening clinical outcomes and expanding treatment options.

Hospitals remain the primary end users, while orthopedic and surgical applications dominate demand. Regional leadership by North America reflects advanced healthcare infrastructure, whereas rapid growth in Asia Pacific highlights improving access to surgical care. Overall, sustained innovation and expanding clinical adoption are expected to support long-term market growth and improved patient safety.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)