Table of Contents

Overview

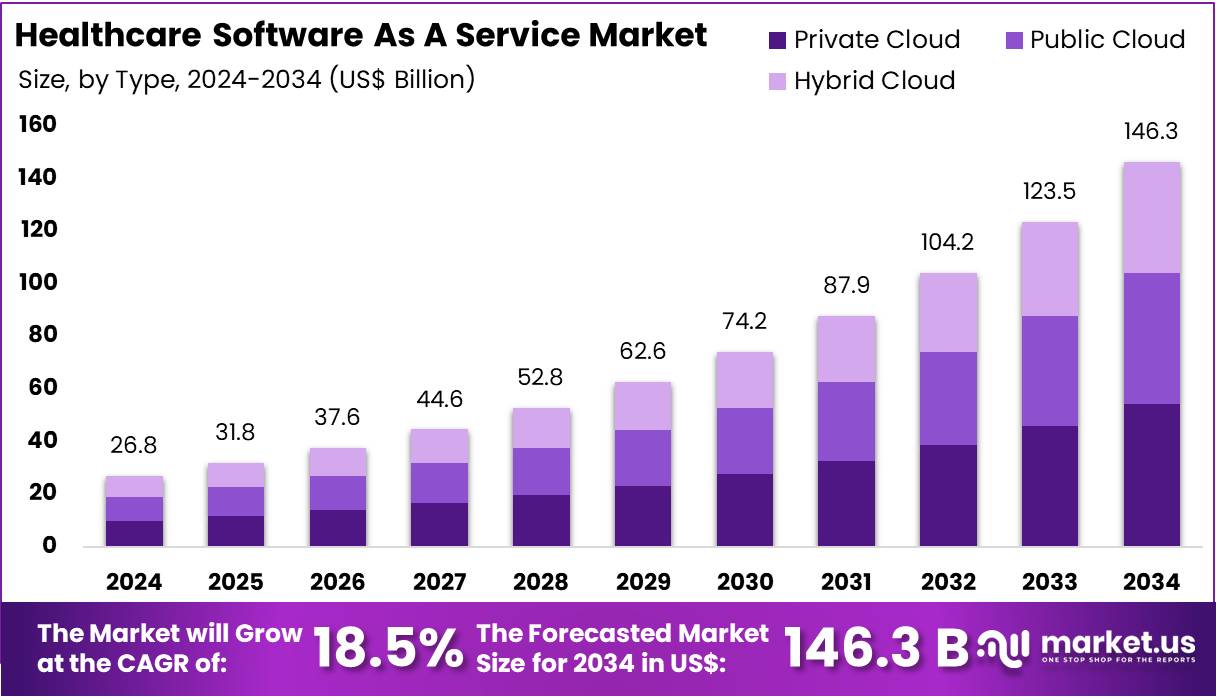

New York, NY – July 30, 2025 – The Global Healthcare Software As A Service Market Size is expected to be worth around US$ 146.3 Billion by 2034, from US$ 26.8 Billion in 2024, growing at a CAGR of 18.5% during the forecast period from 2025 to 2034.

The global Healthcare Software as a Service (SaaS) market is experiencing substantial growth, driven by the increasing demand for cloud-based platforms that enable real-time data access, remote monitoring, and enhanced care coordination.

Healthcare SaaS solutions are widely adopted across hospitals, clinics, diagnostic centers, and insurance providers due to their cost-effectiveness, ease of deployment, and scalability. These platforms support a range of functions including electronic health records (EHR), telemedicine, patient engagement, revenue cycle management, and clinical analytics. The shift toward value-based care and regulatory compliance requirements such as HIPAA and HL7 are further accelerating the adoption of cloud-based healthcare systems.

By deployment model, the market is segmented into public cloud, private cloud, and hybrid cloud, with the hybrid model gaining traction for its balanced approach to security and accessibility. North America currently dominates the market due to robust healthcare infrastructure and widespread cloud adoption, while Asia Pacific is expected to witness the fastest growth driven by digital health initiatives and expanding healthcare access. The Healthcare SaaS model is anticipated to play a critical role in modernizing healthcare delivery and enabling data-driven decision-making across care ecosystems.

Key Takeaways

- In 2024, the healthcare Software as a Service (SaaS) market generated a revenue of US$ 26.8 billion and is projected to reach US$ 146.3 billion by 2034, growing at a CAGR of 18.5% over the forecast period.

- Among solution types, Electronic Health Record (EHR) systems accounted for the largest share, representing 16.5% of the market in 2024.

- With regard to the deployment model, the Private Cloud segment led the market in 2024, capturing a 37.1% revenue share due to its enhanced data security and control features.

- By end-user, Healthcare Providers emerged as the dominant segment, generating the highest revenue share of 72.7% in 2024, reflecting strong adoption across hospitals, clinics, and specialty care facilities.

Segmentation Analysis

- Type Analysis: In 2024, Electronic Health Record (EHR) systems led the Healthcare SaaS market with a 16.5% share, driven by the global shift toward digital health infrastructure. These systems enhance care coordination by centralizing patient data, including diagnoses, treatments, and medications. Widespread adoption is evident in the U.S., where 88% of office-based physicians use EHRs. Cloud-based platforms, such as Epic’s “Garden Plot” and AI-integrated solutions from Oracle Health, are further accelerating adoption, particularly among small to mid-sized providers.

- Deployment Model Analysis: The private cloud segment held the largest revenue share of 37.1% in 2024, reflecting rising demand for secure and compliant data environments. Unlike public clouds, private cloud systems offer healthcare providers enhanced control over data storage, encryption, and access protocols critical under HIPAA and GDPR regulations. High-profile deployments, such as Rackspace’s private cloud-based Epic system for AdventHealth, demonstrate growing trust in private cloud solutions to support large-scale operations and integrate with other core digital health applications.

- End-User Analysis: Healthcare providers dominated the end-user segment in 2024 with a 72.7% revenue share, reflecting strong adoption of SaaS platforms for operational efficiency and clinical effectiveness. Hospitals, clinics, and independent practices are leveraging cloud-based EHRs and other tools to streamline workflows, improve care coordination, and meet regulatory requirements. The flexibility and scalability of SaaS are especially advantageous for smaller practices. Additionally, interoperability features are enabling seamless data exchange. Startups like RapidClaims further illustrate sector-wide investment in AI-driven SaaS innovations.

Market Segments

By Solution Type

- EHR Systems

- Telehealth

- Healthcare Data Analytics Tools

- Laboratory Information Systems (LIS)

- Medical Practice Management Systems

- Inventory and Material Management

- Supply Chain and Logistics Management

- Medical Billing

- HR & Workforce Management

- ePrescribing

- Others

By Deployment Model

- Private Cloud

- Public Cloud

- Hybrid Cloud

By End-User

- Healthcare Providers

- Hospitals & Clinics

- Diagnostic Centers

- Pharmacies

- Ambulatory Care Centers

- Others

- Healthcare Payers

- Private Payers

- Public Payers

Regional Analysis

North America Leads the Global Healthcare SaaS Market

In 2024, North America accounted for 43.4% of the global Healthcare SaaS market, maintaining its position as the leading regional segment. This dominance is supported by advanced healthcare infrastructure, high digital maturity, and stringent regulatory frameworks in countries such as the United States and Canada. The U.S., in particular, has shown strong uptake of cloud-based healthcare platforms including EHR systems, telemedicine applications, and patient management tools fueled by federal health IT incentives and a growing focus on cost-effective, outcome driven care.

Healthcare providers across the region are increasingly deploying SaaS solutions to streamline workflows, secure sensitive data, and enable personalized care through AI-driven analytics. For example, in January 2025, U.S.-based healthcare AI firm Innovaccer raised US$ 275 million in a Series F funding round. The investment is aimed at strengthening the company’s AI and cloud technology capabilities and expanding its portfolio with offerings in utilization management, clinical decision support, and care coordination.

Asia Pacific to Witness Fastest Growth During the Forecast Period

The Asia Pacific region is expected to register the highest compound annual growth rate (CAGR) in the Healthcare SaaS market, driven by accelerating digital healthcare transformation and expanding government support. Nations such as India, China, and Japan are promoting nationwide adoption of electronic medical records (EMRs), telehealth, and digital infrastructure as part of broader healthcare reforms.

Cloud computing is enabling small- and medium-sized healthcare providers in countries like India to adopt scalable SaaS platforms without significant capital investment. This is especially critical in managing the healthcare needs of growing and aging populations. The region’s momentum is further supported by rising private sector investments in health tech innovation.

In April 2025, HealthMetrics launched HealthMetrics Indonesia following its acquisition of Across Asia Assist (AAA) Indonesia in 2022. This integration combines HealthMetrics’ digital capabilities with AAA’s established market presence to form a tech-enabled third-party administrator (TPA) for healthcare services. Through tools such as the HealthMetrics Cloud Platform, Global Member App, and International Assistance Hub, the initiative aims to enhance digital healthcare administration and service delivery in Southeast Asia.

Emerging Trends

- Near-Universal Adoption of Cloud-Based EHR Systems: The adoption of cloud-based electronic health record (EHR) systems has reached near-universal levels among U.S. providers. As of 2021, 96% of non-federal acute care hospitals and 78% of office-based physicians were using certified EHRs, most of which are delivered via SaaS platforms. This widespread uptake can be attributed to incentives for digital health, reductions in on-premises IT costs, and enhanced data backup and recovery capabilities.

- Rapid Expansion of Interoperability via APIs and FHIR: Standards-based application programming interfaces (APIs), particularly those using the FHIR specification, are being integrated at scale. In 2022, 69% of non-federal acute care hospitals reported using standards-based APIs to enable patient access, and two-thirds of hospitals had implemented FHIR APIs a 12-point increase over the prior year. This trend is driven by regulatory requirements under the 21st Century Cures Act and by providers’ need for seamless data exchange across care settings.

- Stabilization and Integration of Telehealth Platforms: Following the peak adoption during the COVID-19 pandemic, telehealth usage has stabilized but remains an integral SaaS offering. In 2022, 36.0% of adults covered by Medicare and Medicaid and 29.7% covered by private insurance used telemedicine services. The persistence of these levels indicates that telehealth SaaS solutions have become entrenched components of care delivery, particularly for chronic disease management and follow-up visits.

- Expansion of Patient Engagement and Access Tools: Patient portals and mobile health apps delivered as SaaS are increasingly prevalent. Nearly three-quarters of hospitals using certified health IT report that they provide patients with electronic access through apps, enabling appointment scheduling, secure messaging, and viewing of test results. These tools have been attributed to improvements in patient satisfaction and self-management of health conditions.

- Growing Participation in National Data Networks (TEFCA): Participation in trusted exchange frameworks has risen steadily. In 2023, over 60% of U.S. hospitals were aware of and planned to participate in the Trusted Exchange Framework and Common Agreement (TEFCA), up from 51% in 2022. This indicates that SaaS solutions are being extended to support broader health information exchange across organizations and regions.

Use Cases

- Cloud-Hosted EHR and Practice Management: Nearly 96% of hospitals and 78% of office-based physicians rely on cloud-hosted EHR systems for patient record management, order entry, and billing functions. The SaaS delivery model has been credited with reducing initial infrastructure costs by up to 30% and shortening deployment times from years to months.

- Telemedicine Platforms: Telehealth SaaS platforms facilitated 36.0% of visits among Medicare and Medicaid beneficiaries in 2022. By enabling video visits, remote monitoring, and virtual check-ins, these solutions have supported an estimated 50 million telehealth encounters in 2022 alone, preserving continuity of care during public health emergencies and beyond.

- API-Enabled Patient Portals: Approximately 75% of hospitals deliver patient portal access through API-driven apps. These portals serve over 100 million active users nationwide, allowing patients to view lab results, request prescription refills, and communicate securely with providers. The result has been a 20–25% increase in patient portal engagement year over year.

- Interoperability and Data Exchange: Two-thirds of acute care hospitals implemented FHIR APIs by 2022, representing a year-over-year growth of 12 percentage points. These APIs are used for data exchange with external care partners, mobile health apps, and population health systems, supporting over 200 million data transactions per month. This contributes to reduced information blocking and improved care coordination.

- Participation in TEFCA-Compliant Networks: Over 60% of hospitals planned to join TEFCA by 2023, up from 51% in 2022. SaaS offerings for national network connectivity have enabled hospitals to share patient summaries and discharge records across state lines, with pilot programs reporting a 15% reduction in redundant imaging and lab tests.

Conclusion

The global Healthcare SaaS market is poised for transformative growth, underpinned by the rapid adoption of cloud-based solutions that enhance clinical efficiency, data accessibility, and patient engagement. Driven by increasing regulatory requirements, technological innovation, and shifting care delivery models, SaaS platforms are becoming integral to healthcare operations across regions.

With strong uptake in North America and accelerating expansion in Asia Pacific, the market is supported by robust investments and public health initiatives. As interoperability, security, and digital health capabilities continue to evolve, Healthcare SaaS is expected to play a central role in shaping the future of global healthcare systems.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)