Table of Contents

Overview

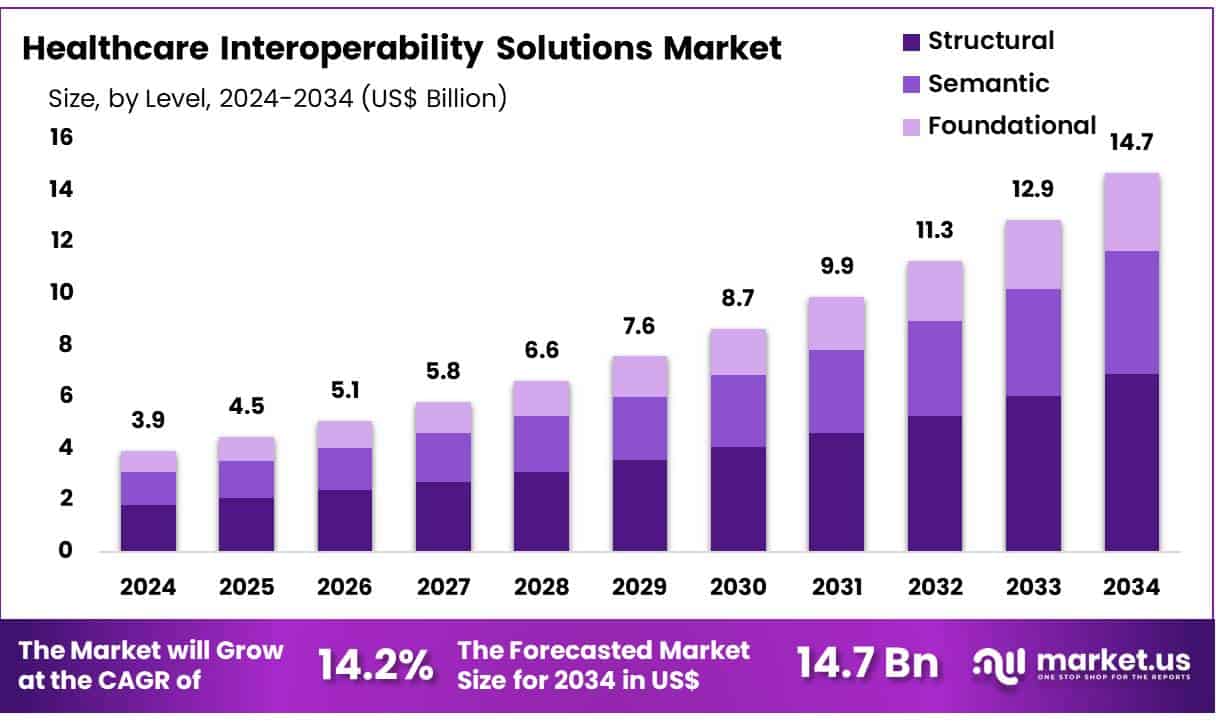

New York, NY – June 11, 2025 – Global Healthcare Interoperability Solutions Market size is expected to be worth around US$ 14.7 billion by 2034 from US$ 3.9 billion in 2024, growing at a CAGR of 14.2% during the forecast period 2025 to 2034. In 2023, North America led the market, achieving over 41.6% share with a revenue of US$ 1.6 Billion.

The global market for healthcare interoperability solutions is experiencing robust growth, driven by the increasing demand for seamless health data exchange, rising adoption of electronic health records (EHRs), and a growing emphasis on patient-centered care. Interoperability solutions enable healthcare systems, hospitals, and providers to efficiently share and interpret data across diverse digital platforms, improving care coordination and clinical outcomes.

As healthcare systems shift toward value-based care models, the need for real-time access to comprehensive patient data has accelerated. Regulatory initiatives such as the U.S. 21st Century Cures Act and global digital health strategies are further promoting interoperability across public and private health systems. Hospitals, diagnostic labs, and payers are increasingly investing in interface engines, health information exchanges (HIEs), and integration platforms to streamline operations and reduce administrative burden.

Cloud-based interoperability solutions are witnessing particularly strong uptake due to their scalability, security features, and cost-efficiency. North America continues to lead the global market, while Asia-Pacific shows rising potential with digital transformation efforts in countries such as India, China, and Australia. The continued integration of AI, FHIR (Fast Healthcare Interoperability Resources), and blockchain technologies into interoperability platforms is expected to enhance data accuracy, reduce redundancy, and support predictive healthcare delivery.

Key Takeaways

- In 2024, the global healthcare interoperability solutions market generated a revenue of US$ 3.9 billion and is projected to reach US$ 14.7 billion by 2034, expanding at a compound annual growth rate (CAGR) of 14.2% over the forecast period.

- By product type, the market is bifurcated into solutions and services, with the services segment leading in 2023, accounting for a 57.3% share of the global revenue.

- Based on interoperability level, the market is segmented into foundational, structural, and semantic. The structural level emerged as the dominant category, capturing a 46.8% share.

- In terms of application, the market is categorized into diagnosis, treatment, and others. The diagnosis segment held the highest share in 2023, contributing 49.5% of the total market revenue.

- Regarding deployment mode, the market is classified into cloud-based and on-premise models. The on-premise segment led with a 52.6% share, reflecting continued reliance on localized infrastructure.

- By end user, the market includes hospitals, ambulatory surgical centers, and others. Hospitals dominated the market, securing a 58.2% share due to their large-scale adoption of integrated healthcare systems.

- Regionally, North America accounted for the highest revenue share of 41.6% in 2023, driven by strong regulatory mandates and advanced digital infrastructure.

Segmentation Analysis

- Product Type Analysis: In 2023, the services segment led the healthcare interoperability solutions market, accounting for 57.3% of the share. This dominance is driven by rising demand for consulting, integration, and managed services as healthcare providers seek streamlined operations and improved care coordination. Increasing IT complexity and regulatory compliance needs are fueling reliance on third-party service providers. System implementation and ongoing support are projected to remain essential as healthcare organizations pursue large-scale digital transformation initiatives.

- Level Analysis: Structural interoperability held a significant 46.8% market share due to its role in enabling standardized healthcare data exchange. The segment’s growth is driven by the increasing adoption of electronic health records (EHRs) and the need to integrate data from varied systems. Regulatory pressures encouraging standardized coding and reporting formats are accelerating adoption. Structural interoperability enhances care coordination and administrative efficiency, making it a strategic priority for healthcare systems undergoing digital modernization.

- Application Analysis: The diagnosis segment accounted for 49.5% of the market share, driven by growing demand for accurate and timely diagnostic information. Interoperability solutions help unify diagnostic data from labs, imaging centers, and EHRs to support better clinical decisions. With the increasing use of AI and personalized medicine, seamless access to diagnostic data is becoming essential. This integration improves outcomes and supports precision healthcare, fueling continued investment in interoperable platforms for diagnostic applications.

- Deployment Analysis: On-premise deployment dominated the market with 52.6% share, favored by healthcare organizations requiring enhanced data control and regulatory compliance. Facilities managing large volumes of sensitive patient data prefer on-premise systems for their ability to ensure security, especially in alignment with HIPAA and other regional privacy laws. Additionally, areas with limited internet infrastructure continue to rely on locally hosted solutions. This segment is expected to sustain growth as security and customization remain top priorities.

- End-user Analysis: Hospitals emerged as the leading end-user segment with a 58.2% share, driven by efforts to optimize patient care, manage complex workflows, and improve data accessibility. The increasing burden of chronic diseases and the need for coordinated long-term care amplify the importance of interoperability. Hospitals are also at the forefront of adopting digital infrastructure to ensure cross-departmental data flow. These factors collectively contribute to hospitals maintaining a dominant role in the interoperability market.

Market Segments

By Product Type

- Solutions

- HIE Interoperability

- Enterprise Interoperability

- EHR Interoperability

- Others

- Services

By Level

- Structural

- Semantic

- Foundational

By Application

- Diagnosis

- Treatment

- Others

By Deployment

- Cloud Based

- On-premise

By End-user

- Hospitals

- Ambulatory Surgical Centers

- Others

Regional Analysis

North America Leads the Healthcare Interoperability Solutions Market

North America accounted for the largest share of the healthcare interoperability solutions market, holding 41.6% of global revenue. This dominance is primarily driven by the widespread adoption of electronic health records (EHRs) and health information exchanges (HIEs), which have significantly improved data sharing among healthcare providers. According to the U.S. Food and Drug Administration (FDA), nearly half of Americans now utilize FDA-approved digital health applications to manage personal healthcare.

Government-backed initiatives by the Centers for Medicare & Medicaid Services (CMS) have further strengthened interoperability by encouraging data integration to enhance care quality and reduce healthcare costs. The American Telemedicine Association (ATA) highlighted that telehealth usage remains 38 times higher than pre-pandemic levels, reinforcing the critical role of interoperable systems in supporting virtual healthcare services. These factors, along with a growing focus on value-based care, are driving the region’s continued market leadership.

Asia Pacific Expected to Witness the Fastest Growth

The Asia Pacific region is projected to experience the highest compound annual growth rate (CAGR) in the healthcare interoperability solutions market over the forecast period. This growth is attributed to the region’s aging population and rising incidence of chronic diseases. The National Bureau of Statistics of China estimates that by 2024, individuals aged 60 and above will comprise 21.1% of the country’s population, intensifying the demand for effective healthcare services.

Furthermore, the region is undergoing rapid digital transformation in healthcare. The World Health Organization (WHO) has observed a sharp increase in digital health initiatives aimed at enhancing healthcare accessibility. In India, the National Digital Health Mission (NDHM) is actively working to build an integrated digital health infrastructure, laying the groundwork for the adoption of interoperability standards. As providers adopt integrated care delivery models, the demand for efficient data exchange systems will accelerate, contributing to robust market expansion across Asia Pacific.

Emerging Trends

- Expansion of Core Data Standards: The United States Core Data for Interoperability (USCDI) was updated to version 5 on July 16, 2024, adding 16 new data elements and two new data classes. This expansion has been driven by a need to include critical information such as social determinants of health and genomics within standardized exchange formats, thereby enabling richer, more actionable data sharing across systems.

- Wider Hospital Engagement: Engagement in all four domains of interoperable exchange sending, receiving, finding, and integrating patient information rose from 46 percent in 2018 to 70 percent in 2023, representing a 52 percent increase in hospital capability. This growth has been attributed to federal incentives and stricter “information-blocking” rules under the 21st Century Cures Act, which have lowered technical and policy barriers to data sharing.

- Integration of Remote and Wearable Technologies: Technological innovations such as wearable sensors, remote monitoring devices, and telehealth platforms have been highlighted in ONC’s “10-Year Vision” as key enablers of at-home and virtual care models. By standardizing the way these devices communicate often via FHIR-based APIs interoperability has been extended beyond traditional EHRs into patient-generated health data, supporting continuous care outside clinical settings.

- Federal LEAP Projects Driving Standards and Tools: Under the “LEAP in Health IT” initiative, federal grants have been used to develop and pilot new interoperability standards, open-source tools, and implementation guides. These projects are intended to advance care delivery and research capabilities by creating reusable components such as test data sets and sandbox environments that can be adopted by health systems nationwide.

Use Cases

- Automated ADT Alerting: Automated Admission, Discharge, and Transfer (ADT) alerts have been implemented in state and regional Health Information Exchanges (HIEs) to notify care teams in real time when a patient moves between settings. High-value ADT use has been promoted by ONC fact sheets, helping to reduce readmissions and ensure timely follow-up care across networks.

- Electronic Laboratory Reporting (ELR): By FY 2019, nearly 90 percent of laboratory reports for state-reportable conditions were being received electronically by public health agencies a substantial increase from earlier years. This shift has improved the timeliness and completeness of data for outbreak detection and case management, enabling more rapid public health responses.

- Immunization Information Systems (IIS): Interoperable IIS have achieved national coverage rates of 98 percent for children under 6 years in 2022 and 100 percent in 2023 (excluding U.S. territories). These systems allow providers and public health officials to query vaccination records in real time, supporting vaccine campaign planning and reducing missed or duplicated immunizations.

- FHIR®-Enabled Patient Apps: More than two-thirds of U.S. hospitals reported use of HL7® Fast Healthcare Interoperability Resources (FHIR®) APIs in 2022 to enable patient access to their own health data through mobile and web applications. Such APIs support patient engagement, remote monitoring, and the integration of third-party wellness and chronic-care management tools into clinical workflows.

Conclusion

The healthcare interoperability solutions market is undergoing significant transformation, supported by technological advancements, regulatory frameworks, and increasing demand for integrated care delivery. The market’s growth is underpinned by the expansion of digital health strategies, real-time data sharing, and adoption of cloud-based platforms.

With strong leadership from North America and rapid growth in Asia Pacific, the industry is poised for sustained expansion. Trends such as FHIR adoption, federal initiatives, and patient-driven technologies are shaping the future landscape. These developments collectively reinforce the essential role of interoperability in improving clinical outcomes, operational efficiency, and patient-centered care across global healthcare systems.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)