Table of Contents

Overview

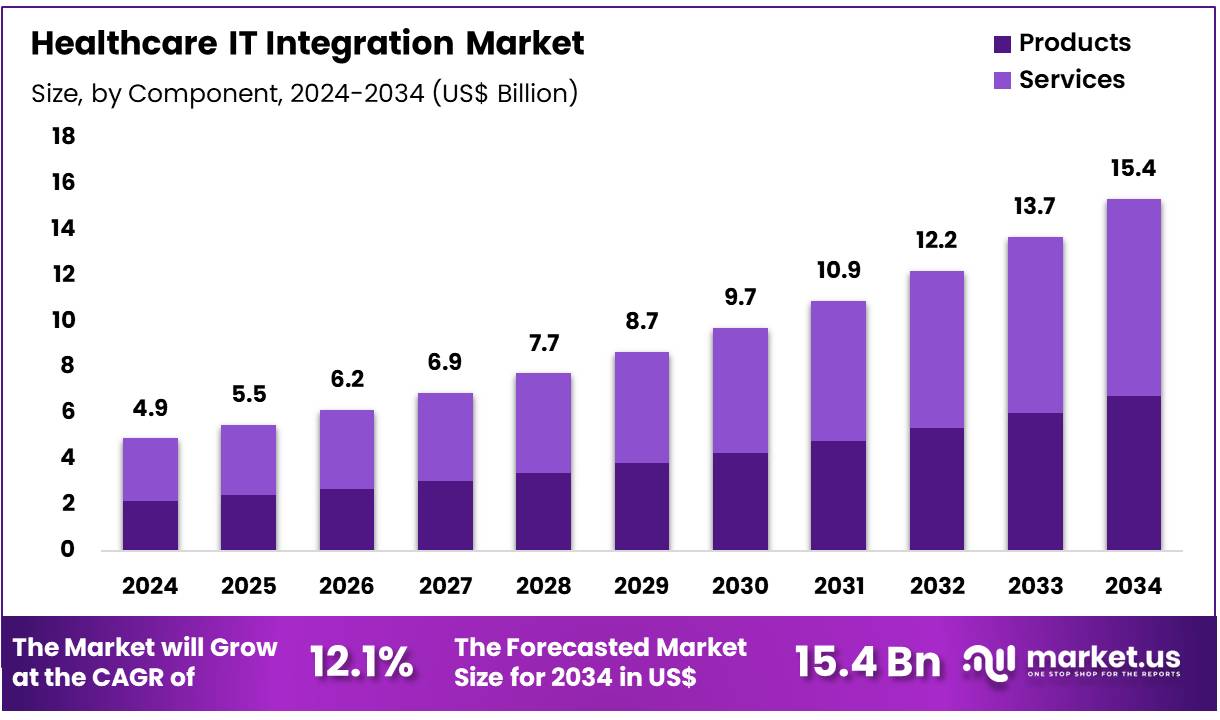

New York, NY – Dec 03, 2025 – Global Healthcare IT Integration Market size is expected to be worth around US$ 15.4 Billion by 2034 from US$ 4.9 Billion in 2024, growing at a CAGR of 12.1% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 41.6% share with a revenue of US$ 2.0 Billion.

The global healthcare IT integration market has been experiencing stable expansion, driven by the increasing adoption of digital health systems and the rising need for streamlined clinical workflows. The growth of the market can be attributed to the rapid shift toward electronic health records (EHRs), the expansion of telehealth platforms, and the rising emphasis on interoperability across healthcare settings. A consistent demand for integrated solutions has been observed, as hospitals and clinics prioritize efficient data exchange to enhance patient outcomes.

Strong investment in healthcare digitalization has supported market adoption, while regulatory encouragement for standardized data formats has accelerated integration efforts. The deployment of cloud-based healthcare IT solutions has further strengthened system scalability and facilitated cost-efficient information management. It has been reported that integration platforms improve operational efficiency by reducing administrative burdens and enabling real-time access to patient information.

The market has been positively influenced by the rising incidence of chronic diseases, which has increased the requirement for coordinated care. Advanced analytics, AI-enabled decision support, and remote patient monitoring are being incorporated into integrated systems to support clinical accuracy and continuity of care.

North America has been leading the market due to established healthcare infrastructure, while Asia-Pacific has been witnessing notable growth driven by digital health initiatives. Overall, the healthcare IT integration market is expected to maintain steady momentum as healthcare providers continue to prioritize connected, interoperable, and data-driven ecosystems.

Key Takeaways

- The global healthcare IT integration market is projected to reach US$ 15.4 Billion by 2034, increasing from US$ 4.9 Billion in 2024.

- The market is anticipated to expand at a CAGR of 12.1% during the forecast period 2025–2034.

- Services represent 56.1% of the overall market share, indicating their essential function in supporting interoperability, connectivity, and secure data exchange across healthcare environments.

- The on-premise deployment mode holds a dominant 63.5% share, demonstrating the continued preference of healthcare institutions for internal infrastructure and controlled data management.

- The EHR application segment leads the market with a 39.7% share, underscoring its core importance in enhancing patient data accessibility, coordinated care, and adherence to regulatory standards.

- Large enterprises account for 68.8% of the market, reflecting their extensive adoption of integrated IT solutions and capacity for advanced digital infrastructure investments.

- Hospitals and clinics constitute the primary end-user group, commanding a 67.0% share due to their high demand for integrated, efficient, and interoperable healthcare systems.

- In 2024, North America remained the leading regional market with a 41.6% share and revenue reaching US$ 2.0 Billion.

Regional Analysis

North America Continues to Lead the Healthcare IT Integration Market

North America has been maintaining its leading position in the healthcare IT integration market, securing 41.6% of total revenue, supported by the region’s strong focus on interoperability and efficient data exchange across diverse healthcare systems. Regulatory emphasis on improving patient outcomes through enhanced information sharing has strengthened this leadership.

The U.S. Department of Health & Human Services (HHS) continues to prioritize seamless data access, while the Office of the National Coordinator for Health Information Technology (ONC) drives national interoperability initiatives. The implementation of the 21st Century Cures Act, which encourages the use of open APIs, has further supported transparent and secure data sharing. High adoption rates of Electronic Health Records (EHRs) among U.S. physicians have also created a solid foundation for advanced integration solutions.

Asia Pacific Expected to Record the Fastest Growth Rate

The Asia Pacific region is projected to achieve the highest CAGR during the forecast period, driven by expanding government efforts to digitize healthcare systems and enhance the efficiency of service delivery. Multiple countries are implementing national digital health programs that rely on strong integration frameworks. Progress in establishing national health information exchanges reflects the region’s growing commitment to interoperable health ecosystems.

Rising EHR adoption and ongoing efforts to achieve universal health coverage are contributing to the demand for platforms capable of connecting heterogeneous IT systems. Additionally, an increase in healthcare collaborations and public–private partnerships across the region has created a stronger need for effective data integration to support coordinated and high-quality care.

Emerging Trends

- A substantial rise in hospital-to-hospital information exchange has been recorded. In 2022, 85% of U.S. hospitals reported electronically querying or locating patient health information through multiple networks, compared with 78% in 2021. In parallel, 64% of hospitals were using national networks in 2021 to send and receive summary-of-care records, indicating a steady shift toward more seamless and interoperable data exchange across care environments.

- Adoption of open, API-based standards has accelerated following recent federal regulation. The CMS Interoperability and Patient Access Final Rule, implemented six months earlier, requires health systems to deploy standardized and publicly accessible APIs that enable real-time access to comprehensive electronic health records for patients and providers. The mandate was established to eliminate technical barriers and enhance patient access to clinical information.

- Distributed data networks built around common data models (CDMs) are becoming fundamental to safety surveillance and clinical research. In January 2025, new HHS guidance emphasized increasing reliance on distributed networks that integrate EHR and claims data through CDMs. These networks have been utilized to support near-real-time detection of medical product safety signals across multiple sites.

- Modernization of public health reporting is progressing through large-scale investment in automated case reporting. Supported by a $200 million CARES Act award, 64 state and local jurisdictions have begun adopting HL7-based electronic case reporting within surveillance systems to automate real-time transmission of reportable conditions from EHRs to public health agencies. Initial outcomes suggest faster case identification and improved timeliness in public health response efforts.

Use Cases

- Transition-of-Care Automation: Automation of transitions of care has been strengthened through integrated health information exchanges capable of transmitting summary-of-care documents when patients move between care settings, such as from hospitals to rehabilitation facilities. In 2021, 64% of U.S. hospitals used national exchange networks for this purpose, while 50% of physicians electronically queried patient histories prior to initial visits. These capabilities reduce manual chart retrieval and support continuity of care.

- Medical Product Safety Surveillance: Distributed data networks standardized through CDMs are being applied to monitor adverse events. In early 2025, participating health systems within a CDM-enabled network detected a safety signal for a newly marketed medication within two weeks of widespread use. The integration of EHR and claims data supports timely identification of safety concerns across varied patient populations.

- Electronic Laboratory Reporting for Outbreak Response: During infectious disease outbreaks, laboratories employ electronic laboratory reporting (ELR) to transmit test results directly to public health authorities. As of April 2024, 90% of CDC laboratories were electronically sharing data with state and local health departments. This infrastructure improves situational awareness and strengthens the timeliness of outbreak response activities.

- Automated Case Reporting in Public Health Surveillance: Electronic case reporting (eCR) systems automatically extract reportable disease data from EHRs and transmit it to public health agencies without manual intervention. Supported by a $200 million HHS data modernization initiative, 64 jurisdictions implemented HL7 eCR standards for COVID-19 surveillance. Early assessments indicate a 30% reduction in reporting delays, improving outbreak monitoring and enabling more efficient resource allocation.

Frequently Asked Questions on Healthcare IT Integration

- Why is Healthcare IT Integration important?

The importance of healthcare IT integration is driven by the need for accurate data flow, reduced clinical errors, and optimized resource utilization. Integrated systems ensure timely information access for providers, resulting in improved patient outcomes and strengthened institutional efficiency across healthcare environments. - What technologies are used in Healthcare IT Integration?

Key technologies used include electronic health records, health information exchanges, cloud platforms, middleware solutions, application programming interfaces, and interoperability standards like HL7 and FHIR. These tools enable real-time data sharing, consistent communication, and secure connectivity among diverse healthcare systems. - How does Healthcare IT Integration support hospitals and clinics?

Hospitals and clinics benefit through streamlined workflows, improved information accuracy, reduced administrative burdens, and better resource management. Integrated systems also enhance operational transparency, enabling providers to deliver coordinated care while reducing delays caused by fragmented or inconsistent data sources. - What role does interoperability play in Healthcare IT Integration?

Interoperability ensures different healthcare applications communicate effectively, enabling standardized, secure, and reliable data exchange. It forms the foundation of integration, allowing diverse systems to work collectively and supporting improved clinical decisions, operational efficiency, and regulatory compliance across healthcare environments. - What is driving growth in the Healthcare IT Integration Market?

Growth is being driven by increasing digitalization, demand for interoperable solutions, expansion of telehealth, and rising healthcare data volumes. Regulatory mandates promoting data exchange and patient safety further strengthen market adoption across both developed and emerging healthcare systems. - Which regions dominate the Healthcare IT Integration Market?

North America dominates due to advanced healthcare infrastructure, strong regulatory support, and significant adoption of electronic health systems. Europe follows with extensive digitalization initiatives, while Asia-Pacific is experiencing rapid growth driven by expanding healthcare facilities and government-led modernization programs. - Who are the main end users of Healthcare IT Integration solutions?

Major end users include hospitals, diagnostic laboratories, clinics, and healthcare payers. These institutions adopt integration solutions to improve data management, streamline workflows, enhance compliance, and support high-quality patient care across increasingly digital healthcare environments. - How is the rise of telehealth affecting the Healthcare IT Integration Market?

The rise of telehealth is increasing demand for integrated platforms that support remote monitoring, virtual consultations, and secure data exchange. This trend strengthens the need for interoperable solutions, improving digital care delivery and expanding integration opportunities across healthcare ecosystems.

Conclusion

The global healthcare IT integration market is expected to maintain steady progression as healthcare systems continue to transition toward fully connected and data-driven environments. Growth is being supported by rising EHR adoption, strong regulatory encouragement for interoperability, and increasing dependence on cloud-based and API-enabled platforms.

The expanding burden of chronic diseases and rapid development of digital health ecosystems further reinforce demand for integrated solutions. North America remains the dominant region, while Asia-Pacific is projected to accelerate rapidly. Overall, sustained investment in digital infrastructure and coordinated care models will continue to drive long-term market expansion.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)