Table of Contents

Overview

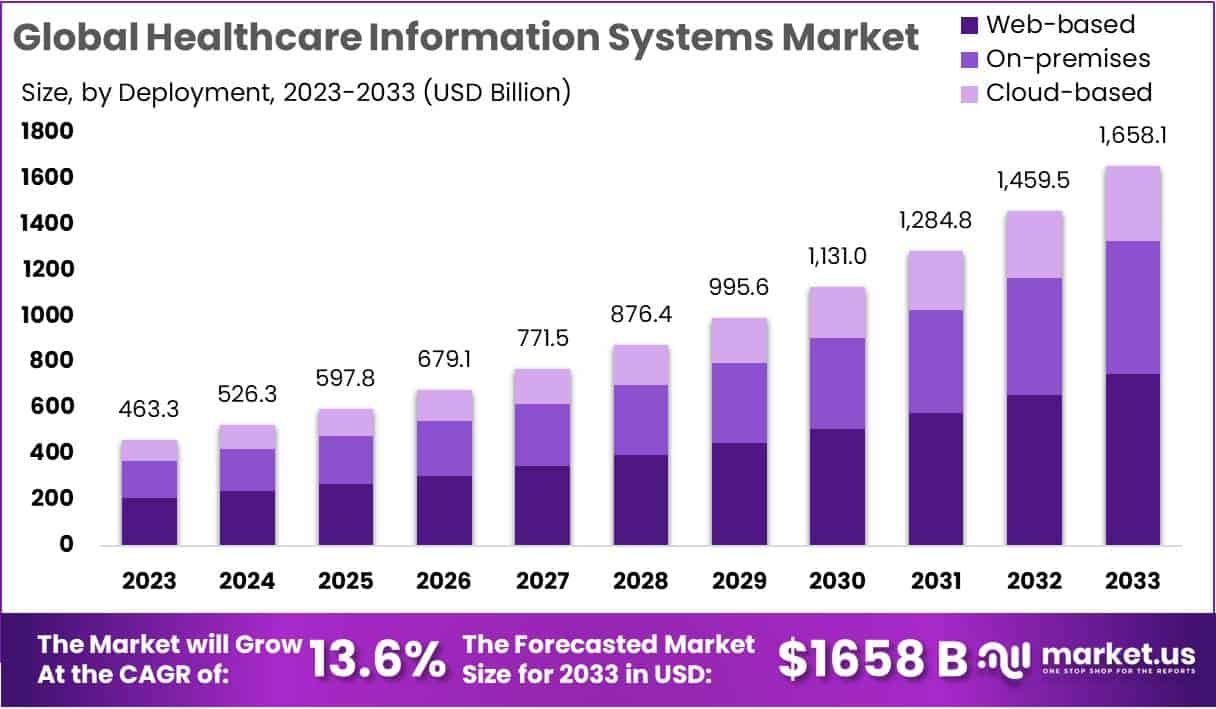

The Global Healthcare Information Systems Market is projected to grow strongly in the coming decade. It is expected to reach US$ 1658.1 billion by 2033, up from US$ 463.3 billion in 2023, expanding at a CAGR of 13.6% from 2024 to 2033. Growth is driven by rising demand for digital health, government initiatives, and the increasing role of data in modern healthcare. National policies and global frameworks are reinforcing investment in interoperable platforms and patient-centric solutions.

Governments and health agencies are pushing digital health strategies at scale. The World Health Organization’s Global Strategy on Digital Health (2020–2025) has urged countries to develop national plans, allocate budgets, and build digital capacity. This has signaled that technology and data are now considered essential parts of healthcare systems. As a result, many countries are aligning resources and long-term strategies with this direction, creating a durable foundation for market expansion.

Formal regulations are accelerating adoption. In the United States, the 21st Century Cures Act and related CMS rules mandate secure data sharing and patient access through APIs. In Europe, the creation of the European Health Data Space is enabling seamless cross-border use of electronic health records and health data for care and research. These measures are driving strong demand for compliance tools, APIs, and interoperable hospital systems.

Demographic shifts further reinforce this trend. According to the United Nations, the global share of individuals aged 65 and older is increasing rapidly. Older populations typically use more health services and require coordinated, data-driven care for chronic conditions. To manage multi-morbidity and complex care at scale, healthcare systems are upgrading their information infrastructure. This demographic shift is a key structural driver that ensures sustained demand for connected records, analytics, and digital care management platforms.

Disease Burden, Technology Advances, and Standards Evolution

Chronic diseases are placing persistent strain on healthcare systems worldwide. The World Health Organization estimates that noncommunicable diseases account for nearly three-quarters of global deaths. Managing conditions such as cardiovascular disease, cancer, diabetes, and chronic lung disorders requires long-term tracking, registries, and collaborative care models. Health information systems are central to enabling this with structured data, alerts, and decision-support tools.

Technology advances are strengthening the foundation for adoption. The World Bank notes that broadband coverage has expanded across many regions, reducing barriers to digital solutions. While the digital divide persists, connectivity improvements allow wider use of electronic health records, telehealth, and patient portals. This is particularly relevant in emerging markets where infrastructure gains are most visible, boosting software demand in both clinical and community health settings.

Adoption data confirm steady progress, though gaps remain. OECD reporting shows that electronic health records are widely used across member states, but national fragmentation and uneven standards still limit interoperability. At the same time, more citizens are actively seeking health information online, which raises expectations for digital services. This trend pushes providers to expand their digital capabilities, thereby accelerating market growth.

Finally, maturing standards are lowering integration costs and improving outcomes. The WHO’s ICD-11 classification, introduced globally in 2022, is a digital-first coding framework with APIs and modern tools. It supports better analytics, billing accuracy, and safety reporting. Countries upgrading to ICD-11 often invest simultaneously in broader interoperability projects, boosting overall spending on healthcare IT. Development partners and ministries of health also view digital transformation as essential for efficiency and equity, channeling funds toward national platforms. This ensures a long-term, sustainable growth trajectory for the healthcare information systems market.

Key Takeaways

- The Healthcare Information Systems Market is anticipated to achieve US$ 1658.1 billion by 2033, advancing at a strong CAGR of 13.6%.

- Web-based deployment accounts for 45.1% market share, owing to its accessibility, user-friendly interface, and efficiency in streamlining healthcare workflows.

- The Services segment dominates with 48% market share, providing essential solutions like implementation, consulting, support, and training across healthcare organizations.

- Hospitals represent the leading end-user segment with 77.4% market share, highlighting their reliance on advanced information systems for efficient patient care.

- Market growth is fueled by digital transformation, widespread adoption of data analytics, and supportive government initiatives targeting healthcare modernization.

- Cloud-based solutions gain traction, offering healthcare providers scalability, flexibility, and cost-effectiveness, reinforcing a significant industry trend.

- North America leads with 54.8% market share in 2023, driven by rapid technological adoption and continuous healthcare IT innovations.

- Asia Pacific emerges as the fastest-growing region, propelled by government healthcare spending, infrastructure improvements, and rising demand for healthcare IT solutions.

- Strategic mergers and acquisitions, including Teladoc’s acquisition of Livongo and Allscripts’ $28 billion purchase of Cerner, demonstrate industry consolidation and expansion.

Regional Analysis

North America dominated the healthcare information systems market in 2023, securing a 54.8% share with a market value of USD 253.8 billion. This strong position reflects the region’s robust healthcare infrastructure and rapid adoption of advanced technologies. The region’s proactive initiatives in digitizing healthcare processes further supported its growth. Investments in cutting-edge solutions have reinforced North America’s leadership, making it the key region influencing global healthcare IT developments and setting benchmarks for innovation in medical information systems.

The region’s dominance is underpinned by a strategic focus on digital healthcare transformation. Hospitals and healthcare providers in North America have increasingly integrated advanced information systems to enhance efficiency and accuracy. This trend has improved patient care delivery while streamlining operational processes. The emphasis on regulatory compliance and data management also accelerated adoption. These collective efforts have ensured that North America remains at the forefront of global healthcare technology, positioning it as a trendsetter in this highly competitive market.

Asia Pacific is identified as the fastest-growing regional market for healthcare information systems. Government initiatives and increased healthcare spending in developing nations are driving adoption of IT-based healthcare solutions. Improvements in infrastructure and digital integration have also enhanced demand for healthcare IT services. Providers are seeking solutions that improve workflow efficiency while reducing medical costs, creating significant opportunities in the region. With rapid advancements and increasing policy support, Asia Pacific is expected to remain the leading growth hub, reshaping the global healthcare information systems landscape.

Segmentation Analysis

In 2023, the Revenue Cycle Management (RCM) segment held a commanding share of over 65.8% in the healthcare information systems market. Its dominance is explained by its critical role in streamlining financial operations across healthcare providers. The Hospital Information System (HIS) also contributed significantly by enabling smoother communication and coordination within hospital departments. Similarly, the Electronic Health Record (EHR) and Electronic Medical Record (EMR) segments demonstrated notable growth. These systems improved accessibility, accuracy, and organization of patient data, making them indispensable in modern healthcare operations.

The market also experienced rising adoption of real-time healthcare solutions. These systems provided immediate data updates, ensuring faster and more effective clinical decisions. Their agility helped improve patient outcomes and overall operational efficiency. Patient Engagement Solutions further gained traction by enhancing communication between providers and patients. By involving patients in their care, these solutions promoted better adherence and satisfaction. Other emerging systems also attracted attention, focusing on solving targeted challenges and strengthening the wider healthcare delivery ecosystem.

From a deployment perspective, web-based systems led with a 45.1% market share in 2023. Their flexibility, cost-effectiveness, and ease of access across locations supported faster adoption. On-premises deployment remained relevant, particularly among organizations prioritizing control and data security. Despite its traditional nature, it served as a reliable and customizable option. Cloud-based systems displayed robust growth potential, benefiting from scalability, cost savings, and collaborative functions. With increasing adoption, the cloud model emerged as a key avenue for future innovation and long-term expansion in healthcare information systems.

In terms of components, services dominated with over 48% market share in 2023. Implementation, support, training, and consulting services played a vital role in optimizing system usage. Hardware demand also grew steadily, with hospitals and clinics investing in servers, storage, and networking devices. Meanwhile, software and integrated systems advanced significantly, driven by interoperability and EHR adoption. On the end-user side, hospitals accounted for 77.4% of the market, followed by diagnostic centers and academic institutes. Collectively, these segments underscored the essential role of information systems in improving efficiency, patient care, and medical research.

Key Players Analysis

Athenahealth Inc. has emerged as a frontrunner in the healthcare information systems (HIS) market. The company is known for its innovative and user-friendly solutions designed to enhance operational efficiency. Its strong presence is attributed to its advanced electronic health record (EHR) and practice management tools. These systems are widely adopted by healthcare providers seeking improved workflows and cost efficiency. Athenahealth’s emphasis on cloud-based platforms has positioned it as a preferred partner in digital transformation within the healthcare sector.

The Agfa Gevaert Group is recognized as a leading player with its strong focus on healthcare IT and medical imaging. Its integrated solutions combine imaging technologies with information management platforms, delivering comprehensive tools for healthcare professionals. The group’s offerings address both diagnostic and administrative needs, ensuring better coordination in hospitals and clinics worldwide. By focusing on innovation and interoperability, Agfa has strengthened its global market position. Its commitment to advancing digital healthcare systems has made it an essential contributor to industry modernization.

eClinicalWorks and Philips Healthcare are significant players driving the growth of HIS globally. eClinicalWorks specializes in EHR and practice management solutions, improving healthcare delivery efficiency and patient care outcomes. Its solutions are widely acknowledged for advancing digital health adoption. Philips Healthcare, on the other hand, contributes with a broad portfolio spanning diagnostic imaging, patient monitoring, and information management systems. Its advanced technologies support precision medicine and real-time data integration. Together, these companies strengthen the HIS ecosystem and contribute to healthcare’s ongoing digital transformation.

Challenges

1) Interoperability and Data Fragmentation

Health data are often stored in separate systems such as EHRs, labs, imaging platforms, and payer databases. This fragmentation makes it difficult to achieve smooth data exchange. Even though progress has been made, many healthcare providers still face challenges with incomplete interoperability. Care coordination is delayed, and advanced analytics become harder to implement. The OECD highlights the importance of global standards such as FHIR. These standards can support seamless data exchange, reduce inefficiencies, and improve decision-making. Without strong interoperability, healthcare organizations cannot fully benefit from digital transformation or provide timely, coordinated care.

2) Cybersecurity Risk and Breach Impact

Healthcare remains a top target for cyberattacks due to sensitive patient data. The sector has experienced some of the largest breaches on record. For example, the Change Healthcare cyberattack affected 192.7 million people in the U.S., making it the largest breach ever reported. The U.S. HHS breach portal continues to show frequent and large incidents. These breaches cause financial losses, operational disruption, and damage to trust. The volume of exposed records has been rising steadily in recent years. This trend underlines the urgent need for strong cybersecurity measures, better resilience strategies, and strict compliance frameworks.

3) Clinician Burnout and EHR Usability

Clinicians face high levels of stress from documentation and digital workloads. Research shows that heavy inbox volume, time-consuming documentation, and poor system usability contribute to burnout. Many EHR platforms add clerical burdens rather than reduce them. Workflow interruptions and inefficient design make daily tasks harder. Studies consistently identify usability problems as key drivers of frustration among physicians and nurses. Burnout not only affects clinicians but also patient care quality. Addressing this challenge requires redesigning EHR interfaces, reducing unnecessary tasks, and ensuring technology supports, rather than hinders, medical practice.

4) Data Quality, Governance, and Trust

Reliable data is essential for analytics and AI in healthcare. However, issues such as inconsistent coding, missing values, and unclear data origins undermine trust. Poor data governance makes it harder to ensure accuracy and patient safety. International health organizations emphasize the need for robust governance frameworks. Strong privacy and security standards must be in place to protect sensitive information. Building trust requires transparency, standardization, and accountability in how health data is collected and reused. Without this foundation, advanced technologies cannot deliver accurate insights or safe recommendations for clinical or operational use.

5) Uneven Digital Capacity Across Settings

Not all healthcare systems have equal access to digital tools. In many low- and middle-income countries, limited resources slow the adoption of digital health solutions. Workforce shortages, weak infrastructure, and financial constraints further widen the gap. Even within high-income regions, smaller hospitals and clinics often lack the capacity to implement advanced systems. The WHO Digital Health Strategy highlights the need to strengthen capacity across all settings. Investments in infrastructure, training, and equitable access are essential. Without addressing these disparities, digital health innovations will not reach their full potential globally.

Opportunities

1. Standards-Based Interoperability at Scale

Healthcare systems are shifting toward FHIR-first platforms and APIs. These standards reduce integration costs and make it easier to connect different systems. Vendors that adopt FHIR can enable modular innovation and support data exchange across providers, payers, and pharmacies. National governments are creating adoption plans, which signals strong growth opportunities. With FHIR, vendors can scale solutions faster, reduce custom integration work, and improve long-term system compatibility. Aligning with these standards creates trust and positions companies for future contracts. The push for nationwide interoperability makes this a critical area for investment and competitive advantage.

2. Secure-by-Design Architectures

Security is becoming a priority as healthcare faces increasing risks from cyber threats. Zero-trust security, multi-factor authentication, and least-privilege access are now seen as essential. These measures reduce the risk of breaches and align with strict regulatory expectations. Hospitals and health systems are investing in continuous monitoring and resilience planning. Vendors that provide secure-by-design systems gain credibility and trust. The growing focus on compliance, data protection, and patient safety creates opportunities for new solutions. With regulators pushing for modernization, security vendors are in a strong position to capture long-term demand across the healthcare ecosystem.

3. Workflow-Centric EHR Optimization

Healthcare providers are seeking improvements in electronic health records (EHR). Usability challenges create extra workload and contribute to clinician burnout. Solutions that reduce documentation time, improve inbox management, and automate routine tasks are in high demand. Evidence shows that EHR burden is linked to staff dissatisfaction, making optimization a business priority. Vendors can offer ambient documentation, templating tools, and human-centered design features. These solutions can reduce administrative strain, improve user satisfaction, and free up time for patient care. The ongoing focus on efficiency makes workflow optimization a valuable opportunity in healthcare IT.

4. Patient Engagement and Virtual Care Integration

Hospitals and clinics are expanding tools that connect patients to their care. Patient portals, secure messaging, and remote access platforms are now widely used. These solutions support better prevention, adherence, and overall patient experience. Virtual care tools also create new data streams for population health management. With rising expectations for digital access, engagement platforms are central to care strategies. Providers are seeking solutions that integrate seamlessly into existing systems. Vendors who deliver user-friendly and connected platforms gain strong adoption potential. The demand for patient-centric technology is expected to grow as healthcare shifts to hybrid and digital-first models.

5. Secondary Use of Data for Quality and Research

Healthcare data has growing value beyond direct care. With strong governance, de-identified and permissioned datasets can support outcomes measurement, real-world evidence, and AI development. Researchers and regulators emphasize the importance of data privacy while promoting access for innovation. OECD guidance highlights the balance between governance and value creation. Vendors can provide platforms that enable safe data sharing and analytics. By supporting secondary data use, health systems can improve quality of care and accelerate discovery. The opportunity lies in offering trusted solutions that protect privacy while unlocking data for research and decision-making.

6. Public Health Alignment and Digital Strategies

The World Health Organization (WHO) Digital Health Strategy is shaping healthcare modernization worldwide. It emphasizes equity, system alignment, and digital-first approaches. Governments are adopting frameworks that support digital transformation and public health priorities. Vendors who align offerings with these strategies gain stronger market access. By mapping solutions to policy goals, providers can secure funding and adoption pathways. Digital health solutions that improve coordination, population health, and data-driven planning are in demand. The alignment between policy and technology creates a clear opportunity for growth. Vendors positioned in this space can scale globally with government partnerships.

Conclusion

The healthcare information systems market is moving toward a strong and sustainable growth path, supported by digital transformation, regulatory initiatives, and demographic shifts. Governments and health organizations are actively promoting digital health, while providers are upgrading systems to improve care coordination, data sharing, and patient outcomes. Advances in cloud solutions, analytics, and interoperability are helping hospitals and clinics become more efficient and patient-focused. At the same time, challenges such as cybersecurity risks, uneven access, and clinician burnout remain important barriers. However, with policy alignment, technology innovation, and industry collaboration, the sector is expected to expand steadily and play a central role in shaping the future of healthcare.

View More Related Reports Here:

Blood Bank Information System Market || Anesthesia Information Management Systems Market || Cardiovascular Information System Market || Radiology Information Systems Market || Health Information Exchange (HIE) Market || Oncology Information Systems Market || Personal Health Record Software Market || Electronic Health Records Market || Health Data Archiving Market || Big Data in Healthcare Market || Clinical Data Analytics Solutions Market || Healthcare Data Monetization Market || Healthcare Customer Data Platform Market || Clinical Data Management System Market || Chromatography Data Systems Market || Patient Data Hub Solutions Market

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)