Table of Contents

Overview

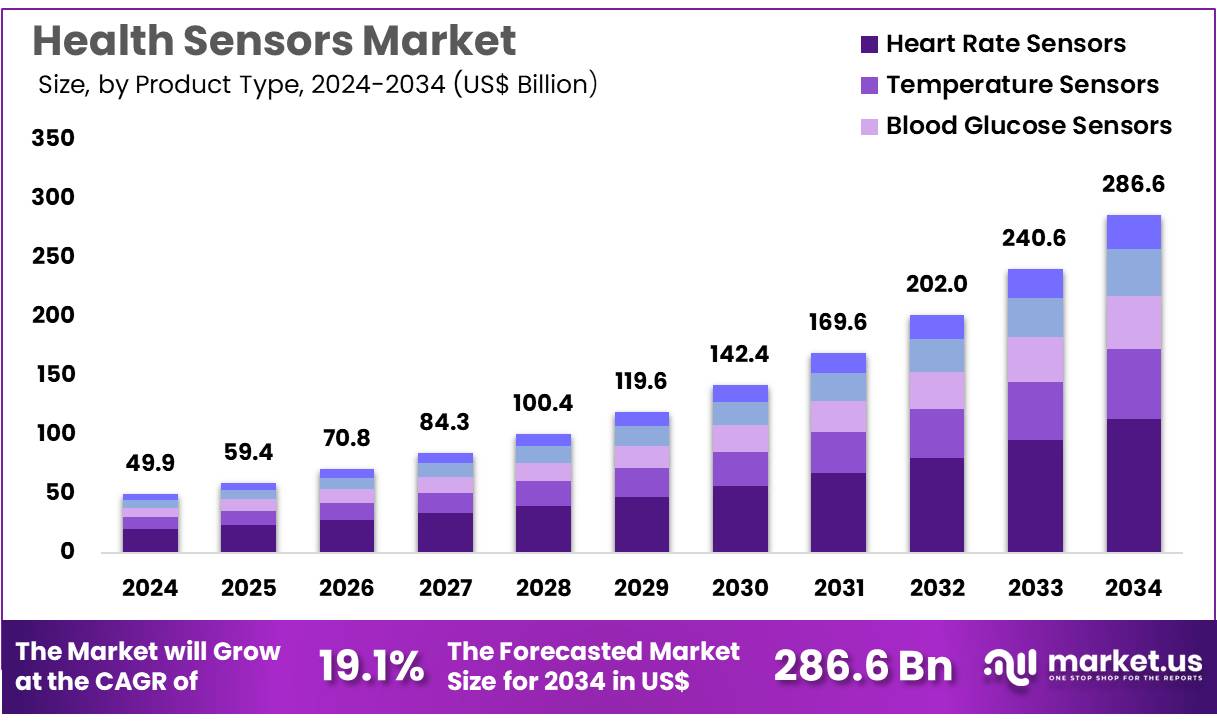

New York, NY – Dec 03, 2025 – Global Health Sensors Market size is expected to be worth around US$ 286.6 billion by 2034 from US$ 49.9 billion in 2024, growing at a CAGR of 19.1% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 37.4% share with a revenue of US$ 18.7 Billion.

The global market for health sensors has been expanding steadily as demand for real-time health monitoring and preventive care continues to increase. The adoption of innovative sensing technologies has been supported by rising chronic disease prevalence, the growth of wearable devices, and continuous advancements in digital health platforms. The integration of biosensors, motion sensors, temperature sensors, and pressure sensors into consumer and medical devices has improved diagnostic accuracy and enhanced patient engagement in personal health management.

Significant momentum has been observed in wearable health technologies, as manufacturers incorporate advanced sensor systems into smartwatches, fitness bands, and remote monitoring solutions. The growth of the market has also been influenced by the expansion of telehealth services, where continuous data collection from sensors is used to support remote diagnosis and treatment. The demand for non-invasive and minimally invasive monitoring has further supported the development of compact, energy-efficient sensor components.

The market outlook remains positive, as industry stakeholders invest in research and development to improve sensor precision, connectivity, and interoperability with digital ecosystems. The adoption of AI-enabled analytics is expected to increase the value of sensor-generated data, allowing early detection of health abnormalities and more personalized care pathways. As regulatory frameworks evolve to support digital health innovation, strong opportunities are anticipated across consumer health, clinical diagnostics, sports performance monitoring, and elderly care applications. The expansion of these technologies is expected to play a critical role in shaping the next generation of preventive healthcare solutions.

Key Takeaways

- In 2024, the health sensors market generated US$ 49.9 billion in revenue, supported by a 19.1% CAGR, and is projected to reach US$ 286.6 billion by 2033.

- The product type segment includes heart rate sensors, temperature sensors, blood glucose sensors, blood oxygen sensors, and others, with heart rate sensors accounting for 39.7% of the market in 2024.

- By technology, the market is categorized into handheld diagnostic sensors, wearable sensors, and implantable/ingestible sensors, where wearable sensors held a 57.3% share.

- In terms of application, the market is segmented into handheld diagnostic sensors, chronic illness & at-risk monitoring, wellness monitoring, patient admission triage, and others, with chronic illness & at-risk monitoring capturing 40.4% of total revenue.

- The end-user segment comprises hospitals & clinics, long-term care centers & nursing homes, home care settings, and others, with hospitals & clinics leading at 44.6%.

- North America emerged as the leading regional market, accounting for 37.4% of global revenue in 2024.

Regional Analysis

North America Leading the Health Sensors Market

North America accounted for the largest revenue share of 37.4%, supported by strong consumer adoption of personal health monitoring technologies and the growing burden of chronic diseases. According to the US Centers for Disease Control and Prevention (CDC), 6 in 10 adults in the country are living with at least one chronic illness, reinforcing the demand for continuous and reliable monitoring solutions.

The widespread use of wearable devices equipped with advanced sensors for heart rate, activity levels, and other health metrics has further strengthened the region’s market position. Industry assessments indicated that North America held the leading share of the global wearable medical devices market in 2024. In addition, ongoing FDA initiatives aimed at advancing digital health are accelerating the integration of sensor-based technologies into clinical and personal healthcare systems.

Asia Pacific Expected to Record the Highest CAGR

The Asia Pacific region is projected to achieve the fastest CAGR during the forecast period, driven by a rapidly expanding elderly population and the rising prevalence of chronic illnesses. In 2022, the region represented a substantial share of global cardiovascular disease cases, contributing to increased demand for continuous monitoring devices.

Government initiatives to strengthen digital health ecosystems are also supporting market expansion. India’s introduction of the Ayushman Bharat Digital Health Mission (ABDM) in 2022 is one such example, aimed at building a unified digital health infrastructure. Growing smartphone penetration and improved internet accessibility across the region are further expected to accelerate the adoption of sensor-based monitoring technologies.

Use Cases

- Chronic Disease Monitoring: Continuous monitoring of vital signs such as blood pressure and heart rate has become integral to long-term disease management. With six in ten Americans affected by at least one chronic condition, home-based sensors enable early detection of physiological deterioration and support timely clinical intervention.

- Diabetes Management: Continuous glucose monitoring technologies provide real-time blood sugar measurements for the 38.4 million Americans living with diabetes, representing 11.6% of the population. These systems improve glycemic control and have demonstrated up to a 30 percent reduction in hypoglycemic events in clinical evaluations.

- Cardiovascular Health Tracking: Wearable ECG patches and pulse oximeters are increasingly used to detect arrhythmias and monitor oxygen saturation. Heart disease caused 702,880 deaths in 2022, accounting for one in five U.S. fatalities, reinforcing the importance of continuous cardiac surveillance for early detection and improved outcomes.

- Remote Patient Monitoring in Medicare: Remote Patient Monitoring has been incorporated into Medicare care models, with about 43 % of beneficiaries utilizing RPM at least once. Sensor-driven RPM has been linked to fewer emergency department visits and reduced hospital readmissions, indicating improved care quality and cost efficiency.

- Public Health and Environmental Surveillance: Environmental and satellite-based sensors are used to assess air quality and vector habitats, supporting outbreak prediction for diseases such as malaria and dengue. Nearly all CDC-supported vector-borne disease research now integrates remote sensing to enhance mapping precision and strengthen response strategies.

Frequently Asked Questions on Health Sensors

- How do health sensors work?

Health sensors operate through advanced sensing technologies that detect biological signals and convert them into measurable data. These signals are processed through integrated circuits and transmitted to healthcare platforms or smart devices for real-time analysis, monitoring, and health decision support. - What types of health sensors are commonly used?

Common health sensors include heart rate sensors, blood pressure sensors, glucose monitors, motion sensors, temperature sensors, and pulse oximeters. These devices are increasingly integrated into wearables, remote monitoring systems, and clinical diagnostic tools for continuous health assessment. - What are the key applications of health sensors?

Health sensors are widely applied in chronic disease management, fitness tracking, diagnostic monitoring, elderly care, and remote patient care. Their role has expanded significantly due to rising digital health adoption and increased demand for real-time physiological data. - What benefits do health sensors provide?

Health sensors enable early detection of health issues, reduce hospital visits, support personalized treatment, and improve patient outcomes. Continuous data collection helps clinicians track disease progression, while users gain improved self-management through timely monitoring insights. - Which regions are leading the health sensors market?

North America leads due to strong digital health infrastructure, followed by Europe with supportive regulatory frameworks. The Asia-Pacific region is experiencing rapid expansion driven by rising healthcare spending, urbanization, and growing consumer preference for smart health monitoring devices. - Who are the key end-users in the health sensors market?

Primary end-users include hospitals, diagnostic centers, home healthcare providers, wearable device manufacturers, and fitness technology companies. Increased adoption in telemedicine networks and remote patient monitoring solutions is further expanding the end-user base.

Conclusion

The global health sensors market is positioned for robust long-term growth, supported by rising chronic disease prevalence, expanding wearable adoption, and increasing integration of digital health technologies. Advances in sensor precision, interoperability, and AI-driven analytics are expected to strengthen preventive care and enable more personalized health management.

Strong uptake in North America and rapid acceleration in Asia Pacific highlight broad regional opportunities. The market’s expansion is anticipated to be sustained by continuous innovation, supportive regulatory frameworks, and growing demand for real-time, non-invasive monitoring across clinical, home-based, and consumer health environments.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)