Table of Contents

Overview

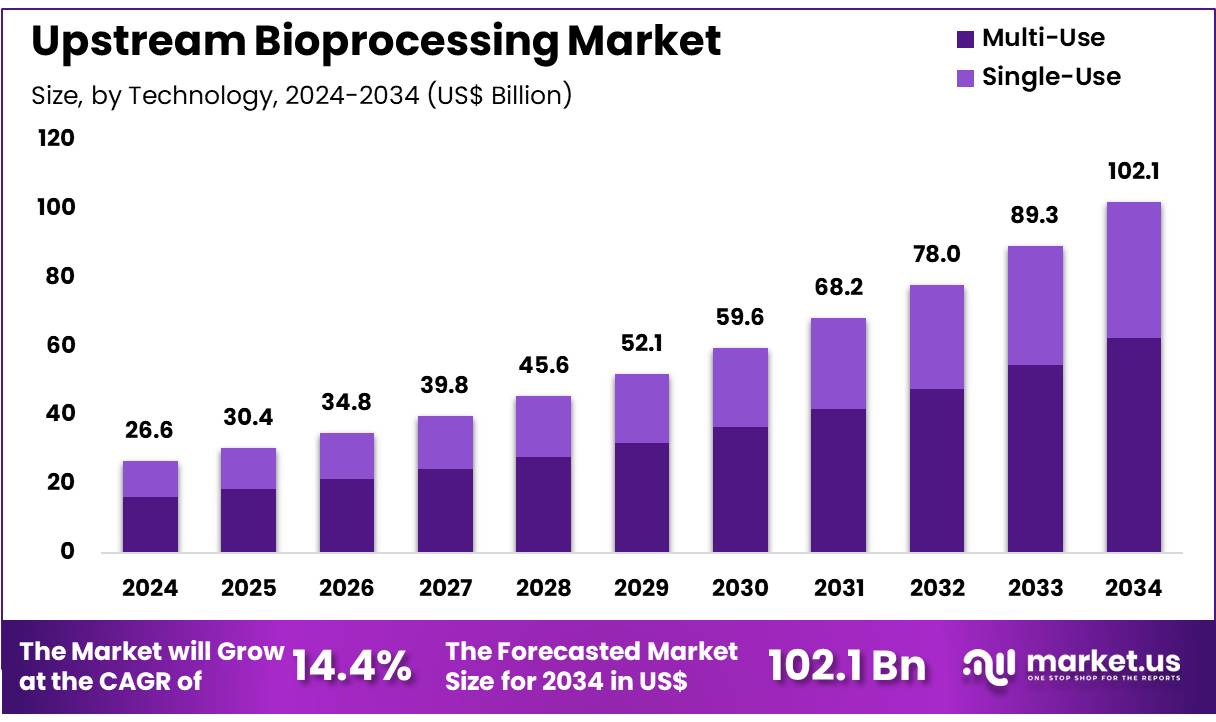

New York, NY – Nov 25, 2025 – The Global Upstream Bioprocessing Market size is expected to be worth around US$ 102.1 billion by 2034 from US$ 26.6 billion in 2024, growing at a CAGR of 14.4% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 38.2% share with a revenue of US$ 10.4 Billion.

Upstream bioprocessing has been recognized as a critical phase in the production of biologics, as it establishes the foundational conditions under which cells are cultured, grown, and optimized for therapeutic output. The process involves cell line development, media preparation, inoculum expansion, and large-scale cultivation, and it plays a decisive role in determining overall product quality and yield. The growth of the biopharmaceutical industry has been supported by rapid advancements in upstream technologies, including single-use bioreactors, high-performance cell culture media, and automation systems designed to enhance process efficiency.

The demand for monoclonal antibodies, vaccines, recombinant proteins, and cell-based therapies has increased significantly, and upstream bioprocessing platforms have been adapted to meet this rising need. The adoption of perfusion systems and high-density cell culture methods has enabled continuous production with improved productivity. These innovations have reduced manufacturing timelines and strengthened the commercial viability of complex biologics.

Regulatory focus has remained centered on process robustness, reproducibility, and compliance with quality standards, contributing to continuous improvement across production facilities. Partnerships between technology providers, biopharmaceutical manufacturers, and research organizations have accelerated innovation, enabling upstream operations to become more flexible and scalable.

The expansion of global biologics manufacturing capacity, combined with the growing emphasis on precision medicine, is expected to support sustained investment in upstream bioprocessing solutions. The industry has shown cautious optimism as new technologies continue to address long-standing challenges related to cost, efficiency, and process control. This sector is positioned to play an essential role in shaping the next generation of biotherapeutics.

Key Takeaways

- In 2024, the market for upstream bioprocessing generated a revenue of US$ 26.6 Billion, with a CAGR of 14.4%, and is expected to reach US$ 102.1 Billion by the year 2033.

- The product type segment is divided into bioreactors/fermenters, cell culture products, filters, and others, with bioreactors/fermenters taking the lead in 2024 with a market share of 53.5%.

- Considering technology, the market is divided into multi-use and single-use. Among these, multi-use held a significant share of 61.2%.

- Furthermore, concerning the application segment, the market is segregated into media preparation, cell culture, and cell separation. The cell culture sector stands out as the dominant player, holding the largest revenue share of 52.8% in the upstream bioprocessing market.

- The mode segment is segregated into in-house and outsourced, with the in-house segment leading the market, holding a revenue share of 58.2%.

- North America led the market by securing a market share of 38.2% in 2024.

Market Segmentation Analysis

- Product Type Analysis: The bioreactors and fermenters segment held a dominant 53.5% share of the upstream bioprocessing market in 2023. Its growth was supported by the rising production of vaccines, monoclonal antibodies, and therapeutic proteins. Bioreactors continue to serve as the core equipment for large-scale cell cultivation. Ongoing improvements in automation, vessel design, and real-time monitoring have strengthened process reliability and efficiency, promoting broader adoption across global biomanufacturing facilities.

- Technology Analysis: Multi-use systems represented 61.2% of the market in 2023, driven by their long-term cost advantages and operational adaptability. These systems enable high-volume production while reducing recurring operational expenses, particularly in settings with lower contamination control requirements. With increasing clinical trial activity and expanding biologics manufacturing, multi-use technologies remain the preferred option in established facilities. Their strong integration within existing infrastructure is expected to support sustained leadership over the forecast period.

- Application Analysis: The cell culture segment accounted for 52.8% of total revenue in 2023, emerging as the leading application area. Its prominence was supported by growing demand for biologics such as vaccines and advanced cell-based therapies. Cell culture platforms are essential for producing therapeutic proteins by facilitating the expansion of recombinant cell lines. Rising disease incidence, especially cancer and genetic disorders, combined with advancements in media optimization and high-performance cell lines, is anticipated to drive continued segment growth.

- Mode Analysis: The in-house segment captured 58.2% of upstream bioprocessing revenue in 2023, reflecting the industry’s focus on enhanced control over quality, consistency, and proprietary workflows. In-house operations offer scalable and customizable production capabilities that are increasingly vital for personalized and niche biologics. The ability to manage scheduling internally and respond quickly to market shifts has reinforced the preference for in-house manufacturing, solidifying its position as a key component of the global bioprocessing ecosystem.

Regional Analysis

North America accounted for the highest revenue share of 39.2%, supported by documented advancements across the bioprocessing landscape. The FDA’s annual report confirmed the approval of 12 new biologic therapies in 2023, reflecting continued demand for upstream bioprocessing technologies. Government funding for biomanufacturing infrastructure reached US$ 2 billion in 2023, as outlined in the Department of Health and Human Services budget. Production capacity expansion was also verified through corporate disclosures, with major biotechnology companies reporting 15–20% increases in manufacturing capabilities in their 2023 filings.

Further support for market expansion was observed in academic initiatives. Institutions such as MIT and Stanford announced the establishment of new research centers dedicated to bioprocessing optimization. The National Institute for Innovation in Manufacturing Biopharmaceuticals reported rising adoption of single-use systems in its annual technology survey. Collectively, these developments strengthened growth across key therapeutic segments, including monoclonal antibodies and cell therapies.

The Asia Pacific region has been projected to record the fastest CAGR during the forecast period. China’s National Development and Reform Commission reported US$ 1.5 billion in biomanufacturing investments in 2023, while India’s Department of Biotechnology confirmed expansions in biopharmaceutical production capacity.

South Korea’s Ministry of Food and Drug Safety documented an increase in biologic approvals, and Singapore’s trade statistics indicated higher imports of bioprocessing equipment. Corporate announcements across the region further validated substantial capacity enhancement initiatives completed in 2023. These verified developments indicate strong long-term growth potential for the region’s bioprocessing capabilities, particularly in biologics and advanced cell therapies.

Frequently Asked Questions on Upstream Bioprocessing

- What technologies are used in upstream bioprocessing?

Upstream bioprocessing utilizes advanced technologies such as single-use bioreactors, automated control systems, perfusion culture, and high-throughput screening tools. These technologies support efficient cell growth, enhanced productivity, and reduced contamination risk across biopharmaceutical manufacturing workflows. - Why is upstream bioprocessing important?

Upstream bioprocessing is critical because product quality and yield are largely determined during cell cultivation. Optimized upstream operations ensure consistent biological activity, reduced batch failure rates, and improved overall manufacturing efficiency for complex biologics, including monoclonal antibodies and vaccines. - What are single-use systems in upstream bioprocessing?

Single-use systems are disposable bioprocessing components such as bags, tubing, and bioreactor vessels designed to replace traditional stainless-steel systems. Their adoption reduces cleaning requirements, lowers contamination risk, and enables faster changeover in manufacturing facilities. - How does automation support upstream bioprocessing?

Automation enhances upstream bioprocessing by enabling real-time monitoring, precise control of culture conditions, and reduced manual intervention. These capabilities improve reproducibility, accelerate process development, and support the production of high-quality biologics at scale. - What types of products are produced through upstream bioprocessing?

Upstream bioprocessing is used to generate biologics such as monoclonal antibodies, recombinant proteins, cell-based therapies, and viral vectors. These products are manufactured by cultivating engineered cells to express therapeutic or prophylactic biomolecules for clinical use. - Which regions dominate the upstream bioprocessing market?

North America and Europe currently dominate the market due to established biopharmaceutical production infrastructure, strong R&D investments, and favorable regulatory environments. Asia-Pacific is experiencing accelerated growth supported by capacity expansions and increasing regional biologics manufacturing activities. - Who are the major players in the upstream bioprocessing market?

Major market participants include Thermo Fisher Scientific, Sartorius, Merck KGaA, Cytiva, and Danaher. These companies provide advanced bioreactors, media solutions, automation platforms, and single-use technologies supporting development and scale-up of upstream bioprocessing operations. - What trends are shaping the upstream bioprocessing market?

Key trends include the shift toward continuous bioprocessing, integration of automation and AI-driven analytics, increased reliance on single-use technologies, and rising investments in cell and gene therapy manufacturing. These trends support improved productivity and operational resilience.

Conclusion

The upstream bioprocessing sector has advanced into a strategic pillar of biologics production, supported by rising demand for monoclonal antibodies, vaccines, and cell-based therapies. Continuous innovation in bioreactors, media systems, single-use technologies, and automation has strengthened process efficiency, scalability, and product quality.

Market expansion has been reinforced by strong regional investments, regulatory support, and increased manufacturing capacity across North America, Europe, and Asia Pacific. With growing emphasis on precision medicine and high-yield cell culture platforms, upstream bioprocessing is positioned for sustained growth. The industry is expected to remain a critical enabler of next-generation biotherapeutics over the coming decade.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)