Table of Contents

Overview

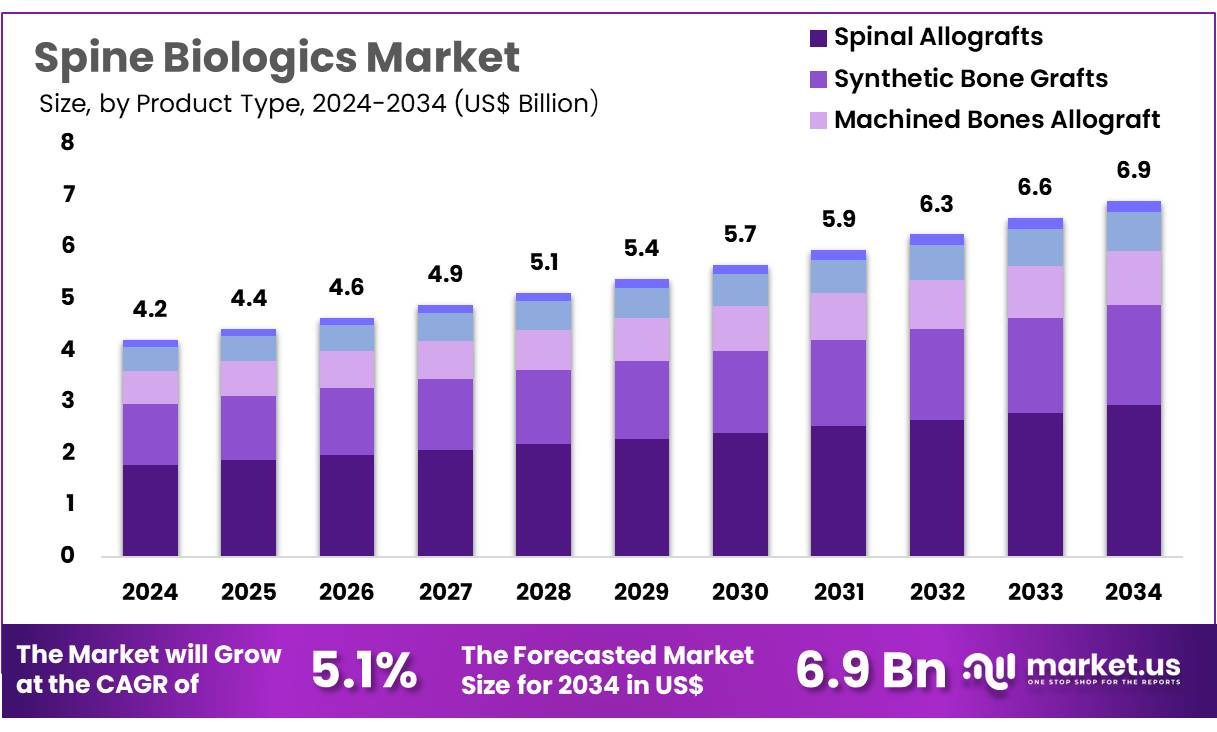

New York, NY – Oct 31, 2025 – Global Spine Biologics Market size is expected to be worth around US$ 6.9 Billion by 2034 from US$ 4.2 Billion in 2024, growing at a CAGR of 5.1% during the forecast period 2025 to 2034. North America held a dominant market position, capturing more than a 39.8% share and holds US$ 1.7 Billion market value for the year.

The global spine biologics market is experiencing notable growth, driven by increasing prevalence of spinal disorders, a rising aging population, and continuous advancements in regenerative medicine. The demand for minimally invasive spinal procedures has been rising, supported by strong clinical outcomes and reduced recovery times. Favorable reimbursement frameworks and supportive government initiatives for orthopedic research have further contributed to market expansion.

Biologic products including bone graft substitutes, cell-based matrices, and growth factors are being increasingly adopted in spinal fusion and spinal decompression procedures. The focus of manufacturers has been placed on developing next-generation biologics with improved osteoinductive and osteoconductive properties. Investment in stem-cell-based therapies and recombinant technologies has been accelerating, illustrating strong innovation momentum across the ecosystem.

North America currently represents the leading regional market, attributed to advanced healthcare infrastructure, high patient awareness, and strong surgeon uptake of biologic solutions. Asia-Pacific is anticipated to exhibit the fastest growth rate, supported by healthcare modernization and increasing access to advanced orthopedic therapies. Strategic collaborations, product launches, and regulatory clearances are being observed among leading market players to strengthen product portfolios and expand global reach.

The growth of the spine biologics market can be attributed to clinical efficacy, increasing procedural volume, and expanding applications in spinal repair and regeneration. Continued research excellence and technological development are expected to support sustainable industry progress and enhance patient outcomes across diverse care settings. Growth prospects remain strong across global markets worldwide.

Key Takeaways

- The Spine Biologics market is projected to reach approximately USD 6.9 billion by 2034, rising from USD 4.2 billion in 2024.

- The product landscape comprises synthetic bone grafts, spinal allografts, machined bone allografts, demineralized bone matrix, and other biologic solutions. Spinal allografts were identified as the dominant category in 2024, accounting for 42.5% of total revenue.

- Based on surgery type, the industry is segmented into transforaminal lumbar interbody fusion, posterior lumbar interbody fusion, lateral lumbar interbody fusion, anterior lumbar interbody fusion, and anterior cervical discectomy and fusion. Anterior cervical discectomy and fusion emerged as the leading segment, representing 33.7% of the market.

- With respect to end use, hospitals and ambulatory surgical centers constitute the primary settings. Hospitals held the dominant share, representing 61.2% of total revenue in 2024.

- Geographically, North America led the global market, contributing 39.8% of total revenue in 2024.

Regional Analysis

North America accounted for the largest revenue share of 39.8%, supported by the rising prevalence of spinal disorders, advancements in biologic treatment options, and increasing adoption of minimally invasive surgical procedures. Growth in the elderly population and the rising incidence of lifestyle-related conditions, including obesity and osteoporosis, have resulted in a higher volume of spinal interventions, thereby driving demand for advanced spine biologics.

In January 2024, the U.S. Food and Drug Administration (FDA) granted Breakthrough Device Designation to Renovos Biologics for RENOVITE Bone Morphogenic Protein 2. This development emphasizes the region’s commitment to innovation in biologic therapies that support bone regeneration and enhance healing post-spinal surgeries.

Continuous progress in biologic research, including stem cell-based therapies and bone morphogenic proteins, has strengthened market expansion by offering more effective and less invasive treatment pathways. Furthermore, increased healthcare spending and strategic partnerships between biotechnology firms and medical device manufacturers have improved access to advanced biologic solutions, supporting steady market growth across North America.

Asia Pacific is projected to record the fastest CAGR over the forecast period, driven by rising healthcare expenditure, expanding population, and increasing incidence of spinal disorders. Demand for advanced biologic treatments for conditions such as degenerative disc disease and spinal stenosis is anticipated to rise as healthcare infrastructure strengthens across China, India, and Japan.

The region’s rapidly aging population and accelerating urbanization are expected to increase spinal disorder prevalence, bolstering the need for biologic-based spinal therapies and surgical solutions. Advancements in biotechnology and regenerative medicine in countries such as South Korea and Australia are also expected to support product innovation.

Higher awareness of biologic treatment advantages, including faster recovery and reduced complication risks, alongside growing domestic manufacturing capabilities and supportive government healthcare initiatives, is expected to further accelerate market growth in the Asia Pacific region.

Emerging Trends

- Expansion of Clinical Research Activity: A systematic review of ClinicalTrials.gov reported 26 prospective clinical trials investigating cell-based therapies for intervertebral disc regeneration as of November 12, 2023. This reflects a steady rise in clinical efforts directed toward biologic treatment pathways for spine-related disorders.

- Increasing Adoption of Mesenchymal Stromal Cell Approaches: Mesenchymal stromal cell (MSC) injections into the disc space have emerged as the most frequently evaluated biologic strategy, indicating a sustained shift toward stimulating natural tissue repair rather than relying solely on implant-based interventions.

- Initial Progress in Growth Factor and Small-Molecule Modalities: Research into growth factor-driven therapies (including BMP variants) and small-molecule biologics remains concentrated in early-phase studies. The limited number of ongoing trials suggests that therapeutic categories beyond cell-based approaches are in nascent stages of development.

- Advancement of Multifunctional Biologic Constructs: Increasing emphasis is being placed on integrated biologic platforms combining osteogenic, osteoinductive, and osteoconductive properties. Gene therapy vectors and hydrogel-based scaffolds are being explored to improve spinal fusion performance and facilitate disc tissue restoration.

- Emphasis on Minimally Invasive Delivery Systems: Injectable formulations, including MSC suspensions blended with carriers such as hyaluronic acid, are being prioritized to support reduced surgical trauma and facilitate outpatient treatment. This aligns with the broader transformation of spine care toward minimally invasive therapeutic delivery.

Frequently Asked Questions on Spine Biologics

- Why are spine biologics used in spinal surgery?

Spine biologics are used to facilitate bone fusion, accelerate healing, reduce post-operative complications, and improve structural stability. Their application can reduce the need for harvesting patient bone and enhance success rates in degenerative or traumatic spinal conditions. - What types of spine biologics are commonly used?

Common types include autografts, allografts, demineralized bone matrices, synthetic bone substitutes, growth factors, and stem-cell-based materials. Each type provides specific biological support for bone formation, tissue regeneration, and integration with the patient’s native anatomy. - What role do growth factors play in spine biologics?

Growth factors stimulate cell activity, enhance bone-forming processes, and improve tissue repair. They are often used to accelerate fusion and regeneration, providing targeted biological signals that improve healing quality and reduce recovery time in spinal fusion procedures. - What is the difference between autograft and allograft in spine biologics?

Autografts originate from the patient’s own body and provide natural compatibility and strong healing potential, while allografts are donor materials, reducing surgical time and patient morbidity, and providing effective structural support without additional tissue harvesting. - What is meant by the spine biologics market?

The spine biologics market refers to the commercial segment involved in developing, manufacturing, and supplying biological materials used for spinal fusion, tissue repair, and bone regeneration. It includes medical device companies, biotech firms, and hospital procurement systems. - What factors contribute to market growth?

Market expansion can be attributed to rising spinal disorder cases, increasing use of minimally invasive techniques, advancements in regenerative technologies, and greater adoption of biologics for improved healing and reduced recovery time compared to conventional grafting methods. - Which product categories drive market adoption?

Key product categories include bone graft substitutes, allografts, cell-based matrices, and growth-factor-based materials. Adoption is driven by clinical effectiveness, surgeon preference, and advancements in biomaterials that improve fusion success and reduce surgical complication risks. - What future trends are expected in the spine biologics market?

Future developments are expected to include personalized regenerative therapies, wider integration of stem-cell-based systems, biologic-enhanced minimally invasive surgery, and technological innovation in biomaterials and delivery systems that further improve spinal fusion reliability and healing outcomes.

Conclusion

The global spine biologics market is positioned for sustained growth, supported by rising spinal disorder incidence, an aging population, and expanding adoption of minimally invasive and regenerative therapies. Advancements in biologic materials, including cell-based matrices, synthetic grafts, and growth factors, are expected to enhance fusion outcomes and accelerate recovery.

Strong clinical evidence, supportive reimbursement policies, and active regulatory pathways are reinforcing market development. North America remains the dominant region, while Asia-Pacific is anticipated to record the fastest expansion. Ongoing research in stem-cell technologies, multifunctional biologics, and innovative delivery platforms is expected to strengthen long-term market potential and patient benefits.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)