Table of Contents

Overview

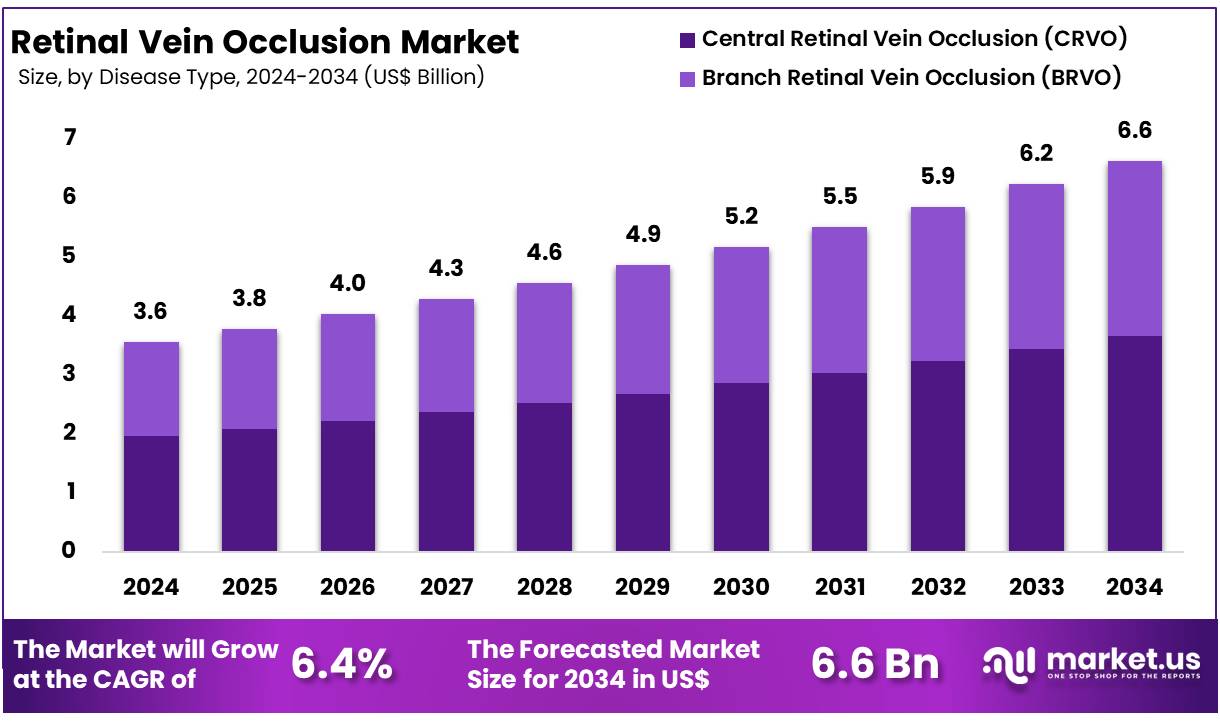

New York, NY – Nov 03, 2025 – Global Retinal Vein Occlusion Market size is expected to be worth around US$ 6.6 Billion by 2034 from US$ 3.6 Billion in 2024, growing at a CAGR of 6.5% during the forecast period from 2025 to 2034. In 2023, North America led the market, achieving over 41.10% share with a revenue of US$ 1.46 Million.

A rise in awareness and diagnostic precision is shaping the understanding of Retinal Vein Occlusion (RVO), a vision-threatening vascular disorder of the retina. RVO occurs when a vein responsible for draining blood from the retina becomes blocked, leading to impaired blood flow, hemorrhage, and swelling within retinal tissues.

The condition is recognized as the second most common retinal vascular disease after diabetic retinopathy, and its occurrence increases significantly with advancing age. The prevalence of hypertension, diabetes, and cardiovascular disorders has been identified as key contributing factors to disease progression.

Early symptoms such as sudden blurred vision or partial vision loss can be observed, particularly when the central retinal vein is affected. Timely ophthalmic evaluation plays a critical role, as delays in diagnosis may lead to irreversible damage to retinal structures.

Current therapeutic approaches include intravitreal injections targeting vascular endothelial growth factor (VEGF), corticosteroid implants, and laser photocoagulation. These interventions have demonstrated effectiveness in managing macular edema and limiting vision deterioration.

Research activity in this field continues to advance, driven by the growing demand for improved treatment outcomes and long-term disease management. Increasing screening programs, along with technological developments in retinal imaging, have facilitated earlier intervention and enhanced patient prognosis.

The burden associated with RVO underscores the need for continued education, preventive strategies for high-risk populations, and sustained innovation in ophthalmic care. The importance of collaborative efforts among clinicians, researchers, and healthcare stakeholders has been emphasized to support improved vision health and patient quality of life.

Key Takeaways

- The global Retinal Vein Occlusion market was valued at US$ 3.56 Billion in 2024 and is projected to reach US$ 6.26 Billion, exhibiting a CAGR of 6.5%.

- By disease type, Central Retinal Vein Occlusion (CRVO) accounted for the largest share, representing 55.2% of total revenue.

- Based on condition, the Non-Ischemic segment held the dominant position with a 61.4% market share.

- In terms of diagnosis, Optical Coherence Tomography emerged as the leading segment, contributing 38.7% of market revenue.

- By treatment, Anti-vascular Endothelial Growth Factor (Anti-VEGF) therapies constituted the highest share at 44.8%.

- Based on end-user, Hospitals & Clinics led the market, securing a 52.9% share.

- Regionally, North America remained the largest market, capturing 41.10% of global revenue.

Regional Analysis

In 2024, North America accounted for 41.10% of total market revenue, supported by a well-established and strongly regulated healthcare system. Growth in the region has been driven by strategic collaborations among leading industry participants aimed at expanding product portfolios and maintaining stringent quality benchmarks, thereby increasing adoption of Retinal Vein Occlusion (RVO) therapies. A rising burden of ocular disorders also continues to reinforce market expansion in the region.

Data from the CDC indicates that nearly 12 million individuals aged 40 years and above in the United States are affected by vision impairment. Supportive reimbursement structures further strengthen market growth, as approximately 84% of the U.S. population receives healthcare coverage through either public insurance programs (26%) or private insurers (70%).

The combination of comprehensive reimbursement coverage and ongoing advancements in treatment approaches is anticipated to sustain favorable growth prospects for the RVO market across North America.

Emerging Trends

- Rising prevalence associated with metabolic comorbidities: Incidence of retinal vein occlusion increased during 2021–2022, particularly among individuals aged 40–64. The rise has been attributed to a higher prevalence of hypertension, diabetes, and other metabolic disorders rather than direct effects of COVID-19.

- Shift toward chronic disease management: Long-term data indicate that retinal vein occlusion requires extended treatment and monitoring for at least five years to sustain visual outcomes. The condition is increasingly viewed as a chronic vascular disorder requiring customized, continuity-based therapeutic strategies.

- Enhanced risk assessment for bilateral involvement: Evidence shows a 6.3–6.4% probability of disease occurrence in the fellow eye. This trend supports earlier screening and proactive monitoring for high-risk groups, including older adults and individuals with vascular or hypertensive risk factors.

Use Cases

- Expanded therapeutic innovation: Dual-pathway biologics and biosimilars have strengthened clinical options for macular edema associated with retinal vein occlusion. Faricimab received FDA approval in 2022, with supplemental approval in 2023, offering dual inhibition of VEGF-A and Ang-2, while ranibizumab-eqrn emerged as the first interchangeable biosimilar to ranibizumab, improving cost-efficient access to care.

- Anti-VEGF therapy for macular edema: Regular intravitreal injections of agents such as bevacizumab and aflibercept significantly improve visual outcomes in macular edema secondary to retinal vein occlusion. Long-term results from the SCORE2 trial demonstrated sustained visual acuity gains five years after treatment commencement.

- Dual-pathway biologic intervention: Faricimab provides targeted inhibition of VEGF-A and Ang-2, reducing vascular leakage and edema. Its clinical introduction offers potential for extended dosing intervals and improved management of refractory macular edema associated with retinal vein occlusion.

- Adoption of interchangeable biosimilars: Ranibizumab-eqrn enables automatic substitution for reference ranibizumab at the pharmacy level, expanding access and supporting cost containment in the management of retinal vein occlusion-related macular edema.

- Individualized long-term therapy strategies: Real-world evidence confirms that most patients require continued treatment beyond the initial year. Personalized injection schedules informed by optical coherence tomography guide sustained control of retinal thickness and preservation of visual function over extended follow-up periods.

Frequently Asked Questions on Retinal Vein Occlusion

- What are the symptoms of Retinal Vein Occlusion?

Symptoms generally include sudden blurring or loss of vision in one eye. Distortion of central vision, dark spots, and floaters may also be observed. Symptoms typically develop suddenly, signaling the need for immediate ophthalmic evaluation. - What causes Retinal Vein Occlusion?

The condition is primarily caused by blood vessel blockage due to clotting, high blood pressure, diabetes, or glaucoma. Age-related vascular changes and systemic cardiovascular issues often contribute to increased susceptibility among older individuals. - How is Retinal Vein Occlusion diagnosed?

Diagnosis is performed through a comprehensive eye examination, including dilated fundus evaluation, fluorescein angiography, and optical coherence tomography. These diagnostic tools help identify retinal swelling, hemorrhages, and vascular abnormalities associated with RVO. - How is Retinal Vein Occlusion treated?

Treatment mainly includes intravitreal anti-VEGF injections, corticosteroids, and laser therapy to reduce swelling and restore retinal function. Management typically focuses on minimizing complications and improving visual outcomes through ongoing ophthalmologic monitoring. - What factors drive the Retinal Vein Occlusion market growth?

Growth is attributed to increasing aging population, prevalence of diabetes and hypertension, improved ophthalmic imaging, and the adoption of anti-VEGF therapies. Favorable regulatory approvals and enhanced patient awareness also support continued market expansion. - Which treatment segment holds major share in the RVO market?

Anti-VEGF therapy dominates the market, supported by strong clinical outcomes and broad physician preference. Corticosteroid implants and laser procedures continue to serve as supplementary options, particularly for patients with persistent macular edema. - What regions lead the Retinal Vein Occlusion market?

North America holds a significant share due to advanced healthcare infrastructure, high treatment adoption, and active clinical research. Europe follows closely, while Asia-Pacific demonstrates accelerated growth driven by rising healthcare investment and disease burden.

Conclusion

The increasing burden of retinal vein occlusion has been reinforced by rising metabolic risk factors, growing elderly populations, and expanding diagnostic awareness. Advanced imaging and innovative therapies, including anti-VEGF agents and emerging biologics, have strengthened long-term management outcomes and elevated treatment standards.

Market expansion is being driven by sustained research investment, accessible biosimilars, and supportive reimbursement models, particularly in developed regions. The shift toward chronic care management, personalized treatment schedules, and proactive screening strategies underscores the evolution of clinical practice.

Continued technology adoption, clinical collaboration, and preventive eye-care initiatives are expected to support sustained market growth and improved patient quality of life.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)