Table of Contents

Overview

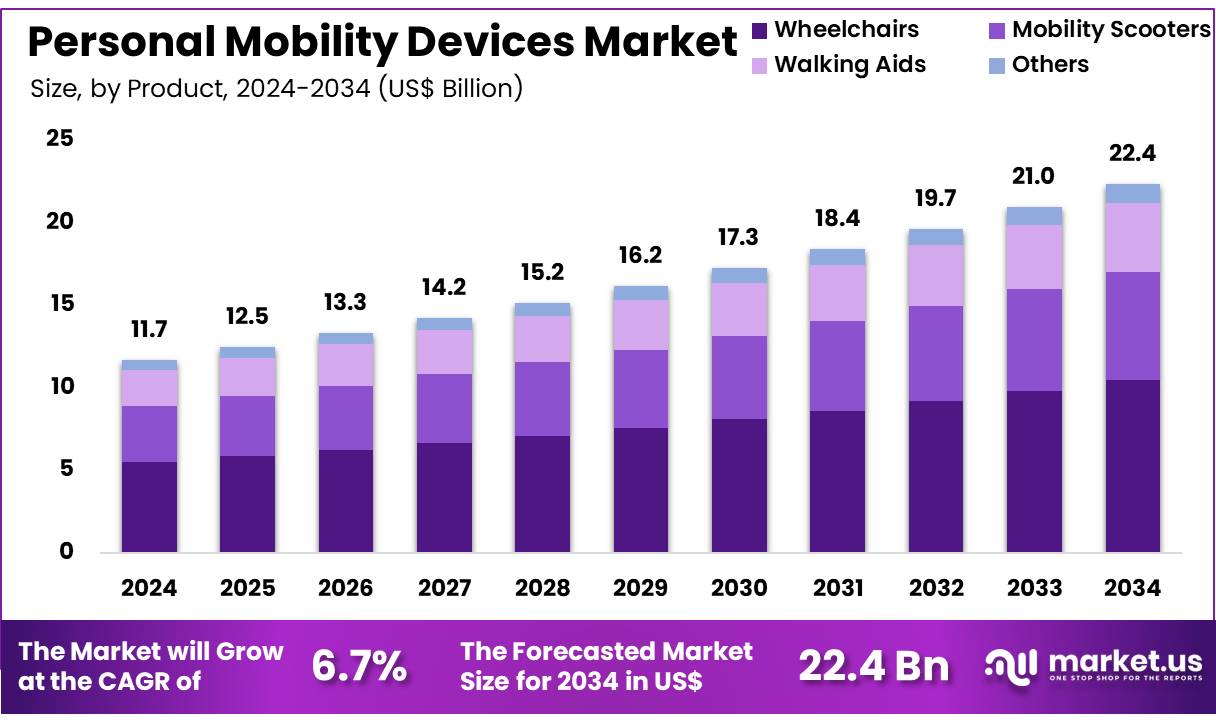

New York, NY – Nov 14, 2025 – Global Personal Mobility Devices Market size is expected to be worth around US$ 22.4 billion by 2034 from US$ 11.7 billion in 2024, growing at a CAGR of 6.7% during the forecast period 2025 to 2034. In 2023, North America led the market, achieving over 35.7% share with a revenue of US$ 1.6 Billion.

The market for Personal Mobility Devices (PMDs) has been witnessing consistent expansion as urban populations seek convenient, sustainable, and technology-enabled mobility solutions. The adoption of electric scooters, powered wheelchairs, mobility scooters, and smart assistive devices has been rising steadily, supported by advances in battery technologies, lightweight materials, and intelligent navigation systems. The growth of the market can be attributed to increasing urban congestion, rising demand for last-mile transportation, and the need for enhanced mobility support for aging populations.

Significant improvements in safety features, such as automatic braking, stability control, and real-time monitoring, have contributed to stronger consumer confidence. Growing investments by manufacturers in compact designs and energy-efficient components have further strengthened market competitiveness. The integration of IoT-based tracking and connected mobility platforms has enabled better performance management and higher user convenience.

Supportive regulatory frameworks and government initiatives promoting eco-friendly mobility solutions have been fostering market adoption across major cities. The expansion of dedicated riding lanes and charging infrastructure has been enabling smoother penetration of PMDs in both developed and emerging markets.

Overall, the Personal Mobility Devices market is positioned for continued growth as consumer preferences shift toward accessible, sustainable, and technology-driven mobility alternatives. The industry is expected to benefit from ongoing product innovation, rising health awareness, and increasing focus on urban mobility transformation.

Key Takeaways

- In 2023, the Personal Mobility Devices market generated revenue amounting to US$ 11.7 billion. The market has been expanding at a CAGR of 6.7%, and the overall value is projected to reach US$ 22.4 billion by 2033.

- The product landscape is categorized into wheelchairs, mobility scooters, walking aids, and other devices. Among these segments, wheelchairs accounted for the highest contribution, capturing 46.8% of the total market share in 2023.

- From an end-user perspective, the market is segmented into personal users and institutional users. Personal users represented the dominant segment, with a 58.4% share during the year.

- Regionally, North America emerged as the leading market, securing 35.7% of global revenue in 2023, supported by strong adoption of advanced mobility technologies and well-established healthcare infrastructure.

Regional Analysis

North America remained the leading region in the personal mobility devices market, accounting for 35.7% of the total share in 2024. The regional market value reached USD 4.2 billion, supported by the growing elderly population, a high incidence of chronic disorders, and a mature healthcare ecosystem that facilitates the adoption of advanced mobility solutions. The emphasis on improving quality of life for elderly and physically challenged individuals continues to stimulate regional demand.

Europe followed as a major contributor, driven by strong government initiatives promoting disability support solutions and the presence of a sizeable aging population requiring mobility assistance. Advancements in product innovation and a favorable regulatory framework have further strengthened device adoption across European markets.

The Asia Pacific region is projected to experience the most rapid expansion. Growth in this region is attributed to the increasing elderly population in countries such as Japan and China, improving healthcare infrastructure, and rising healthcare expenditure. The substantial population base provides significant opportunities for manufacturers operating in the mobility devices landscape.

The Middle East & Africa region exhibited steady progress, influenced by growing healthcare investments and policy efforts aimed at strengthening healthcare infrastructure. Increasing awareness regarding mobility aids is expected to support future market development.

Latin America also demonstrated positive growth momentum. Factors such as expanding urban populations, rising medical tourism, and supportive healthcare policies have been contributing to regional demand. Improvements in healthcare services and the expansion of the middle-income demographic are expected to reinforce market growth.

Emerging Trends

- Demographic Drivers: Demand for personal mobility devices is increasing as the global population ages. In the United States, individuals aged 65 years and older represented 16.8% of the population in 2020, rising from 13.0% in 2010, and expanding faster than any other age segment. Within this group, 29.4% used mobility aids outdoors and 26.2% used such devices indoors in 2021. This demographic shift is associated with higher life expectancy and the continued aging of the baby-boomer generation.

- Global Unmet Need and Policy Response: More than 2.5 billion people worldwide require at least one assistive product such as wheelchairs or mobility scooters, yet nearly one billion lack access, particularly in low- and middle-income regions. This unmet demand has prompted coordinated policy efforts to expand device availability. In India, for example, a district administration distributed 461 mobility aids including motorized three-wheel bicycles and standard wheelchairs to 217 beneficiaries in May 2025, illustrating the growing emphasis on publicly funded accessibility programs.

- Technological Advancements and Device Diversification: Advances in engineering and material science have contributed to a broader range of mobility solutions. Studies from the U.S. Department of Health and Human Services reported that the use of powered wheelchairs and scooters nearly doubled over the past decade, while walkers remained twice as prevalent. These changes reflect improvements in compact motor systems, enhanced battery efficiency, and customizable controls that collectively increase performance, durability, and user autonomy.

- Digital Integration and Smart Features: Personal mobility devices are evolving into digitally integrated systems. Modern wheelchairs and scooters increasingly incorporate Bluetooth connectivity and smartphone applications for functions such as remote diagnostics, navigation assistance, and fall-detection alerts. The World Health Organization has acknowledged these digital tools as part of essential assistive technologies, reinforcing the trend toward smart and connected mobility ecosystems.

Use Cases

- Mobility Outdoors and Indoors: Older adults remain the primary users of personal mobility devices, with 2021 data showing 29.4% of U.S. adults aged 65 and above using such devices outside the home and 26.2% using them indoors. Additionally, 9.3% of this population reported using multiple device types within a month, indicating diverse mobility requirements supported by canes, walkers, and wheelchairs.

- Addressing Mobility Impairments: Assistive mobility technologies are widely used in the United States, where approximately 7.4 million individuals rely on such devices for mobility impairments. This includes nearly 4.8 million cane users, 1.80 million walker users, and 1.56 million wheelchair users. These devices are routinely prescribed to improve independence, support rehabilitation, and facilitate long-term care.

- Supporting Rehabilitation and Disability Services: Personal mobility devices play a central role in rehabilitation and disability support frameworks. In 2011, about 24% of adults aged 65 and older reported using at least one mobility aid, while 9.3% used multiple devices in the previous month. These tools contribute significantly to fall prevention, post-operative recovery, and community-based healthcare programs designed to enhance functional mobility.

- Enhancing Quality of Life in Low-Resource Settings: Government-supported distribution programs are expanding access in low-resource environments. The recent distribution of 461 assistive devices in India exemplifies how targeted initiatives can deliver substantial benefits to large groups of beneficiaries. Such programs reduce caregiver burden and improve opportunities for education, employment, and social participation among people with mobility limitations.

Frequently Asked Questions on Personal Mobility Devices

- What are personal mobility devices?

Personal mobility devices are assistive products designed to support individual movement, independence, and daily functionality. These include wheelchairs, mobility scooters, walking aids, and powered devices used by elderly individuals or persons with mobility impairments for safer, more efficient transportation. - What types of personal mobility devices are commonly used?

Commonly used personal mobility devices include manual and powered wheelchairs, mobility scooters, canes, crutches, and walkers. These devices are selected based on user mobility needs, physical condition, and the desired level of support for daily movement tasks. - Who typically uses personal mobility devices?

Personal mobility devices are typically used by elderly individuals, patients suffering from musculoskeletal disorders, and people with temporary or permanent physical disabilities. The devices are adopted to improve mobility, reduce fall risk, and enhance independence in routine indoor and outdoor activities. - What benefits do personal mobility devices provide?

Personal mobility devices provide enhanced mobility, reduced physical strain, and improved independence for users. They enable safer movement, lower caregiver burden, and support rehabilitation. Their use improves quality of life by offering stable and comfortable mobility solutions across various personal environments. - How are personal mobility devices selected?

Personal mobility devices are selected based on patient mobility level, body strength, daily activity needs, and medical recommendations. Assessment by healthcare professionals ensures appropriate device fit, safety features, and comfort, which support long-term usability and better functional outcomes. - Which product segments dominate the personal mobility devices market?

Wheelchairs and mobility scooters dominate the personal mobility devices market due to strong demand from elderly users and individuals with chronic mobility conditions. Walking aids represent another significant segment, supported by high affordability and widespread utilization in home-care settings. - Which regions are leading the market?

North America leads the personal mobility devices market due to strong healthcare infrastructure, insurance coverage, and high device adoption. Europe follows, while Asia-Pacific shows rapid growth driven by aging populations and rising investment in accessible healthcare solutions.

Conclusion

The personal mobility devices market is positioned for sustained expansion as aging populations, rising mobility impairments, and rapid urbanization continue to elevate global demand. Growth has been supported by technological advancements, improved safety features, and increased integration of digital capabilities that enhance user independence and convenience.

Strong regional adoption, particularly in North America and Europe, alongside accelerating growth in Asia Pacific, reflects broadening consumer acceptance and supportive healthcare ecosystems. Expanding government initiatives, improved accessibility programs, and ongoing product innovation are expected to strengthen market penetration further, ensuring that personal mobility devices remain essential solutions for enhanced mobility and quality of life.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)