Table of Contents

Overview

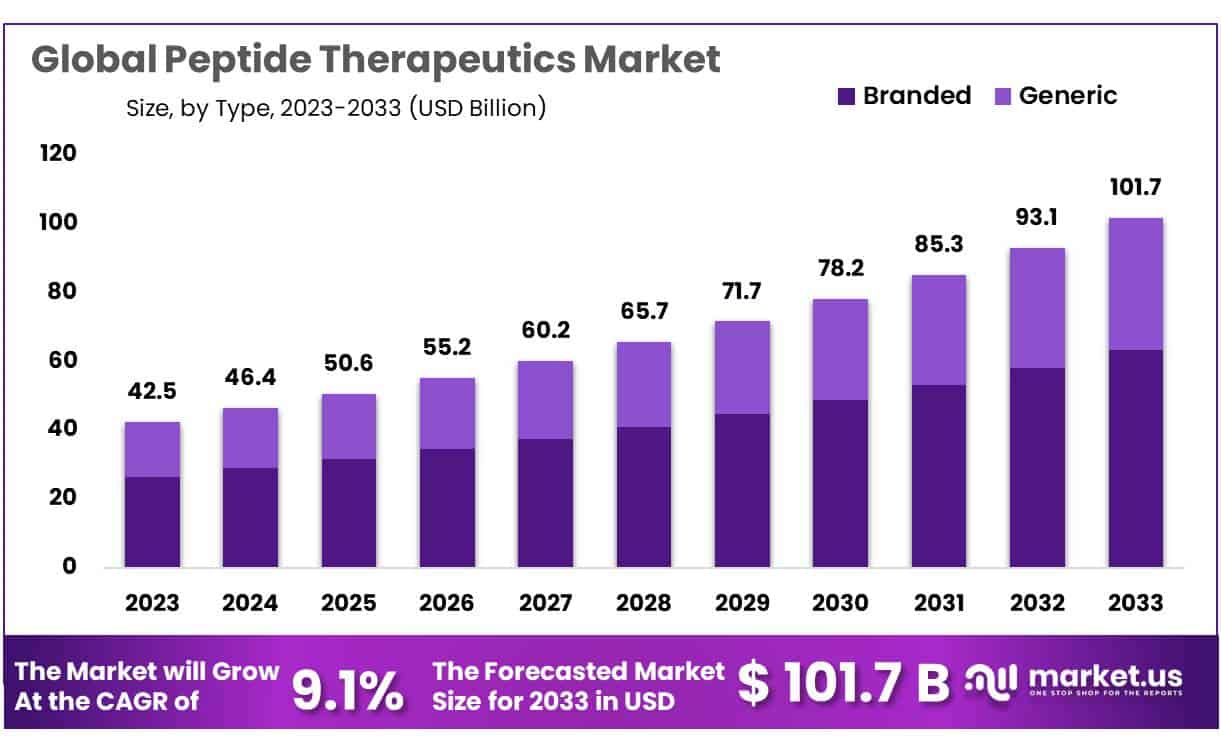

The Global Peptide Therapeutics Market is witnessing robust growth, projected to reach USD 101.7 billion by 2033 from USD 42.5 billion in 2023, at a CAGR of 9.1%. Peptide drugs, formed from short amino acid chains, provide advantages such as high selectivity, low toxicity, and strong pharmacokinetics. Their ability to target specific disease mechanisms makes them a preferred choice over traditional small molecules. Growing investments in pharmaceutical R&D, coupled with technological progress in peptide synthesis and delivery systems, are fueling demand. However, the high cost of development and strict regulatory frameworks may restrain adoption to some extent.

The rising prevalence of genetic and rare diseases is a significant growth driver. Oligonucleotide synthesis, closely linked with peptide therapeutics, is essential in diagnostics and therapeutics for conditions such as cancer, neurological disorders, and metabolic syndromes. The increasing demand for targeted therapies has reinforced the adoption of custom, high-quality oligonucleotides. With the rise in genetic testing and advanced diagnostics, market opportunities for both peptides and oligonucleotides are expanding, reflecting a strong synergy in their applications across healthcare.

Personalized and precision medicine are expanding rapidly, further supporting growth in these segments. Oligonucleotides enable accurate modulation of gene expression and are critical for therapies aligned with patient-specific genetic profiles. Pharmaceutical companies and research institutions are investing in tailored solutions, strengthening the demand base. Clinical trial success, coupled with regulatory approvals of antisense oligonucleotides and small interfering RNAs, has accelerated commercialization, adding momentum to the overall market landscape.

Technological advancements in synthesis platforms are enhancing efficiency and reducing costs. Automated and solid-phase synthesis methods, along with AI-driven design tools, are improving yields and lowering error rates. These innovations support large-scale and accurate production, which is essential to meet the growing clinical and commercial demand. Parallel synthesis systems and miniaturization techniques are also contributing to scalability, making peptide and oligonucleotide production more accessible for both large pharmaceutical firms and smaller biotech players.

Investment in biotechnology, genomics, and molecular diagnostics continues to expand. Public and private funding are driving applications in gene editing, next-generation sequencing, and disease surveillance. Oligonucleotides and peptides are increasingly used in research, agriculture, and forensic science, widening their scope beyond therapeutics. Outsourcing to specialized CDMOs is another trend, offering scalability, compliance, and cost advantages. Strategic collaborations among pharmaceutical companies, CROs, and research institutes are strengthening development pipelines and ensuring market sustainability through innovation and regulatory support.

Key Takeaways

- The global peptide therapeutics market is projected to reach USD 101.7 billion by 2033, rising from USD 42.5 billion in 2023.

- The market is expected to expand at a compound annual growth rate of 9.1% during the forecast period between 2024 and 2033.

- Branded peptide therapeutics accounted for the largest revenue contribution, representing 62.4% of the overall market share in 2023.

- In terms of application, the metabolic disorders segment dominated the market with a 36.2% revenue share in 2023.

- The parenteral route of administration emerged as the leading segment, contributing 66.7% of the market’s total revenue share in 2023.

- Distribution through hospital channels remained the most lucrative, registering a 60.1% share of total revenues in 2023.

- North America accounted for the largest regional market share, representing 35.7% of the global peptide therapeutics market in 2023.

- Increasing prevalence of chronic diseases, particularly cancer and diabetes, continues to accelerate the adoption of peptide therapeutics worldwide.

- Significant investments in research and development by pharmaceutical companies are fueling continuous innovation and growth within the peptide therapeutics market.

- Rising adoption of biologics, including peptide therapeutics, is driven by their therapeutic specificity and high effectiveness in targeted treatments.

Regional Analysis

Segmentation Analysis

The branded type of peptide therapeutics accounted for the highest market share in 2023, representing 62.4% of total revenue. The dominance of branded products can be attributed to strong brand loyalty and the development of novel drugs. However, the generic segment is expected to grow significantly during the forecast period. Expansion of generic drug usage is being supported by increased healthcare spending by governments. Moreover, patent expirations of several branded peptide drugs are expected to create opportunities for generic manufacturers to enter the market with cost-effective alternatives.

The metabolic disorders segment emerged as the largest application area in 2023, holding a share of 36.2% of the global peptide therapeutics market. Rising incidences of metabolic diseases such as diabetes are major factors supporting the dominance of this segment. Cancer represented the second-largest application, driven by increasing adoption of peptide-based therapies in oncology treatments. The rising global cancer burden and growing preference for effective, targeted, and fast-acting peptide medicines are likely to accelerate market growth in this segment over the forecast period.

Parenteral administration accounted for the largest share of 66.7% of the peptide therapeutics market in 2023. This route remains the preferred method due to improved absorption, quicker onset of action, and superior therapeutic outcomes compared to other methods. The demand for parenteral delivery is further reinforced by advancements in drug delivery technologies. Although oral and other alternative routes are gaining traction, parenteral administration continues to dominate due to its efficacy in delivering complex peptide-based drugs, especially for patients requiring fast and precise therapeutic interventions.

Hospitals held the largest share in the distribution channel analysis, accounting for 60.1% of the global peptide therapeutics market in 2023. The dominance of hospitals is due to their advanced infrastructure, availability of specialized equipment, and skilled professionals required for handling and administering peptide therapeutics. These treatments are complex and often require continuous monitoring, making hospitals the most suitable distribution channel. While retail pharmacies and online platforms contribute to distribution, they mainly serve for less complex drugs, leaving hospitals as the primary centers for peptide-based therapeutic treatments.

Key Players Analysis

The global peptide therapeutics market is shaped by leading companies such as Ipsen, Sanofi, Pfizer, Lonza Group, Merck KGaA, and Sandoz International. These players are actively engaged in developing advanced peptide-based drugs with enhanced safety and efficacy. Their established research infrastructure and strategic collaborations strengthen their presence in this highly competitive market. Continuous investment in innovation and expansion into emerging economies are anticipated to support market penetration and long-term growth opportunities in the peptide therapeutics segment.

Ipsen and Sanofi are key European pharmaceutical firms advancing peptide research. Ipsen is noted for its innovative pipeline targeting oncology and rare diseases, while Sanofi focuses on therapeutic peptides for metabolic and immunological disorders. Both companies are strengthening their portfolios through collaborations and clinical trials. Their contributions are expected to enhance treatment outcomes and increase patient accessibility. This strategic emphasis on novel peptide solutions positions them as strong competitors in the global peptide therapeutics industry.

Pfizer, Lonza Group, Merck KGaA, and Sandoz International also play pivotal roles in driving industry growth. Pfizer leverages its large-scale research programs and global reach to expand peptide drug availability. Lonza Group specializes in peptide manufacturing technologies, enabling scalable production. Merck KGaA focuses on advancing peptide-based therapies in oncology and immunology. Meanwhile, Sandoz International strengthens its generics portfolio with cost-effective peptide drugs. Collectively, these companies contribute to accelerating innovation and expanding the commercial landscape of peptide therapeutics worldwide.

Conclusion

The oligonucleotide synthesis market is expanding steadily, supported by growing applications in advanced diagnostics, precision medicine, and genetic research. The increasing use of oligonucleotides in cancer treatment, neurological therapies, and metabolic disease management highlights their clinical importance. Advances in synthesis technology, including automation and AI integration, are improving efficiency and reducing errors, making production more scalable and cost-effective. Strong investments from pharmaceutical firms and research institutions, coupled with rising demand for personalized medicine, continue to fuel market growth. Strategic collaborations and outsourcing to specialized CDMOs are further strengthening the supply chain, ensuring innovation and sustainable development in this evolving healthcare segment.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)