Table of Contents

Overview

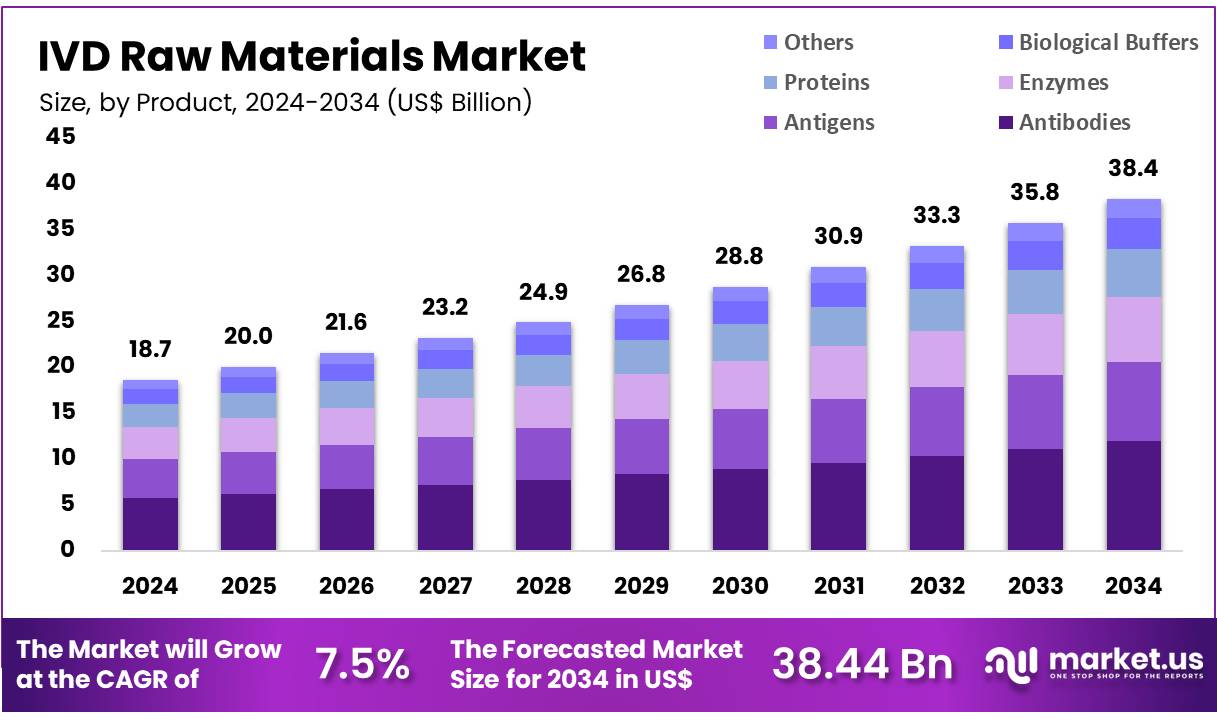

New York, NY – Nov 14, 2025 – Global IVD Raw Materials Market size is expected to be worth around US$ 38.44 Billion by 2034 from US$ 18.65 Billion in 2024, growing at a CAGR of 7.5% during the forecast period 2025 to 2034. In 2023, North America led the market, achieving over 34.8% share with a revenue of US$ 6.49 Billion.

The global In Vitro Diagnostic (IVD) raw materials market has been witnessing steady expansion as demand for reliable diagnostic solutions continues to rise across clinical and research settings. The growth of the market can be attributed to increasing test volumes, widening adoption of molecular diagnostics, and a sustained shift toward high-quality biological reagents and consumables. Strong emphasis on accuracy and reproducibility has elevated the requirements for antibodies, antigens, enzymes, proteins, and specialized chemicals that serve as the core components of IVD assay development.

The industry has been shaped by the expanding burden of chronic and infectious diseases, which has driven laboratories and manufacturers to prioritize robust supply chains and advanced material performance. Strategic collaborations between raw-material suppliers and diagnostic manufacturers have been observed, enabling accelerated development of innovative assay platforms. Consistent investment in R&D has supported the advancement of recombinant materials, synthetic controls, and high-purity reagents designed to enhance test sensitivity and specificity.

The market outlook remains positive as regulatory frameworks continue to reinforce quality standards, encouraging adoption of compliant and traceable materials. Growing demand for point-of-care testing and personalized diagnostics is expected to create new opportunities for raw material suppliers. Emerging trends indicate increased integration of automation-ready components and sustainable material sourcing to support long-term scalability.

This press release highlights the expanding significance of IVD raw materials in strengthening global diagnostic capabilities, underscoring their critical role in enabling accurate, efficient, and high-performance testing solutions.

Key Takeaways

- The global IVD raw materials market generated revenue of US$ 65 billion in 2024, supported by a CAGR of 7.5%, and is projected to attain US$ 38.44 billion by 2033.

- The product type segment comprises Antibodies, Antigens, Enzymes, and Proteins, with Antibodies accounting for the leading share of 31.1% in 2023.

- By technology, the market is categorized into Molecular Diagnostics, Clinical Chemistry, Immunochemistry, and Others, with Molecular Diagnostics dominating at 37.4% of the market share.

- In terms of end users, the market is segmented into Pharmaceutical and Biotechnology Companies, Diagnostic Laboratories, Contract Research Organizations, and Others. Diagnostic Laboratories emerged as the leading segment with a 38.3% revenue share.

- North America*held the largest regional share, securing 34.8% of the market in 2023.

Regional Analysis

The IVD raw materials market in North America has recorded significant expansion and is projected to maintain its growth trajectory, holding a leading share of 34.8% in 2024. This advancement is attributed to the region’s well-established healthcare infrastructure and the increasing burden of chronic diseases. The United States continues to dominate the regional market due to rising healthcare spending and the accelerated adoption of point-of-care testing and companion diagnostics.

The increasing prevalence of chronic illnesses has been driving the demand for in-vitro diagnostic testing, which is essential for the detection and management of numerous medical conditions. A study released in January 2023 in Frontiers in Public Health estimated that by 2050, more than 143 million Americans aged 50 and above will be affected by at least one chronic disease. This projected surge in chronic health conditions is expected to elevate the need for IVD solutions, thereby increasing the consumption of IVD raw materials and supporting regional market growth.

Market expansion is also encouraged by strategic initiatives undertaken by companies in the United States and Canada, including product launches and regulatory approvals. For instance, in May 2022, BioMérieux obtained approval from the Government of Canada for its BioFire Blood Culture Identification 2 (BCID2) panel, developed for the rapid identification of bloodstream infections. The panel provides an expanded list of pathogens, a wider set of antimicrobial resistance genes, and updated diagnostic targets, offering notable improvements over the original BCID panel.

Use Cases

- Molecular Diagnostic Assay Kits: IVD raw materials such as primers, probes, and controls serve as the foundation for rRT-PCR assay kits. The CDC’s H7N9 virus detection kit provides reagents for 200 reactions, enabling rapid identification of avian influenza strains. These kits support early outbreak detection and strengthen ongoing surveillance programs in clinical laboratory environments.

- Specimen Transport and Preservation: Viral transport media (VTM) remains a key component for specimen collection workflows. According to CDC guidelines, VTM is approved for at least seven specimen types, including NP/OP swabs and lesion swabs, with recommended storage at 2–8 °C for seven days before freezing or analysis. This functionality supports reliable, high-throughput testing across centralized and decentralized laboratory operations.

- Quality Control Panels for Assay Validation: WHO’s Technical Guidance Series (TGS–6) describes standardized methods for preparing validated QA/QC panels using defined raw materials. These panels contain reference strains, antigen preparations, and controls that manufacturers use to assess assay sensitivity and specificity before commercial release. Implementation of such panels has been associated with improved lot-to-lot consistency in global diagnostic markets.

- Broad-Panel Diagnostic Test Directories: The CDC’s 2024 Infectious Diseases Laboratory Test Directory (Version 30.0) lists more than 400 diagnostic tests and outlines required raw materials such as culture media, molecular reagents, and antigen-specific antibodies. This directory functions as a reference tool for laboratories when sourcing materials and developing efficient test workflows.

Frequently Asked Questions on IVD Raw Materials

- Why are IVD raw materials important?

The importance of IVD raw materials is derived from their role in sustaining assay reliability, reducing batch variation, and enabling consistent diagnostic outcomes. High-quality materials improve test accuracy, operational efficiency, and overall clinical decision-making effectiveness. - What types of raw materials are commonly used in IVD manufacturing?

Common IVD raw materials include antibodies, antigens, enzymes, proteins, nucleic acids, buffers, stabilizers, and polymers. These components enable biochemical reactions, signal detection, and molecular binding processes necessary for producing accurate diagnostic test results. - What factors influence the quality of IVD raw materials?

The quality of IVD raw materials is influenced by purity levels, stability, source reliability, reproducibility, regulatory compliance, and traceability. These factors directly affect assay consistency, product safety, and overall diagnostic performance in laboratory and point-of-care settings. - Who uses IVD raw materials?

IVD raw materials are utilized by diagnostic manufacturers, research laboratories, biotech firms, and healthcare organizations engaged in developing test kits. These end users rely on high-performance inputs to support innovation in molecular diagnostics, immunoassays, and clinical chemistry. - Which segments dominate the IVD raw materials market?

The market is dominated by antibodies, enzymes, and antigens, which support immunoassay and molecular platforms. Demand for recombinant materials has increased due to their consistency, batch stability, and suitability for high-performance diagnostic applications. - Which regions lead the IVD raw materials market?

North America and Europe lead the market due to strong diagnostic infrastructure, advanced biotechnology capabilities, and significant R&D investments. Asia-Pacific is emerging rapidly as manufacturing expansion and healthcare spending continue to accelerate regional market uptake. - What trends are shaping the IVD raw materials market?

Key trends include adoption of recombinant proteins, automation-compatible reagents, sustainable sourcing practices, and increased reliance on nucleic acid-based materials. Growing preference for high-purity and contamination-free components is strengthening innovation across diagnostics. - What is the future outlook for the IVD raw materials market?

The market outlook remains positive as demand for early disease detection, decentralized testing, and personalized diagnostics grows. Increased investment in biotechnology and sustainable material production is expected to support consistent long-term expansion.

Conclusion

The global IVD raw materials market is positioned for sustained advancement as diagnostic demand increases across clinical and research environments. Growth has been supported by rising test volumes, expanding molecular diagnostics, and stricter quality expectations for high-purity biological inputs. Strong regional performance, particularly in North America, reflects robust healthcare spending and accelerating adoption of advanced testing technologies.

Strategic collaborations, regulatory reinforcement, and innovation in recombinant and automation-ready materials continue to strengthen market competitiveness. Expanding application areas, including point-of-care testing and personalized medicine, are expected to create additional opportunities, ensuring continued progress and long-term market resilience.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)