Table of Contents

Overview

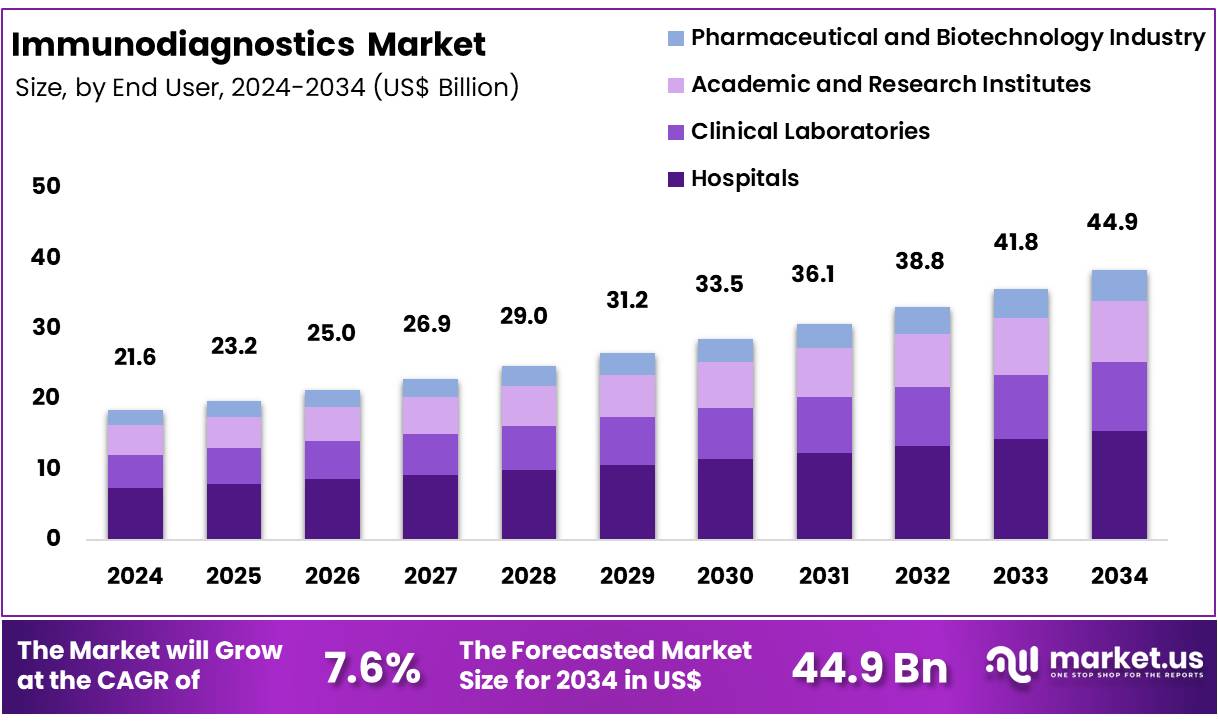

New York, NY – Nov 26, 2025 – Global Immunodiagnostics Market size is expected to be worth around US$ 44.9 Billion by 2034 from US$ 21.6 Billion in 2024, growing at a CAGR of 7.6% during the forecast period from 2025 to 2034. In 2024, North America led the market, achieving over 45.6% share with a revenue of US$ 9.8 Billion.

The global immunodiagnostics landscape is undergoing steady expansion as demand for precise, rapid, and minimally invasive diagnostic solutions continues to rise. Immunodiagnostic technologies are being adopted widely across hospitals, laboratories, and point-of-care settings, as detection accuracy for infectious diseases, oncology biomarkers, and autoimmune disorders has been significantly improved. Market growth has been supported by increasing disease awareness, expanding screening programs, and ongoing investments in diagnostic innovation.

Immunoassays, including ELISA, chemiluminescence assays, and rapid tests, remain central to this industry. Their adoption has been driven by high sensitivity, strong reproducibility, and compatibility with automated systems. The growth of the market has been attributed to technological enhancements that enable faster turnaround times and higher throughput, addressing the rising volume of diagnostic testing worldwide.

Chronic disease prevalence continues to increase globally, and this trend has resulted in sustained demand for early-stage detection tools. Immunodiagnostic platforms play a critical role in identifying biomarkers linked to cardiovascular diseases, diabetes, and cancer. Industry stakeholders are prioritizing the development of advanced assays capable of supporting personalized treatment approaches.

Strong regulatory support, combined with the expansion of molecular-immunodiagnostic integration, is expected to reinforce innovation over the coming years. Major companies are focusing on product pipeline expansion, automation upgrades, and strategic collaborations to strengthen their competitive positions.

The immunodiagnostics market is anticipated to maintain a positive outlook as healthcare systems emphasize accuracy, efficiency, and preventive diagnostics. Continued advancements are likely to enhance global diagnostic capabilities and support improved patient outcomes.

Key Takeaways

- Market Size: The global immunodiagnostics market is projected to reach US$ 44.9 billion by 2034, rising from US$ 21.6 billion in 2024.

- Market Growth: The market is forecast to expand at a CAGR of 7.6% between 2025 and 2034.

- Product Analysis: Reagents and consumables constituted the largest product category in 2024, representing 45.6% of total market share.

- Technology Analysis: The ELISA segment dominated the technology landscape, accounting for 36.4% of the market share.

- Application Analysis: Infectious diseases remained the leading application area, contributing 31.2% of overall market demand.

- End-Use Analysis: Hospitals held the highest share among end users, representing 34.5% of the market in 2024.

- Regional Analysis: North America led the global market in 2024 with over 45.6% share, generating approximately US$ 9.8 billion in revenue.

Segmentation Analysis

Product Analysis: The immunodiagnostics market is categorized into reagents and consumables, instruments, software, and services. Reagents and consumables accounted for 45.6% of the market in 2024, supported by continuous demand for assay kits, calibrators, and buffer solutions. Instruments, including automated analyzers, are utilized to improve workflow efficiency and reduce manual intervention.

Software solutions enable data management, regulatory compliance, and process standardization. Services such as system calibration, maintenance, and operator training are essential for ensuring consistent performance. Together, these segments facilitate reliable diagnostic operations across clinical, academic, and research settings.

Technology Analysis: Key technologies in the market include ELISA, CLIA, Fluorescent Immunoassay, RIA, and Rapid Tests. ELISA held a 36.4% share due to its high reliability and extensive diagnostic application range. CLIA adoption is rising as its enhanced sensitivity and rapid processing are preferred in hormone and metabolic testing.

Fluorescent immunoassays are increasingly applied in point-of-care environments. RIA usage continues to decline owing to radiation-related safety concerns, although it remains relevant in select research laboratories. Rapid Tests are expanding steadily, supported by strong uptake in infectious disease detection and home-based testing.

Application Analysis: Immunodiagnostics are used across several therapeutic applications, including Infectious Diseases, Oncology, Endocrinology, Hepatitis, Bone & Mineral, Autoimmunity, and Others. Infectious Diseases dominated with 31.2% share, driven by the global burden of conditions such as COVID-19, TB, and influenza.

Oncology and Endocrinology segments maintain strong growth due to increasing cancer prevalence and rising hormone-related disorders. Hepatitis and Retrovirus diagnostics show consistent utilization worldwide. Bone and Mineral testing is expanding with aging demographics, while autoimmunity and other emerging applications such as allergy testing continue to gain traction.

End-User Analysis: End users include Hospitals, Clinical Laboratories, Academic and Research Institutes, and the Pharmaceutical and Biotechnology Industry. Hospitals led with 34.5% share, reflecting high patient inflow and the need for rapid diagnostic decision-making. Clinical laboratories represent the next major segment, supported by increased outsourcing of tests and the growth of private diagnostic centers.

Academic and research institutions contribute through biomarker discovery and immunology research. Pharmaceutical and biotechnology companies rely heavily on immunodiagnostics for drug development, safety evaluation, and clinical study support, strengthening overall market adoption.

Regional Analysis

In 2024, North America maintained a dominant position in the global immunodiagnostics market, accounting for more than 45.6% of total revenue and reaching a market value of US$ 9.8 billion. This leadership has been supported by a mature healthcare infrastructure and consistently high diagnostic testing volumes across the region.

The strong presence of technologically advanced hospitals and clinical laboratories has facilitated the widespread adoption of automated immunoassay platforms. In addition, healthcare expenditure per capita remains significantly higher than global averages, strengthening the uptake of advanced diagnostic solutions.

The increasing prevalence of chronic and infectious diseases has further elevated the demand for early and accurate diagnostic testing. According to the U.S. Centers for Disease Control and Prevention (CDC), chronic diseases are responsible for approximately 70% of all deaths in the country. As a result, immunodiagnostic testing plays a central role in routine disease management and long-term monitoring.

Widespread implementation of preventive screening programs, supportive reimbursement frameworks, and growing utilization of point-of-care diagnostic devices contribute to the region’s robust market performance. Government-led disease surveillance systems and public health initiatives continue to enhance diagnostic awareness and accessibility. Collectively, these factors reinforce North America’s position as a major growth engine in the global immunodiagnostics market.

Frequently Asked Questions on Immunodiagnostics

- How do immunodiagnostic tests work?

Immunodiagnostic tests operate through highly specific antigen–antibody binding mechanisms. The formation of these complexes enables the detection and quantification of disease-related biomarkers, supporting early diagnosis, disease monitoring, and therapeutic guidance across various clinical applications. - What are the major types of immunodiagnostic assays?

The major assay types include ELISA, chemiluminescence immunoassays, radioimmunoassays, rapid tests, and immunofluorescence assays. Each technique offers varied sensitivity and throughput levels, enabling broad utility in clinical laboratories, point-of-care settings, and specialized diagnostic workflows. - Which diseases are commonly diagnosed using immunodiagnostics?

Immunodiagnostics are widely used for infectious diseases, cancer biomarkers, cardiovascular markers, allergy testing, and autoimmune disorders. These tests enable early detection, risk assessment, and therapeutic monitoring across diverse clinical specialties, improving overall diagnostic accuracy. - What are the key advantages of immunodiagnostics?

Key advantages include high specificity, rapid detection, broad analyte coverage, and compatibility with automated platforms. These benefits support increased laboratory efficiency, improved clinical accuracy, and the expanding use of immunoassays in routine diagnostic testing. - How is automation influencing immunodiagnostics?

Automation enhances immunodiagnostics through improved throughput, reduced manual error, and standardized assay performance. Automated analyzers support continuous workflow optimization, enabling laboratories to handle increasing test volumes and meet rising global demand for high-accuracy diagnostics. - What technological trends are shaping immunodiagnostics?

Key trends include digital immunoassay development, multiplex testing, biomarker discovery, high-sensitivity platforms, and integration with molecular diagnostics. These advancements support improved clinical decision-making and accelerate the shift toward precision-driven diagnostic solutions. - Which segments dominate the immunodiagnostics market?

Key segments include reagents, analyzers, and consumables, with infectious disease and oncology applications generating substantial demand. Automated analyzers are increasingly dominating due to the industry’s shift toward high-throughput and standardized testing environments. - Which regions lead the immunodiagnostics market?

The market is led by North America and Europe due to advanced healthcare infrastructure and high diagnostic adoption. Significant growth is observed in Asia-Pacific as rising healthcare expenditure and expanding laboratory capacity increase immunoassay utilization.

Conclusion

The global immunodiagnostics market is expected to sustain steady expansion, supported by rising diagnostic demand, technological progress, and growing emphasis on early disease detection. Strong adoption of immunoassays across hospitals, laboratories, and point-of-care settings continues to drive market performance.

North America maintains a leading position due to advanced healthcare systems and high testing volumes. Increasing chronic disease prevalence and ongoing biomarker innovation are reinforcing long-term growth prospects. The market outlook remains positive as automation, molecular integration, and personalized diagnostics strengthen clinical accuracy, operational efficiency, and overall healthcare outcomes worldwide.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)