Table of Contents

Overview

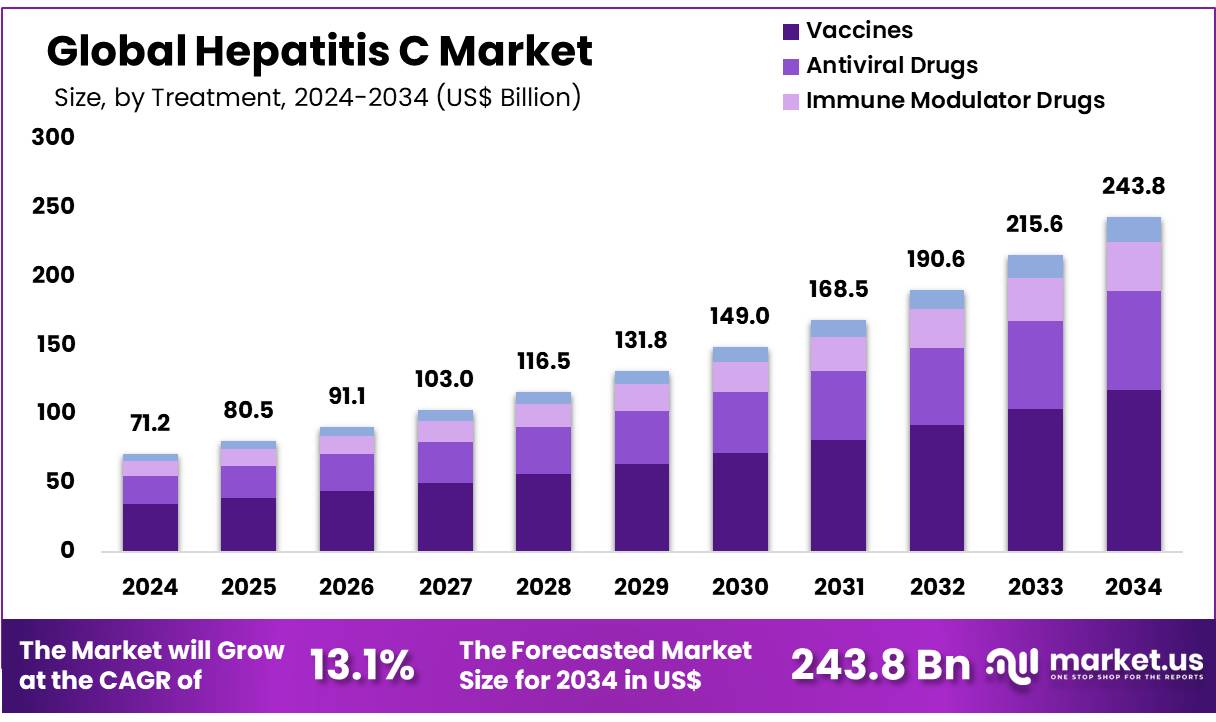

New York, NY – Nov 20, 2025 – Global Hepatitis C Market size is expected to be worth around US$ 243.8 Billion by 2034 from US$ 71.2 Billion in 2024, growing at a CAGR of 13.1% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 42.2% share with a revenue of US$ 30.0 Billion.

A rising focus on viral disease management has renewed global attention on Hepatitis C, a blood-borne infection that continues to present a significant public health burden worldwide. Hepatitis C is caused by the Hepatitis C virus (HCV), which primarily targets the liver and can progress from acute infection to chronic disease if left untreated. Transmission is mainly associated with exposure to infected blood, including unsafe injection practices, inadequate medical sterilization, and, less commonly, from mother to child during birth.

The progression of the disease is often silent, as many individuals remain asymptomatic for years. As a result, diagnoses are frequently made at advanced stages when liver damage such as cirrhosis or hepatocellular carcinoma has already developed. Early screening has therefore been recognized as a critical component in improving treatment outcomes. Blood tests that detect HCV antibodies and viral RNA are widely used to confirm infection.

Significant progress in treatment has been observed with the introduction of direct-acting antiviral therapies. These therapies have contributed to cure rates exceeding 95 percent in most patient groups, and treatment durations have been substantially reduced. Improved accessibility to these therapies has strengthened global elimination efforts.

Greater awareness, expanded screening programs, and enhanced access to effective treatment continue to drive advancements in Hepatitis C prevention and control. Public health agencies, healthcare providers, and patient-focused organizations are encouraging early detection and consistent treatment to reduce disease burden and support long-term liver health.

Key Takeaways

- The global hepatitis C market generated revenue of US$ 71.2 Billion in 2024, supported by a CAGR of 13.1%, and it is projected to reach US$ 243.8 Billion by 2033.

- The treatment segment comprises vaccines, antiviral drugs, immune modulator drugs, and others, with vaccines accounting for 48.3% of the market share in 2024.

- In diagnostics, the market is categorized into liver biopsy, imaging tests, blood tests, and others, where imaging tests represented 41.7% of the share.

- Based on the route of administration, the market includes oral, parenteral, and others, with the oral route dominating at 58.3% revenue share.

- The end-user landscape consists of hospitals, homecare, specialty clinics, and others, and hospitals remained the leading segment with 52.2% share.

- North America emerged as the leading regional market, capturing 42.2% of the global share in 2024.

Regional Analysis

North America is leading the Hepatitis C Market

North America accounted for the largest revenue share of 42.2%, supported by advancements in therapeutic options, expanded screening initiatives, and strong governmental commitments to disease elimination. Data from the Centers for Disease Control and Prevention (CDC) indicated that approximately 66,700 new chronic hepatitis C cases were reported in the United States in 2022, underscoring the persistent demand for improved diagnostics and effective treatment. The adoption of direct-acting antivirals (DAAs), which demonstrate cure rates above 95%, has been a major contributor to regional market growth.

The US Department of Health and Human Services (HHS) reported that more than 1 million patients in the United States have received DAA therapy since its introduction, supported by broader treatment access through Medicaid expansion and state-level funding mechanisms.

In Canada, the Canadian Institute for Health Information (CIHI) noted a 15% rise in hepatitis C-related healthcare expenditure between 2022 and 2023, reflecting heightened national efforts toward disease elimination. Public health initiatives, including the CDC’s Hepatitis C Elimination Plan, have strengthened diagnosis rates and treatment uptake. These developments, coupled with rising awareness and advanced healthcare systems, have reinforced North America’s leading position in the hepatitis C market.

Asia Pacific is expected to experience the highest CAGR

The Asia Pacific region is projected to register the fastest CAGR, driven by increasing disease prevalence, expanding healthcare access, and strong government-led elimination programs. The World Health Organization (WHO) estimated that over 70 million individuals in the region were living with chronic hepatitis C in 2022, with India and China representing a major share.

India’s National Health Mission reported a 25% increase in screening and diagnostic activities between 2022 and 2023, aided by the availability of cost-effective generic DAAs. In China, the National Health Commission stated that more than 1.5 million individuals had received treatment by 2023, with efforts focused on improving access in rural communities.

Australia’s National Hepatitis C Strategy, which targets disease elimination by 2030, contributed to a 30% rise in treatment initiations between 2022 and 2023. With growing regional cooperation, enhanced diagnostic technologies, and rising investments in healthcare systems, Asia Pacific is poised to become a central contributor to global hepatitis C elimination efforts.

Emerging Trends

- Increase in Acute Infections: A rise in acute hepatitis C infections was recorded in 2023, with 4,966 cases reported across 47 states and the District of Columbia, reflecting an estimated 69,000 new infections nationwide. The increase was most evident among adults aged 18–39, indicating persistent transmission in high-risk groups.

- Expansion of Universal Screening: Universal screening is now recommended for all adults aged 18 and older at least once, and for all pregnant women during each pregnancy, except in regions with prevalence below 0.1 percent. This shift supports earlier diagnosis through routine primary care and obstetric testing.

- Advancements in Diagnostic Technology: New diagnostic tools, including advanced HCV core antigen assays, are under development to simplify detection. These one-step tests allow identification of active infections without multiple laboratory visits, helping accelerate diagnosis and treatment in diverse healthcare settings.

- Ambitious Elimination Targets: Global and national strategies aim to test 90 percent of infected individuals and treat at least 80 percent of diagnosed cases by 2030. Modeling shows that meeting these goals could avert 10 million new infections and prevent approximately 2.1 million deaths worldwide.

Use Cases

- Harm Reduction Programs: Needle-exchange and safe-injection initiatives have been adopted in areas with high transmission among people who inject drugs. Between 2020 and 2023, infection rates in this group declined from 2.6 to 1.7 per 100,000, highlighting the effectiveness of targeted interventions.

- Routine Screening in Healthcare Settings: Primary care and obstetric facilities have integrated hepatitis C testing into routine examinations, leading to increased detection. In 2023 alone, over 100,000 new chronic cases were identified, many uncovered through standardized screening rather than risk-based approaches.

- Direct-Acting Antiviral Treatment: Direct-acting antivirals are widely accessible and provide cure rates exceeding 95 percent with 8–12 weeks of therapy. More than 1 million individuals in the United States have received treatment, contributing to significant reductions in severe liver-related outcomes.

- National Elimination Campaigns: Countries are implementing coordinated elimination strategies involving mass screening, rapid diagnostics, and subsidized treatment. Projections indicate that scaling testing to 90 percent and treating 80 percent of cases could prevent millions of future infections and deaths by 2030.

Frequently Asked Questions on Hepatitis C

- What is Hepatitis C?

Hepatitis C is a viral infection affecting the liver, caused by the hepatitis C virus. It is primarily transmitted through infected blood and may progress from acute to chronic disease, leading to long-term liver complications if untreated. - How is Hepatitis C transmitted?

Transmission occurs mainly through exposure to contaminated blood, including unsafe injections, non-sterile medical procedures, or sharing needles. Less common routes include sexual contact and mother-to-child transmission during childbirth. - What are the symptoms of Hepatitis C?

Most individuals remain asymptomatic for years, making early detection difficult. When symptoms appear, they may include fatigue, jaundice, abdominal pain, and dark urine, indicating possible liver inflammation or damage. - What is driving growth in the Hepatitis C market?

Market growth is driven by rising disease prevalence, expanded screening programs, and increased adoption of direct-acting antivirals. Government funding and improved healthcare access also contribute to sustained expansion across major regions. - Which treatment segment leads the Hepatitis C market?

The vaccine segment accounted for the largest market share in 2024. Its dominance is supported by rising immunization initiatives, technological advancements, and global efforts aimed at preventing disease transmission and recurrence. - Which route of administration is most preferred?

The oral administration segment dominated the market due to its convenience, better patient compliance, and widespread adoption of oral direct-acting antivirals, which provide high cure rates with minimal treatment complexity. - Which region leads the global Hepatitis C market?

North America led the global market with a significant share. Strong healthcare infrastructure, expanded access to antiviral therapies, and government-supported elimination initiatives continue to drive regional demand and market leadership.

Conclusion

The global hepatitis C market is positioned for sustained expansion, supported by rising disease awareness, advances in diagnostics, and strong adoption of highly effective direct-acting antivirals. Growth has been reinforced by national elimination strategies, expanding screening programs, and improved treatment accessibility across developed and emerging regions.

North America continues to lead due to robust healthcare systems, while Asia Pacific is expected to witness the fastest growth driven by large patient populations and government-led interventions. Ongoing innovation in diagnostic technologies, universal screening recommendations, and harm-reduction initiatives further strengthen global efforts toward reducing disease burden and achieving long-term elimination targets.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)