Table of Contents

Overview

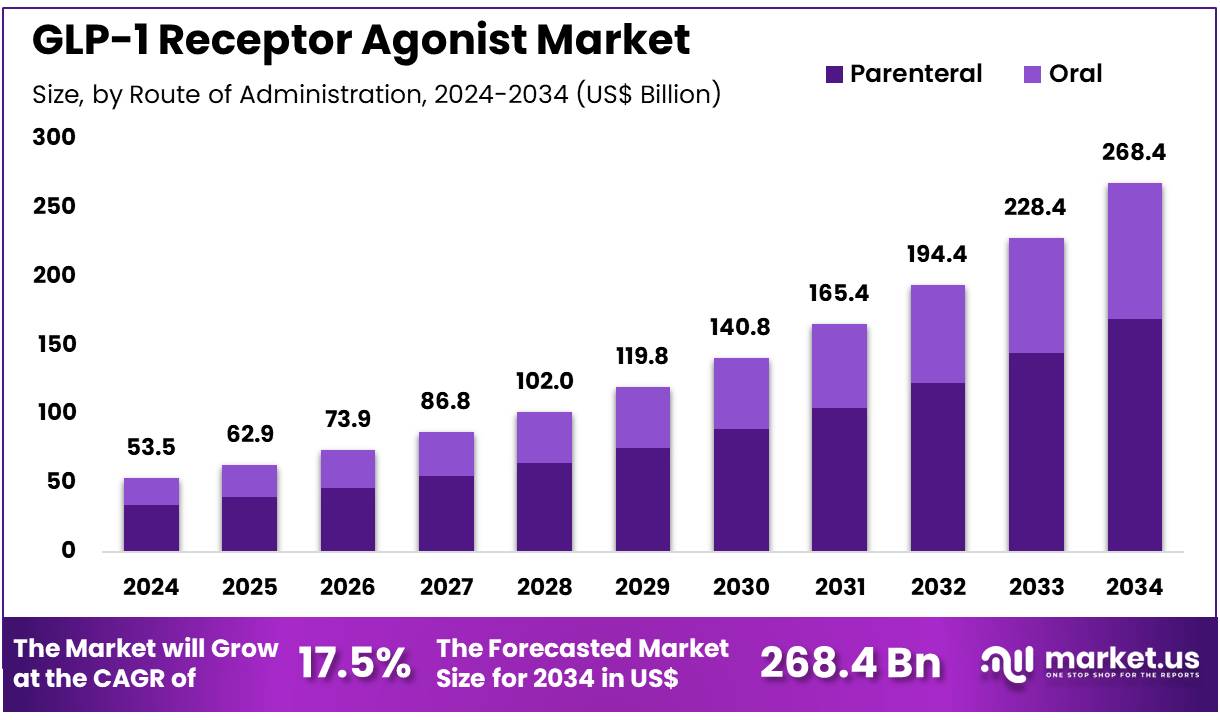

New York, NY – Nov 27, 2025 – Global GLP-1 Receptor Agonist Market size is expected to be worth around US$ 268.4 billion by 2034 from US$ 53.5 billion in 2024, growing at a CAGR of 17.5% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 49.7% share with a revenue of US$ 26.6 Billion.

The GLP-1 receptor agonist market has been characterized by robust expansion as demand for effective therapies for type 2 diabetes and obesity has increased steadily. Growth of the segment has been attributed to strong clinical outcomes associated with this class of drugs, including improved glycemic control, reduced appetite, and significant weight reduction. The mechanism of action is based on the stimulation of the glucagon-like peptide-1 receptor, which enhances insulin secretion, slows gastric emptying, and supports overall metabolic regulation.

A notable rise in global prevalence of diabetes and obesity has accelerated product adoption in both developed and emerging markets. Industry momentum has been further supported by continuous innovations, such as once-weekly formulations and expanded indications for chronic weight management. Increasing investment in research and development has strengthened the competitive landscape, while strategic collaborations among pharmaceutical manufacturers have broadened commercial reach.

Market performance has also benefited from growing physician acceptance, favorable clinical evidence, and improved patient adherence due to enhanced delivery systems. Regulatory approvals for next-generation molecules are expected to stimulate additional opportunities across therapeutic applications. As healthcare systems prioritize chronic disease management, GLP-1 receptor agonists are positioned to remain a critical component of treatment protocols.

The outlook for the market remains positive, supported by rising health awareness, expanding reimbursement frameworks, and sustained technological advancement. Strong demand for metabolic disorder therapies is expected to continue driving market progression over the forecast period.

Key Takeaways

- In 2024, the GLP-1 receptor agonist market generated revenue of US$ 53.5 billion, supported by a CAGR of 17.5%, and the market is projected to attain US$ 268.4 billion by 2033.

- The product type segment includes semaglutide, liraglutide, exenatide, dulaglutide, and others, with semaglutide leading the market in 2024, accounting for 58.4% of total share.

- Based on route of administration, the market is categorized into parenteral and oral, where parenteral formulations dominated with a 63.2% share.

- In terms of application, segmentation covers type 2 diabetes mellitus, obesity, and others, with type 2 diabetes mellitus holding the largest share at 62.3%.

- The distribution channel segment comprises hospital pharmacies, online pharmacies, and retail pharmacies, and hospital pharmacies led the market with a 57.8% revenue contribution.

- North America emerged as the leading regional market, capturing 49.7% of the global share in 2024.

Regional Analysis

North America Leading the GLP-1 Receptor Agonist Market

North America accounted for the largest revenue share of 49.7%, supported by the high prevalence of type 2 diabetes and obesity, a developed healthcare system, and favorable reimbursement structures. Data from the Centers for Disease Control and Prevention (CDC) in 2023 indicated that more than 37 million adults in the United States were living with diabetes, while obesity rates remained considerably high across the region.

The presence of major pharmaceutical manufacturers, strong adoption of advanced therapeutic options, and extensive insurance coverage for prescription medicines further reinforced the region’s dominant position. Rising awareness of the cardiovascular and renal benefits associated with GLP-1 receptor agonists has also contributed to their expanding utilization.

Asia Pacific Expected to Record the Highest CAGR

The Asia Pacific region is projected to register the fastest CAGR during the forecast period, driven by the rapidly rising incidence of type 2 diabetes and increasing healthcare investments. According to the International Diabetes Federation (IDF) in 2021, the region recorded more than 290 million adults living with diabetes, representing the largest affected population worldwide.

Expanding healthcare systems in countries such as China and India, along with improved access to advanced therapies, are strengthening demand for effective glucose-lowering and weight-management treatments. Rising disposable incomes, growing recognition of diabetes-related risks, and government efforts to enhance chronic disease management are expected to support substantial market growth for GLP-1 receptor agonists across Asia Pacific.

Emerging Trends

- Expanded Clinical Indications: GLP-1 receptor agonists were initially approved for type 2 diabetes in 2005, and their indications have expanded over time. Approval was granted for adult obesity in 2021 for individuals with a BMI of ≥ 30 kg/m² or ≥ 27 kg/m² with comorbidities. Authorization for pediatric patients aged 12 years and older followed in 2022. In 2023, the class received approval for reducing cardiovascular risk. This sequence of regulatory actions has widened the therapeutic scope of GLP-1 therapies.

- Greater Patient Eligibility and Uptake: Updated ADA/EASD guidelines indicate that approximately 82 percent of U.S. adults with type 2 diabetes are now eligible for GLP-1 or SGLT-2 therapies, demonstrating guideline-driven expansion of demand. Among adolescents aged 12–17 years with obesity, prescription use increased from 0.1 percent in 2020 to 0.5 percent in 2023, representing a relative rise of more than 300 percent, although total usage remains below 1 percent.

- Introduction of Generics and Oral Formulations: Market accessibility has improved through the approval of the first generic liraglutide (Victoza) earlier this year and generic exenatide last month. Oral semaglutide (Rybelsus) has also been approved for glycemic control in type 2 diabetes, providing a non-injectable option that supports broader patient acceptance.

Use Cases

- Adjunctive Glycemic Control in Type 2 Diabetes: GLP-1 receptor agonists are incorporated with diet and physical activity to reduce blood glucose levels. They are approved for adults and pediatric patients aged 10 years and older. Clinical use shows HbA1c reductions often exceeding 1 percent from baseline, and these agents are recommended for patients not meeting glycemic targets with first-line therapy.

- Chronic Weight Management in Obesity: Real-world evidence from a cohort of 175 adults with overweight or obesity shows semaglutide achieving mean weight reductions of 5.9 percent at 3 months and 10.9 percent at 6 months. Comparative studies indicate semaglutide producing a 15.8 percent mean weight loss at 68 weeks versus 6.4 percent with liraglutide, emphasizing its strong and sustained impact on weight management.

- Pediatric and Adolescent Obesity Treatment: Since FDA approval in 2022, GLP-1 receptor agonists have been prescribed for individuals aged 12 years and older with obesity (BMI ≥ 95th percentile). Although overall utilization remains below 1 percent of eligible adolescents, a marked increase in adoption was observed in 2023.

- Cardiovascular Risk Reduction: With the 2023 approval for reducing major adverse cardiovascular events, GLP-1 receptor agonists are now used within comprehensive cardiovascular risk-management strategies for patients with type 2 diabetes and established cardiovascular disease.

Frequently Asked Questions on GLP-1 Receptor Agonist

- How do receptor agonists work?

Receptor agonists bind to receptors and trigger intracellular signaling pathways that modulate physiological functions. Their action enhances or replicates natural biochemical responses, allowing controlled therapeutic modulation for conditions where endogenous signaling is insufficient or impaired. - What are the major types of receptor agonists?

Receptor agonists include full agonists, partial agonists, and inverse agonists. These categories differ in the magnitude and direction of receptor activation, enabling tailored therapeutic applications depending on disease mechanisms and required biological responses. - What diseases are treated using receptor agonists?

Receptor agonists are widely used in treating chronic diseases such as diabetes, asthma, neurological disorders, hormonal deficiencies, and cardiovascular conditions. Their targeted mechanisms support precise therapeutic intervention, improving disease management and overall treatment outcomes. - What are the advantages of receptor agonist therapy?

Receptor agonist therapy offers targeted action, predictable dose responses, and potential reduction of adverse effects. Its precision enables improved efficacy, making agonists important in modern drug development strategies across therapeutic areas requiring high specificity. - What is driving growth in the receptor agonist market?

Market growth is driven by rising chronic disease prevalence, advancements in targeted therapeutics, and increased investment in drug discovery. Demand for precision medicine has propelled research activities, contributing to steady expansion across global pharmaceutical and biotechnology sectors. - Which therapeutic areas dominate the receptor agonist market?

Diabetes, oncology, respiratory diseases, and neurology remain dominant segments. High disease burden and continuous emergence of novel receptor-targeting molecules encourage robust product pipelines, contributing to sustained market penetration and commercial viability across multiple therapeutic classes. - What regions lead the receptor agonist market?

North America leads due to strong R&D capacity, presence of major pharmaceutical players, and supportive regulatory frameworks. Europe follows closely, while Asia-Pacific is experiencing rapid growth supported by expanding healthcare infrastructure and rising demand for advanced therapeutics.

Conclusion

The GLP-1 receptor agonist market is expected to maintain strong momentum as rising diabetes and obesity rates continue to drive therapeutic demand. Market expansion has been supported by robust clinical outcomes, broader indications, and increasing adoption across global healthcare systems. Advancements in formulations, regulatory approvals, and the introduction of generics are enhancing accessibility and strengthening competitiveness.

North America retains a leading position, while Asia Pacific is projected to grow rapidly due to expanding patient populations and improved healthcare investment. Overall, sustained innovation, favorable reimbursement, and rising health awareness are expected to reinforce long-term market growth.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)