Table of Contents

Overview

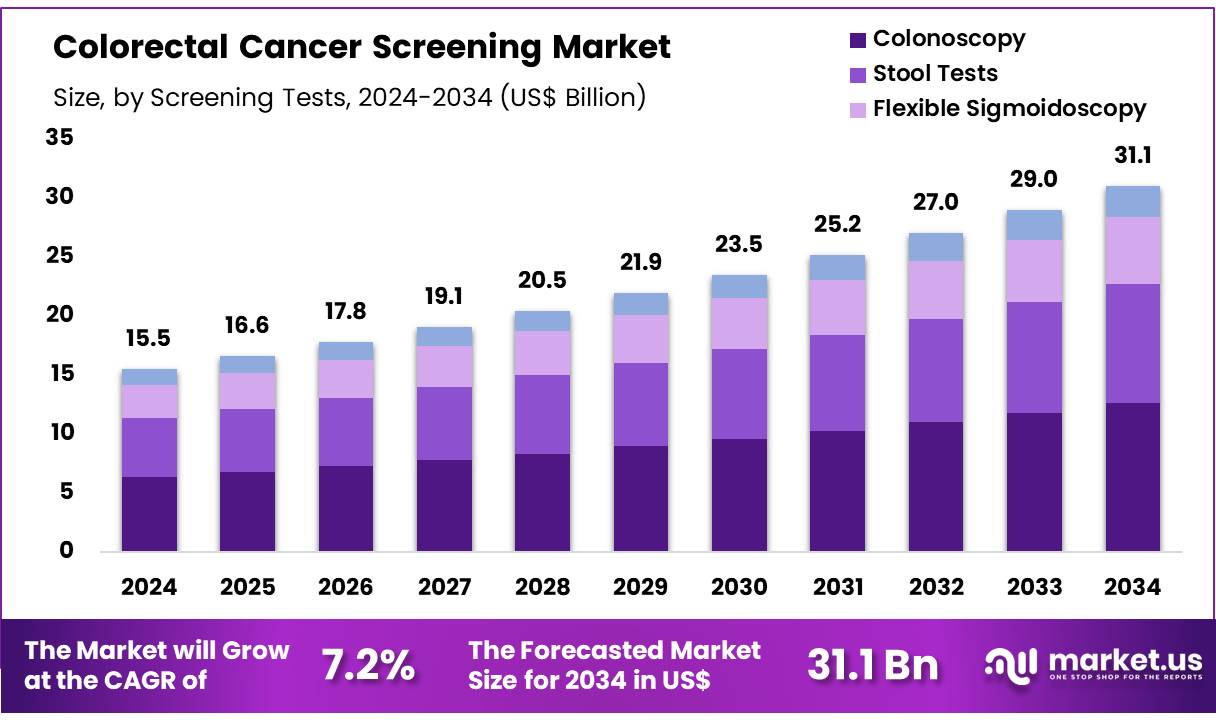

New York, NY – Nov 04, 2025 – Global Colorectal Cancer Screening Market size is expected to be worth around US$ 31.1 Billion by 2034 from US$ 15.5 Billion in 2024, growing at a CAGR of 7.2% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 40.1% share with a revenue of US$ 6.2 Billion.

A sustained emphasis on early detection has been positioned as a key driver in reducing colorectal cancer-related mortality. Colorectal cancer remains one of the most commonly diagnosed cancers worldwide, and a timely screening approach has been recognized as essential for improving patient outcomes. According to leading public health agencies, early detection may lower the risk of death by more than 60 percent, demonstrating clear clinical and economic value for healthcare systems.

Advancements in diagnostic technologies, including fecal immunochemical tests, colonoscopy, and emerging non-invasive screening methods, have expanded accessibility and accuracy. Increased adoption of preventive healthcare initiatives and rising awareness campaigns led by government and non-government organizations have also supported growing participation rates. The global trend toward value-based healthcare continues to strengthen the role of screening programs, as early-stage identification significantly reduces treatment costs and improves survival rates.

Efforts are being directed toward increasing public awareness, addressing screening hesitancy, and expanding screening availability across diverse demographic groups. The integration of digital health tools, including risk-assessment platforms and telehealth-enabled consultation services, is further enhancing patient outreach and engagement.

Colorectal cancer screening remains a critical public health priority, and the expansion of structured screening programs is anticipated to drive measurable improvements in long-term health outcomes. Continued collaboration among healthcare providers, policy bodies, and patient advocacy groups is expected to support broader participation and access, reinforcing the importance of routine screening for eligible individuals.

Key Takeaways

- The global colorectal cancer screening market generated US$ 15.5 billion in revenue in 2024 and is projected to grow at a CAGR of 7.2%, reaching approximately US$ 31.1 billion by 2033.

- Screening modalities are categorized into stool testing, colonoscopy, flexible sigmoidoscopy, and other techniques, with colonoscopy emerging as the dominant segment in 2024, accounting for 40.7% market share.

- In terms of end users, hospitals, specialty clinics, and other healthcare facilities represent key segments, with hospitals capturing a notable share of 55.2% in 2024.

- North America accounted for the leading regional position in the colorectal cancer screening market, representing 40.1% of the overall share in 2024.

Regional Analysis

North America has been observed as the leading region in the colorectal cancer screening market, accounting for 40.1% of total revenue. This dominance can be attributed to a rising burden of colorectal cancer, strong awareness programs emphasizing early detection, and rapid technological advancements in screening solutions.

The American Cancer Society reported that an estimated 153,020 individuals in the United States were diagnosed with colorectal cancer, while approximately 52,550 deaths were recorded. These figures reinforce the critical importance of consistent screening to detect malignancy at an early, more treatable stage. Increased adoption of preventive healthcare practices and the availability of innovative, non-invasive screening tools, including at-home fecal immunochemical tests and emerging blood-based diagnostics, have significantly improved access to screening.

In addition, updated clinical recommendations encouraging screening for adults aged 45 and above have further supported regional market expansion. With rising recognition of the clinical and economic benefits of early diagnosis, the regional market is projected to grow steadily.

Asia Pacific is expected to record the fastest growth during the forecast period. This momentum can be linked to a substantial rise in colorectal cancer incidence, expanding screening infrastructure, and increasing emphasis on preventive healthcare. Research published by the National Center for Biotechnology Information in 2023 indicated an incidence rate of approximately 26.7 cases per 100,000 men and 22.7 cases per 100,000 women in Japan within the 40–44 age group, demonstrating the growing prevalence of the disease.

Government efforts to strengthen screening programs, rising awareness of risk factors, and growing adoption of cost-effective, non-invasive diagnostic techniques are anticipated to propel market growth. Advancements in healthcare infrastructure and increased availability of modern diagnostic systems are further expected to support market expansion, positioning Asia Pacific as a high-growth region in the colorectal cancer screening market.

Emerging Trends

Expansion of Mailed Stool-Based Testing

Mailed stool-based screening programs have been expanding, supported by improved participation rates within federally qualified health centers. Home-delivered kits require minimal patient effort and are accompanied by reminder systems, which help increase screening compliance and reduce late-stage diagnoses.

Cost-effectiveness assessments and publicly funded initiatives have encouraged adoption, particularly in underserved populations. This model lowers access barriers related to transportation and clinic visits, and wider program implementation is anticipated due to simplified logistics and favorable public health strategies.

Increasing Use of Stool DNA Tests

Stool DNA testing continues to gain traction as a preferred home-based screening method, accounting for 11.1 percent of adult usage in 2023. These tests detect tumor-related DNA markers and offer higher sensitivity than traditional fecal occult blood tests.

Samples are returned to laboratories without requiring clinical appointments, and positive results lead to colonoscopy follow-up. User-friendly instructions and strong patient acceptance support adoption, while integration into screening guidelines reflects growing demand for accurate and non-invasive diagnostic options.

Gradual Rise in CT Colonography Adoption

CT colonography has demonstrated modest growth, representing 2.5 percent of screening tests in 2023. This non-sedated, low-dose CT-based “virtual colonoscopy” provides three-dimensional visualization of the colon with rapid post-procedure recovery.

Although bowel preparation remains necessary and follow-up colonoscopy is required for abnormal findings, the technique appeals to individuals seeking alternatives to invasive procedures. Expanded insurance coverage and ongoing evaluations of accuracy and patient satisfaction are contributing to incremental adoption.

Increased Screening Focus Among Younger Adults

Colorectal cancer incidence has been rising among younger adults, with cases among individuals aged 15–39 increasing by 3.8 percent annually. These trends have influenced screening recommendations, lowering the initiation age to 45.

Efforts now emphasize early detection among younger populations with risk factors or family history. Public health programs and clinical outreach have strengthened awareness and screening uptake among adults in their 40s, while continued surveillance supports ongoing policy refinements to address early-onset colorectal cancer.

Frequently Asked Questions on Colorectal Cancer Screening

- Who should undergo colorectal cancer screening?

Screening is recommended for individuals aged 45 years and older, even without symptoms. People with family history, inflammatory bowel disease, or genetic predispositions may require earlier or more frequent screenings, based on physician guidance and established clinical recommendations. - What types of colorectal cancer screening tests are available?

Available screening tests include colonoscopy, fecal immunochemical test (FIT), stool DNA testing, and flexible sigmoidoscopy. Colonoscopy remains the most comprehensive option, while non-invasive stool-based tests are increasingly used due to convenience and accessibility. - Why is early detection of colorectal cancer important?

Early detection significantly increases chances of successful treatment and survival. Identifying cancer or precancerous polyps before symptoms develop allows timely intervention, reduces treatment complexity, and lowers healthcare burden by preventing late-stage disease. - How often should colorectal cancer screening be conducted?

The screening frequency depends on the selected method. Colonoscopy is generally recommended every ten years, while stool-based tests may be conducted annually or biennially. Patients with high-risk factors may require more frequent evaluations. - What is the colorectal cancer screening market?

The colorectal cancer screening market involves products and services designed to detect colorectal cancer early, including diagnostic instruments, screening kits, software solutions, and service providers. Market growth is driven by rising disease incidence and preventive healthcare adoption. - Which screening method dominates the market?

Colonoscopy currently holds the largest market share due to its high diagnostic accuracy and ability to detect and remove polyps in a single procedure. Increasing adoption of stool-based and blood-based screening tools complements demand growth across diverse populations. - Which regions lead the colorectal cancer screening market?

North America leads the market due to advanced healthcare infrastructure, high awareness, and strong reimbursement frameworks. Asia Pacific is projected to register the fastest growth, supported by rising cancer incidence and expanding diagnostic capabilities. - What trends are shaping the market?

Key trends include increasing use of non-invasive at-home tests, adoption of blood-based biomarker screening, integration of artificial intelligence in diagnostics, and expansion of screening programs to younger populations based on updated clinical guidelines and risk profiles.

Conclusion

The colorectal cancer screening landscape is advancing steadily, supported by technological innovation, expanding public health initiatives, and heightened awareness of the importance of early detection. Strong market growth has been driven by increasing adoption of non-invasive screening tools, enhanced access through mailed testing programs, and updated screening guidelines targeting younger populations.

Regional dynamics highlight North America’s leadership and Asia Pacific’s rapid expansion, reflecting improving healthcare infrastructure and preventive care focus. Continued emphasis on early intervention, patient-centric screening options, and policy collaboration is expected to strengthen participation rates and improve long-term outcomes, reinforcing screening as a critical component of global cancer prevention strategies.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)