Table of Contents

Overview

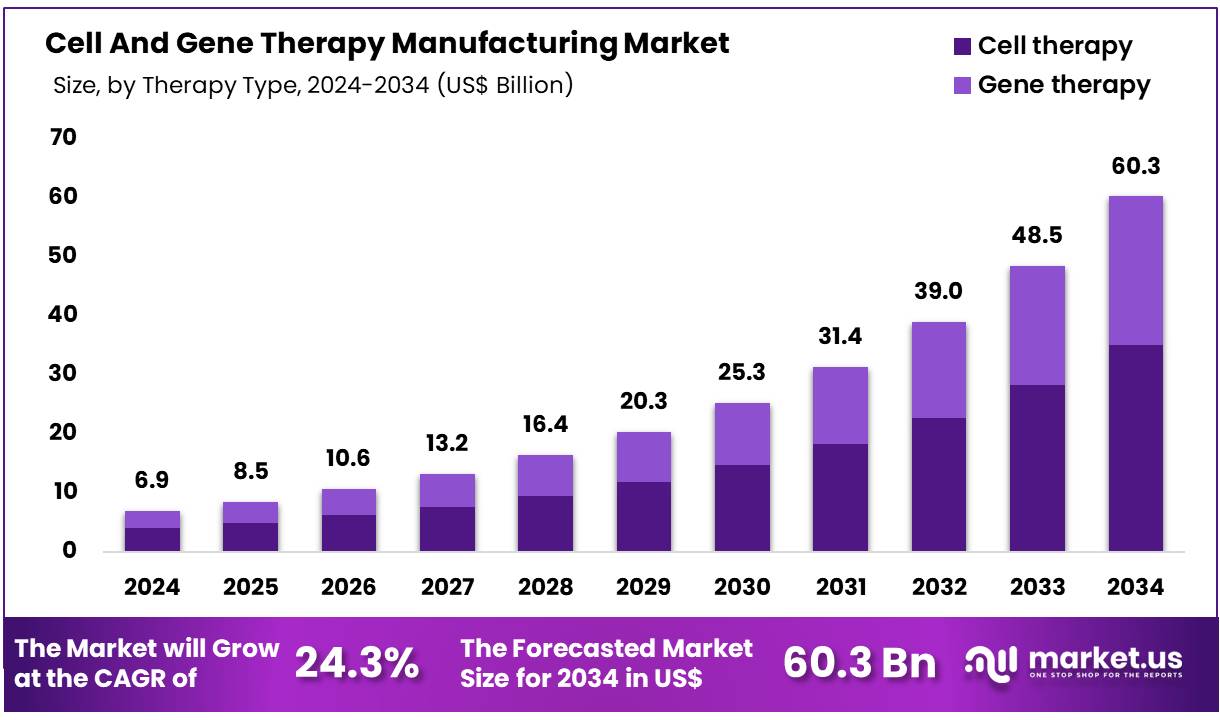

New York, NY – Nov 21, 2025 – Global Cell And Gene Therapy Manufacturing Market size is expected to be worth around US$ 60.3 Billion by 2034 from US$ 6.9 Billion in 2024, growing at a CAGR of 24.3% during the forecast period from 2025 to 2034. In 2024, North America led the market, achieving over 48.1% share with a revenue of US$ 3.29 Billion.

The cell and gene therapy manufacturing landscape has been experiencing significant expansion as demand for advanced therapeutic modalities continues to rise. Strong growth has been observed as companies accelerate investments in next-generation platforms, optimized production workflows, and scalable bioprocessing solutions. The market has been driven by an increasing number of approved therapies, a robust clinical pipeline, and continuous advancements in viral vector technologies.

Manufacturing processes for cell and gene therapies have been characterized by high complexity, owing to stringent quality standards, specialized raw materials, and sensitive production environments. The adoption of automated systems, closed processing, and high-efficiency bioreactors has been increasing, as these technologies enable improved consistency and reduce contamination risks. Capacity expansion initiatives have been undertaken globally as manufacturers respond to rising clinical and commercial volumes.

Strategic collaborations between biotechnology firms, contract development and manufacturing organizations, and research institutions have supported faster development cycles and enhanced technological capabilities. Regulatory frameworks have become more defined, allowing clearer pathways for scale-up and commercialization. The growth of the market can be attributed to rising prevalence of chronic and genetic disorders, increasing investment in personalized medicine, and active government support for advanced therapeutic development.

The sector is expected to maintain strong momentum, supported by continuous innovation and the shift toward more efficient and cost-effective manufacturing platforms. The overall outlook remains positive as cell and gene therapies progress toward broader clinical adoption and global market expansion.

Key Takeaways

- Market Size: Global Cell And Gene Therapy Manufacturing Market size is expected to be worth around US$ 60.3 Billion by 2034 from US$ 6.9 Billion in 2024.

- Market Growth: The Market growing at a CAGR of 24.3% during the forecast period from 2025 to 2034.

- Therapy Type Analysis: Cell therapies hold a dominant position, accounting for 58.2% of the total market share.

- Mode Analysis: Contract manufacturing currently holds the largest share, capturing 67.5% of the market.

- Scale Analysis: Preclinical and clinical-scale manufacturing currently dominates, capturing 74.1% of the market share.

- Application Analysis: oncology applications hold the largest market share, dominating at 48.9%.

- End-Use Analysis: pharmaceutical and biotechnology companies hold the dominant share at 69.2%.

- Regional Analysis: In 2024, North America is projected to dominate the Cell and Gene Therapy Manufacturing Market, accounting for 48.1% of the global market share.

Regional Analysis

In 2024, North America is projected to hold a predominant position in the Cell and Gene Therapy Manufacturing Market, representing 48.1% of global revenue. This leadership is supported by the region’s advanced healthcare infrastructure, substantial biotechnology investments, and an extensive pipeline of cell and gene therapy candidates undergoing development.

The presence of leading pharmaceutical and biotechnology organizations has strengthened manufacturing capacity, while supportive regulatory frameworks have enabled faster approval timelines and more efficient commercialization pathways. The rising incidence of chronic and genetic disorders has increased the demand for novel therapeutic solutions, contributing to sustained market expansion across the region.

Active collaborations between academic research centers and industry participants have facilitated continuous innovation and accelerated research and development activities. Ongoing technological progress, combined with a strong emphasis on personalized and precision medicine, has further enhanced the region’s competitive advantage. Based on these factors, North America is expected to maintain its dominant role in the cell and gene therapy manufacturing landscape over the forecast period.

Emerging Trends

- Adoption of advanced manufacturing technologies: Continuous and automated systems are being integrated to enhance production quality and accelerate manufacturing timelines. These technologies minimize manual intervention and support rapid scale-up, reducing the risk of shortages for high-demand therapies.

- Standardization of CMC processes: Chemistry, Manufacturing, and Control requirements are being strengthened through updated regulatory guidance and structured forums. The strategic focus on clearer standards is expected to streamline licensure pathways under the 21st Century Cures Act.

- Enhanced product characterization methods: Innovative analytical assays are being developed to improve predictions of safety, potency, and overall therapeutic performance. These tools provide regulators with more precise data for evaluating quality before candidate therapies enter clinical settings.

- Modular, scalable manufacturing facilities: Flexible and facility-dedicated manufacturing spaces are being introduced to meet evolving production needs. An example includes the establishment of an 8,000 ft² modular site equipped with four clean rooms designed to support diverse clinical-trial demands.

Use Cases

- Dedicated clinical-trial production: A newly funded Modular Terrace Facility, supported by a USD 20 million investment, provides specialized manufacturing for first-in-human studies. The center includes 3,000 ft² of clean-room space and typically requires several months for a single patient production cycle.

- Viral vector manufacture for gene transfer: The NCI’s Biopharmaceutical Development Program has expanded capabilities to produce lentiviral and retroviral vectors. Standard project timelines range from 9 to 13 months, covering production, testing, and final product release for clinical applications.

- Regulatory readiness for Biologics License Applications: The FDA has initiated dedicated town halls addressing CMC preparedness for gene therapy BLAs. These sessions build on previous forums for investigational products and reflect an increasing emphasis on pathway clarity for advanced therapy approvals.

Frequently Asked Questions on Cell And Gene Therapy Manufacturing

- Why is cell and gene therapy manufacturing complex?

The complexity arises from strict quality standards, sensitive biological materials, and individualized production processes. Highly specialized equipment, skilled personnel, and controlled conditions are required to maintain consistency while preventing contamination during the development of personalized or batch-based therapies. - What technologies are commonly used in this manufacturing process?

Production relies on automated systems, closed bioprocessing platforms, viral vector production units, and high-efficiency bioreactors. These technologies support improved scalability, reduced contamination risk, and enhanced reproducibility across both clinical and commercial manufacturing operations. - What are viral vectors, and why are they important?

Viral vectors are engineered viruses used to deliver therapeutic genes into patient cells. Their critical role in gene therapy manufacturing is based on their ability to transport genetic material safely and efficiently while maintaining high transduction performance. - How do regulatory requirements influence manufacturing?

Regulatory agencies enforce strict guidelines covering safety, quality, and production consistency. These requirements ensure reliable therapeutic outcomes while guiding manufacturers in designing validated processes that meet global clinical and commercial standards for advanced therapies. - Which region currently leads the global market?

North America holds the dominant market position due to strong healthcare infrastructure, significant R&D investments, and a robust pipeline of therapeutic candidates. The presence of major biotechnology firms further strengthens manufacturing capacity across the region. - What role do CDMOs play in this market?

Contract development and manufacturing organizations provide essential support through specialized production services, scalable facilities, and regulatory expertise. Their involvement enables faster development cycles and reduces the capital burden on biotechnology and pharmaceutical companies. - How is automation influencing the market?

Automation enhances process consistency, reduces manual errors, and supports scalable production. Increasing adoption of automated bioprocessing systems is driving efficiency gains across clinical and commercial manufacturing, contributing to overall market competitiveness.

Conclusion

The cell and gene therapy manufacturing market is positioned for sustained expansion as technological innovation, rising clinical demand, and supportive regulatory pathways continue to advance the sector. Strong growth is being driven by increasing therapy approvals, expanding manufacturing capacity, and deeper collaboration among industry stakeholders.

North America’s leadership reflects the region’s mature infrastructure and robust R&D ecosystem, while global investments highlight growing confidence in advanced therapeutic modalities. The emergence of automated systems, scalable facilities, and standardized CMC frameworks is expected to further enhance efficiency and reliability. Overall, the market outlook remains highly positive, underpinned by strong momentum and broad clinical adoption.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)