Table of Contents

Overview

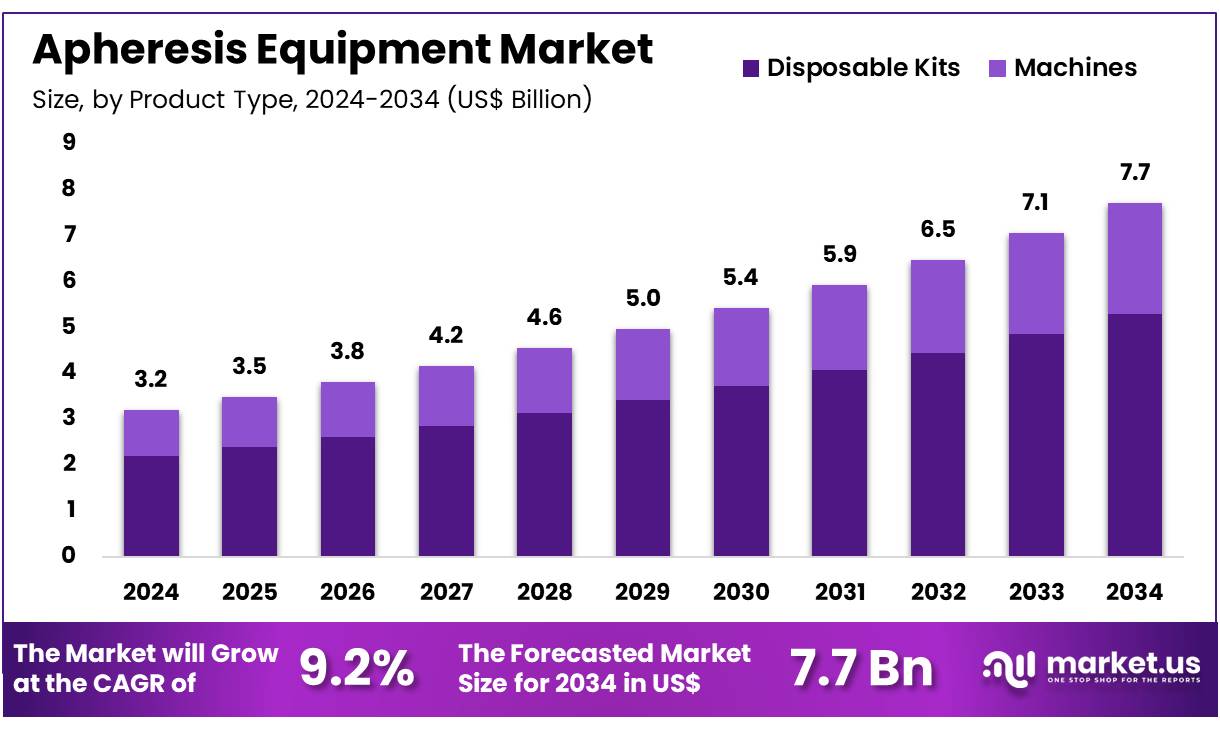

New York, NY – Nov 18, 2025 – Global Apheresis Equipment Market size is expected to be worth around US$ 7.7 Billion by 2034 from US$ 3.2 Billion in 2024, growing at a CAGR of 9.2% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 38.7% share with a revenue of US$ 1.2 Billion.

The global apheresis equipment market has been witnessing steady expansion, driven by the rising prevalence of chronic diseases and the increasing adoption of advanced blood component separation technologies. Growth has been supported by a broader shift toward personalized therapies, in which apheresis procedures have become integral to the management of oncology, autoimmune disorders, and hematological conditions. Demand has also been reinforced by the growing emphasis on plasma-derived medicinal products, resulting in increased utilization of both automated systems and disposable apheresis kits.

The market has been characterized by continuous technological improvements. Enhanced device automation, improved collection efficiency, and reduced procedure times have contributed to the wider acceptance of apheresis systems in hospitals, transfusion centers, and specialized clinics. The expansion of therapeutic apheresis, including leukapheresis, plasmapheresis, and plateletpheresis, has further strengthened equipment adoption across major healthcare markets.

The rise in voluntary blood donation programs and government-supported initiatives for ensuring blood safety have contributed to accelerated procurement of advanced apheresis devices. Growing investment in healthcare infrastructure across emerging economies has also supported equipment penetration. Strategic collaborations and product innovations by key manufacturers have been observed, aiming to improve device performance and expand clinical applications.

Overall, the growth of the apheresis equipment market is expected to remain positive, as the demand for high-quality blood components and therapeutic apheresis procedures continues to increase. Continued product development, rising awareness, and expanding clinical utility are anticipated to sustain the market’s upward trajectory in the coming years.

Key Takeaways

- The Apheresis Equipment market generated US$ 3.2 billion in revenue in 2024, registered a 9.2% CAGR, and is projected to reach US$ 7.7 billion by 2033.

- By product type, the market is categorized into disposable kits and machines, with disposable kits dominating in 2024 with a 68.7% share.

- Based on technology, the market is segmented into centrifugation and membrane filtration, where membrane filtration accounted for a 75.4% share.

- In terms of application, the market is classified into neurological disorders, renal disorders, hematological disorders, and others, with neurological disorders leading at 56.5%.

- The procedure segment includes plasmapheresis, photopheresis, LDL apheresis, leukapheresis, and others, and plasmapheresis held the highest share of 66.3%.

- By end user, the market is divided into hospitals & clinics, blood donation centers, ambulatory surgical centers, and others, with hospitals & clinics representing 72.1%.

- Regionally, North America dominated the market in 2024 with a 38.7% share.

Segmentation Analysis

- Product Type Analysis: In 2023, disposable kits accounted for 68.7% of the product segment, driven by rising demand for single-use and cost-efficient medical consumables that lower infection risk. Their use removes the need for complex sterilization, providing higher safety and operational convenience. Growing adoption of apheresis procedures across hospitals and outpatient facilities, supported by continuous product innovations, is expected to sustain the dominance of disposable kits over the forecast period.

- Technology Analysis: Membrane filtration held a 75.4% share of the technology segment in 2023 due to its precision, capacity for high-volume processing, and superior component recovery capabilities. This technology remains essential in the management of renal and neurological conditions, where efficient therapeutic procedures are required. Increasing preference among healthcare providers for reliable and clinically effective systems is expected to reinforce membrane filtration’s leading position in future apheresis equipment developments.

- Application Analysis: Neurological disorders represented 56.5% of the application segment in 2023, supported by extensive use of apheresis treatments such as plasmapheresis for conditions including multiple sclerosis and Guillain-Barré syndrome. The growing prevalence of autoimmune neurological diseases, combined with expanding clinical validation for apheresis therapies, continues to drive this segment. As new therapeutic approaches emerge for complex neurological conditions, demand for apheresis equipment is projected to rise steadily.

- Procedure Analysis: Plasmapheresis captured 66.3% of procedure-related revenue in 2023, reflecting its proven ability to eliminate pathogenic antibodies in autoimmune, hematological, and neurological disorders. Increased awareness of its therapeutic value and ongoing enhancements in filtration technologies continue to strengthen uptake. As treatment strategies shift toward more targeted interventions, plasmapheresis is expected to retain its central role, thereby supporting consistent demand in the apheresis equipment market.

- End-user Analysis: Hospitals and clinics accounted for 72.1% of end-user share in 2023, remaining the primary locations for apheresis procedures due to their advanced infrastructure and diverse patient populations. The rising prevalence of chronic conditions such as renal and hematologic disorders has increased the need for specialized therapeutic interventions in these settings. As institutions prioritize improved clinical outcomes and operational efficiency, demand for advanced apheresis equipment in hospitals and clinics is expected to remain strong.

Regional Analysis

North America Leading the Apheresis Equipment Market

North America accounted for the largest revenue share of 38.7%, supported by a combination of structural and demographic factors. The rising burden of chronic and autoimmune diseases increased the demand for therapeutic apheresis procedures across healthcare facilities. Continuous technological advancements in apheresis systems improved operational efficiency and clinical outcomes, which encouraged broader adoption among hospitals and specialized treatment centers.

The expanding geriatric population, which is more prone to conditions requiring apheresis-based interventions, further contributed to market growth. Supportive government measures, including initiatives from the Centers for Medicare & Medicaid Services (CMS) to strengthen access to advanced medical technologies, reinforced equipment utilization across the region. Leading industry participants such as Terumo BCT Inc., Fresenius SE & Co. KGaA, and Haemonetics Corporation strengthened regional growth through ongoing product innovation and strategic expansion activities. These combined drivers supported the strong performance of the North American apheresis equipment market in 2024.

Asia Pacific Expected to Record the Fastest Growth

The Asia Pacific region is projected to register the highest CAGR during the forecast period, driven by the increasing incidence of hematological disorders and the rising demand for high-quality blood components. Ongoing technological advancements in apheresis systems are anticipated to enhance procedure efficiency and expand treatment accessibility.

Government-led healthcare improvements, including initiatives by the Indian government to advance medical infrastructure and promote modern therapeutic technologies, are expected to accelerate adoption rates. Key global manufacturers such as Terumo BCT Inc., Fresenius SE & Co. KGaA, and Haemonetics Corporation continue to expand their presence in the region by offering innovative solutions tailored to local clinical needs. These developments are expected to support strong and sustained market growth across Asia Pacific during the forecast period.

Frequently Asked Questions on Apheresis Equipment

- What is apheresis equipment?

Apheresis equipment is used to separate specific blood components such as plasma, platelets, or leukocytes. The process enables targeted extraction while returning remaining components to the donor, supporting therapeutic procedures and specialized blood collection. - How does apheresis equipment work?

Apheresis equipment operates by circulating blood through a centrifugation or filtration system where individual components are isolated. Selected components are retained for treatment, while unneeded elements are reinfused safely back into the patient or donor. - What are the main types of apheresis devices?

The main types include plasma separators, platelet separators, leukocyte separators, and multifunctional therapeutic apheresis systems. These devices support both donor collection activities and clinical treatments for various hematological or autoimmune disorders. - What clinical conditions require apheresis procedures?

Apheresis procedures are employed in the management of conditions such as autoimmune diseases, neurological disorders, hematologic malignancies, and metabolic abnormalities. The technology facilitates rapid removal of harmful components from the bloodstream in critical care. - How safe is apheresis equipment for patients and donors?

Apheresis equipment adheres to strict regulatory standards and incorporates advanced monitoring systems to ensure safety. Modern devices maintain controlled flow rates, sterile pathways, and real-time oversight to minimize procedural risk for both patients and donors. - What technological advancements are shaping apheresis equipment?

Recent advancements include automation, improved membrane filters, enhanced centrifugal precision, and integrated digital monitoring. These innovations have strengthened procedural efficiency, reduced operator dependence, and enabled more accurate targeting of specific blood components. - Which regions dominate the apheresis equipment market?

North America and Europe currently dominate the market due to advanced healthcare systems, high awareness, and established reimbursement frameworks. Rapid growth is observed in Asia-Pacific, supported by rising healthcare investment and increased diagnosis rates. - Who are the key players in the apheresis equipment market?

The market consists of established manufacturers offering advanced separation technologies. Key companies typically provide therapeutic apheresis systems, donor apheresis platforms, and integrated disposables that support operational reliability across blood banks and clinical facilities.

Conclusion

The global apheresis equipment market is expected to maintain a positive growth trajectory, supported by rising chronic disease prevalence, expanding therapeutic applications, and continuous technological upgrades. Strong demand for disposable kits, membrane filtration systems, and plasmapheresis procedures has reinforced market expansion across key end-use settings.

Significant adoption in hospitals and clinics, coupled with supportive government initiatives and increased investment in healthcare infrastructure, continues to strengthen market penetration. North America remains the leading region, while Asia Pacific is projected to record the fastest growth. Overall, sustained innovation and rising clinical utilization are anticipated to drive long-term market advancement.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)