Overview

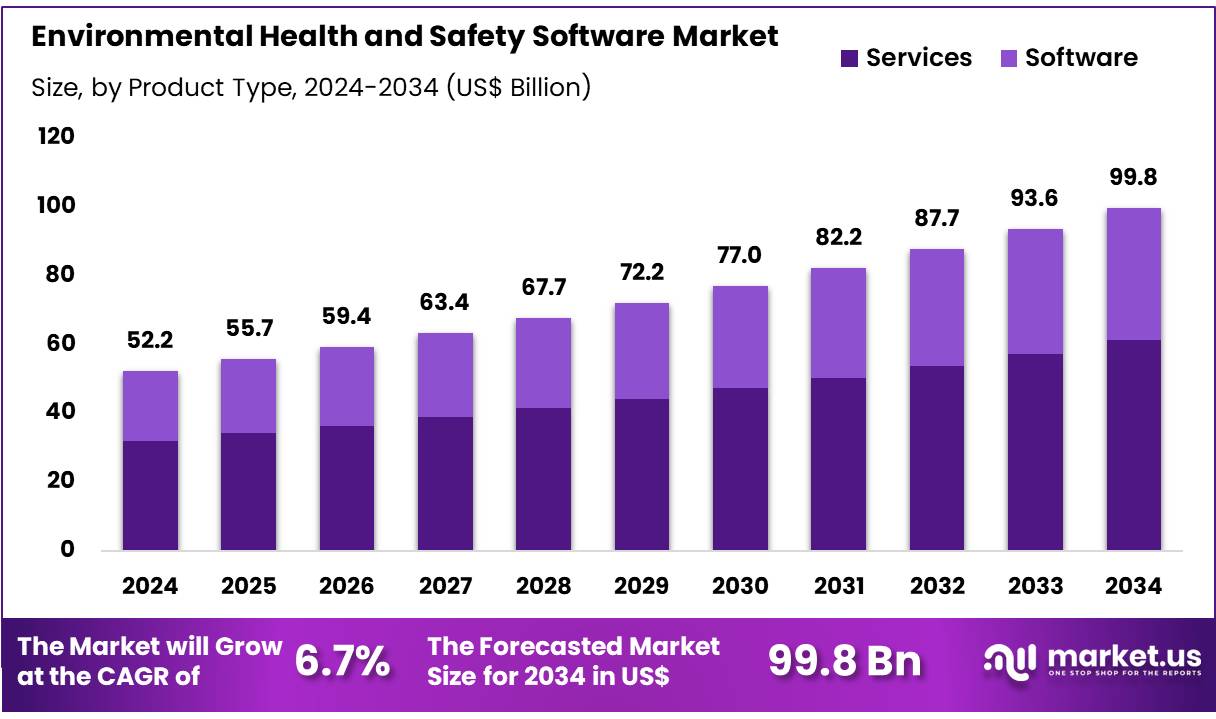

New York, NY – Nov 19, 2025 – Global Environmental Health and Safety Software Market size is expected to be worth around US$ 99.8 Billion by 2034 from US$ 52.2 Billion in 2024, growing at a CAGR of 6.7% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 38.6% share with a revenue of US$ 20.1 Billion.

The launch of the Environmental Health and Safety (EHS) software is being announced as a strategic advancement designed to strengthen organizational compliance, risk control, and workplace sustainability. The introduction of this platform has been positioned as a response to increasing regulatory demands and the rising emphasis on environmental stewardship across industries.

The software has been developed to support real-time monitoring of safety processes, incident reporting, environmental performance tracking, and regulatory documentation. Its adoption is expected to streamline compliance management, as automated workflows reduce manual errors and enhance the accuracy of reporting activities. Integration capabilities allow the platform to connect with existing enterprise systems, ensuring a unified view of safety and environmental metrics.

The demand for digital EHS solutions has been increasing, as organizations seek systems that minimize operational risks and ensure adherence to global safety standards. The growth of this market has been attributed to stricter environmental regulations, heightened awareness of workplace hazards, and the need for data-driven decision-making. The platform’s analytics module supports predictive insights, enabling the identification of potential risks before they escalate.

The introduction of this EHS software reflects a commitment to improving operational transparency and enhancing worker protection. Its deployment is expected to support enterprises in meeting compliance obligations while promoting sustainable business practices. The platform establishes a foundation for safer workplaces and improved environmental responsibility, reinforcing the importance of digital innovation in modern risk management.

Key Takeaways

- In 2024, the environmental health and safety software market generated revenue of US$ 52.2 billion, supported by a CAGR of 6.7%, and is projected to reach US$ 99.8 billion by 2033.

- The product type segment is categorized into software and services, with services leading the market in 2024 by accounting for 61.3% of the total share.

- Based on deployment mode, the market is segmented into cloud and on-premises, where the cloud segment held a significant share of 67.5%.

- The end-user segment includes chemical & petrochemical, telecom & IT, healthcare, general manufacturing, energy & mining, construction, and others, with the chemical & petrochemical sector dominating by securing 27.3% of overall revenue.

- North America remained the leading regional market in 2024, recording a 38.6% share.

Regional Analysis

North America accounted for the largest share of 38.6% in the environmental health and safety software market. This dominance has been supported by stringent regulatory frameworks, a stronger emphasis on sustainability, and the rising need for streamlined compliance management. Data from the US Environmental Protection Agency (EPA) indicated that environmental violations increased by 18% in 2023 compared to 2022, prompting wider adoption of advanced EHS platforms to minimize operational risks.

The Occupational Safety and Health Administration (OSHA) reported a 22% rise in workplace safety inspections in 2024, reinforcing the demand for systems designed to support adherence to safety regulations. Additionally, the US Department of Labor recorded a 15% annual increase in funding for workplace safety initiatives in 2023, which encouraged companies to deploy digital solutions for incident tracking and hazard assessment.

Key industry participants such as Intelex and Cority recorded a 25% expansion in their customer base in 2024, reflecting growing market penetration. The incorporation of artificial intelligence and IoT technologies has strengthened the capabilities of EHS platforms by enabling real-time monitoring and predictive analytics. These developments, combined with heightened corporate responsibility efforts, have supported strong market growth in the region.

Asia Pacific Expected to Record the Highest CAGR

The Asia Pacific region is projected to register the fastest growth, supported by accelerated industrial development, tighter regulatory oversight, and growing awareness of workplace safety. The Chinese Ministry of Ecology and Environment reported a 30% rise in environmental compliance audits in 2023, driving companies toward digital environmental management tools.

India’s Ministry of Labour and Employment noted a 20% increase in workplace safety inspections in 2024, underscoring the need for structured safety management systems. In Japan, a 15% increase in funding for occupational health initiatives in 2023 was announced by the Ministry of Health, Labour, and Welfare, encouraging the deployment of advanced EHS technologies.

ASEAN reported a 25% rise in cross-border environmental regulations in 2024, further influencing the adoption of compliance-focused software solutions. Companies such as Enablon and Sphera reported a 30% increase in their customer base across the region in 2024. These trends, combined with higher investments in smart manufacturing and sustainability initiatives, are expected to accelerate market expansion in the Asia Pacific region.

Emerging Trends

- Cloud-Based Compliance Platforms: The shift toward cloud-hosted EHS solutions has been strengthened by regulatory requirements for electronic submissions. OSHA’s 2024 mandate specifies annual electronic filing of Forms 300, 300A, and 301 through the Injury Tracking Application, encouraging adoption of automated cloud systems that streamline compliance workflows.

- IoT-Enabled Real-Time Monitoring: Integration of IoT sensors with EHS platforms is enabling continuous measurement of air, water, and soil indicators. The EPA’s Air Trends program now compiles National Emissions Inventory and Air Quality System data into digital dashboards, demonstrating expanding access to real-time environmental information for regulators and industry users.

- AI-Driven Predictive Analytics: The demand for predictive insights continues to increase as organizations seek to prevent incidents. In 2024, the NIOSH Science Blog recorded nearly 787,000 views, reflecting strong interest in data-driven safety topics and reinforcing the need for analytic tools that support proactive risk identification.

Use Cases

- Automated Injury and Illness Reporting: During reporting year 2024, approximately 1.5 million workplace injury and illness records were filed electronically through OSHA’s Injury Tracking Application. EHS software automates preparation of Form 300A summaries and Form 301 details, reducing manual input and enhancing accuracy for high-volume submissions.

- Regulatory Compliance and Penalty Avoidance: With OSHA civil penalties rising by 3.2 percent in 2024 reaching $16,131 for serious violations and $161,323 for willful or repeated violations organizations are adopting EHS platforms to track corrective actions and produce audit-ready documentation, reducing exposure to costly regulatory penalties.

- Community-Centered Technical Assistance: To strengthen environmental justice initiatives, the EPA allocated $91 million in FY 2024 to develop community technical assistance hubs. These hubs rely on digital EHS tools to train local partners in data collection, compliance management, and reporting, illustrating cross-agency use of software for community-driven outcomes.

Frequently Asked Questions on Environmental Health and Safety Software

- What are the key features of EHS software?

Key features include incident tracking, compliance management, audit workflows, risk assessments, environmental data monitoring, and training modules. These functions streamline operational reporting, support regulatory alignment, and facilitate structured safety and sustainability management. - How does EHS software improve compliance?

Compliance is improved through automated alerts, standardized documentation, real-time data capture, and regulatory tracking. These capabilities reduce manual errors, strengthen oversight, and ensure timely adherence to environmental and workplace safety requirements. - What industries commonly use EHS software?

The software is widely used in manufacturing, energy, chemicals, construction, pharmaceuticals, and transportation sectors. High regulatory exposure and complex safety requirements drive adoption across these industries to ensure systematic risk and compliance management. - What benefits does EHS software provide to organizations?

Benefits include enhanced compliance performance, reduced incident rates, improved data accuracy, and strengthened sustainability reporting. These advantages support operational efficiency while reducing the costs associated with regulatory violations and safety-related disruptions. - Which regions hold the largest market share for EHS software?

North America holds a significant share due to stringent regulations and advanced digital adoption. Europe follows closely, while the Asia-Pacific region is experiencing rapid growth driven by industrial expansion and evolving compliance mandates. - How is technology influencing the EHS software market?

Technologies such as AI, IoT, predictive analytics, and mobile platforms are shaping product innovation. These advancements improve real-time monitoring, automate risk assessments, and enhance decision-making across environmental and safety operations. - How is demand from emerging economies impacting the market?

Demand from emerging economies is rising as regulatory enforcement strengthens, industrial activity expands, and digital transformation initiatives grow. These factors are creating new opportunities for global EHS software providers.

Conclusion

The environmental health and safety software market is advancing as organizations prioritize compliance, risk mitigation, and sustainability. Growth has been supported by rising regulatory scrutiny, increased workplace safety inspections, and expanding adoption of digital tools. The integration of cloud platforms, IoT systems, and predictive analytics has strengthened real-time monitoring and improved decision-making.

Strong demand from North America and rapid expansion in Asia Pacific indicate broad global momentum. The market’s progression demonstrates a sustained shift toward data-driven environmental management, structured safety processes, and enhanced operational transparency, positioning EHS software as a critical component of modern compliance and sustainability frameworks.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)