Table of Contents

Overview

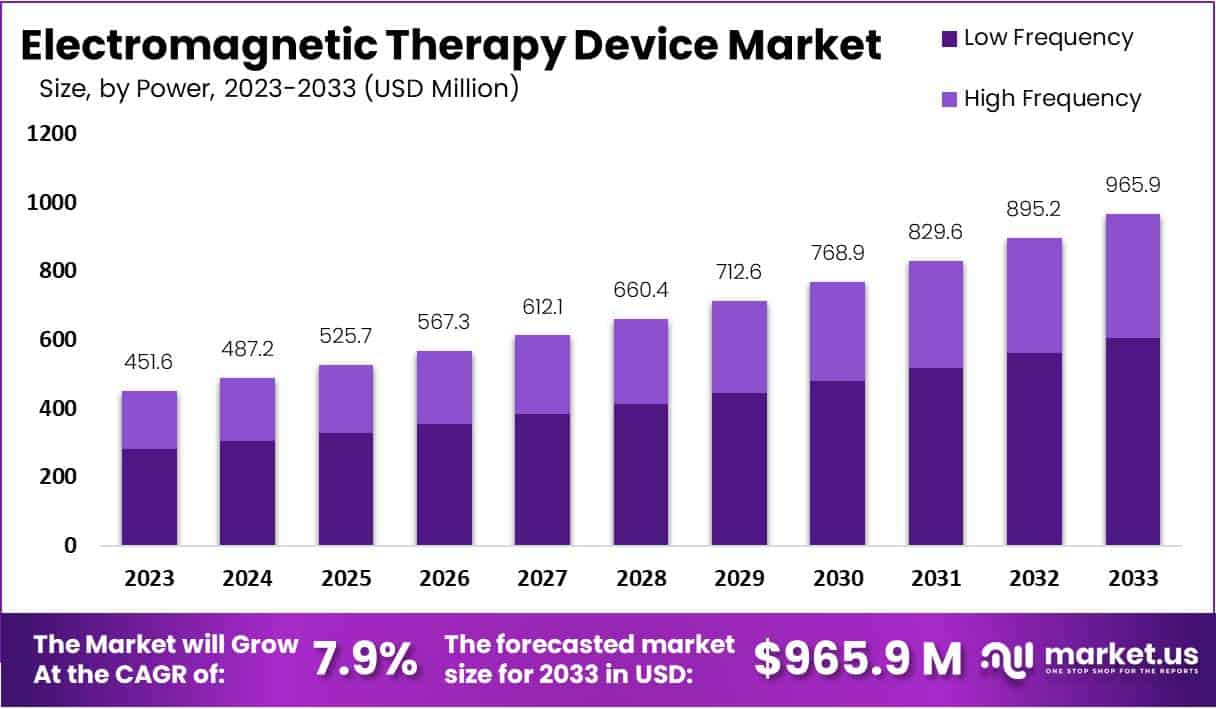

The Global Electromagnetic Therapy Device Market is projected to reach USD 965.9 million by 2033, increasing from USD 451.6 million in 2023 at a CAGR of 7.9% from 2024 to 2033. This growth is driven by the rising demand for non-invasive and drug-free pain management solutions. Increasing awareness about electromagnetic therapy’s therapeutic benefits and its expanding applications across clinical, homecare, and wellness sectors are fueling adoption. The technology is gaining popularity due to its proven ability to reduce inflammation, improve circulation, and accelerate recovery from chronic pain and musculoskeletal conditions.

Technological advancements have played a vital role in market expansion. The introduction of modern pulsed electromagnetic field (PEMF) systems, smart energy delivery technologies, and user-friendly interfaces has improved therapy outcomes and patient compliance. The development of portable and wearable devices has further broadened their use in homecare and sports medicine. These innovations are making electromagnetic therapy more accessible, efficient, and affordable. Manufacturers are focusing on integrating personalized settings and digital monitoring, which enhance precision and patient satisfaction while driving demand in both developed and emerging markets.

The growing incidence of chronic pain and musculoskeletal disorders continues to be a key driver. Conditions such as arthritis, post-surgical pain, and degenerative bone diseases are increasing among aging populations. Older adults are seeking safe and continuous treatment options that minimize medication dependency. Electromagnetic therapy meets this demand effectively, offering non-invasive pain relief and improved mobility. As global demographics shift toward older populations, healthcare providers are increasingly recommending electromagnetic therapy as part of comprehensive rehabilitation and pain management programs.

A rising preference for non-invasive, natural therapies is reshaping treatment trends worldwide. Patients and practitioners now favor solutions that avoid surgery or pharmaceuticals. Electromagnetic therapy aligns with this shift, delivering effective results with minimal side effects. Its growing acceptance in physiotherapy centers, rehabilitation clinics, and wellness facilities highlights a broader move toward holistic healthcare. Expanding use in sports medicine also contributes to visibility, with athletes and trainers using these devices for muscle recovery, fatigue reduction, and injury prevention.

The market outlook is further supported by favorable regulatory approvals, clinical validation, and improving healthcare infrastructure. Increasing research evidence has strengthened the clinical credibility of electromagnetic therapy, encouraging its integration into physiotherapy and rehabilitation guidelines. Emerging economies are investing in advanced healthcare and wellness technologies, boosting device adoption. Affordable and easy-to-use models are making electromagnetic therapy accessible to a wider population. Overall, the market is set for sustained growth as healthcare systems continue to adopt innovative, non-invasive therapeutic solutions.

Key Takeaways

- The global market is projected to reach USD 965.9 million by 2033, growing at a 7.9% CAGR from USD 451.6 million in 2023.

- Low Frequency devices accounted for 62.5% market share in 2023, driven by their proven safety, reliability, and therapeutic efficacy among consumers.

- Pain management applications led with 45.3% market share in 2023, followed by Bone Growth stimulation and other diversified therapeutic uses.

- Hospitals dominated the market with 51.8% share in 2023, though home care adoption is rising due to compact, user-friendly device designs.

- Market growth is supported by technological advancements in wearable electromagnetic therapy devices and increasing clinical research validating their therapeutic benefits.

- High costs of advanced devices and limited long-term clinical evidence remain key barriers to wider adoption in various end-user segments.

- Integration with IoT and AI presents opportunities for personalized electromagnetic therapy, expanding applications into new medical and wellness domains.

- Emerging trends include increased acceptance of Pulsed Electromagnetic Field (PEMF) therapy and development of affordable, wearable OTC solutions.

- North America led with 42.1% market share and USD 190.1 million in 2023, while Asia Pacific is forecasted to witness the fastest CAGR.

Regional Analysis

In 2023, North America dominated the electromagnetic therapy device market with a 42.1% share, valued at USD 190.1 million. The region’s leadership is supported by the strong presence of key manufacturers, advanced healthcare infrastructure, and early adoption of modern medical technologies. The United States remains the primary contributor, driven by an aging population, rising cases of chronic pain, and growing demand for non-invasive therapies. Additionally, government support for innovation in medical devices further strengthens regional market performance.

Europe held the second-largest share in the global electromagnetic therapy device market. The region benefits from developed healthcare systems, high adoption of advanced technologies, and a strong base of established manufacturers. Countries such as Germany, France, the UK, Italy, and Spain are major revenue contributors. The increasing prevalence of musculoskeletal disorders, coupled with a rising elderly population, is accelerating device adoption. Favorable healthcare policies and investments in medical research are also boosting the region’s overall market growth.

The Asia Pacific market is projected to witness the fastest growth rate over the forecast period. The expansion is supported by rising healthcare spending, supportive government initiatives, and increasing awareness of advanced therapeutic options. Emerging economies like China, India, and South Korea are key contributors due to rapid improvements in healthcare infrastructure. Meanwhile, Latin America and the Middle East & Africa are expected to show moderate growth. Factors such as expanding medical tourism, improving reimbursement frameworks, and growing healthcare access are positively influencing market development.

Segmentation Analysis

In 2023, the Electromagnetic Therapy Device market was led by the Low-Frequency segment, which captured over 62.5% of the total share. This dominance reflects consumers’ growing trust in devices that emit gentle yet effective electromagnetic waves. These devices are preferred for their safety and efficiency, making them suitable for various therapeutic purposes. In contrast, High-Frequency devices serve a smaller group seeking targeted benefits. The overall market trend highlights an increasing preference for comfort, safety, and non-invasive therapy options among health-conscious users.

The application landscape was dominated by the Pain Management segment, which held more than 45.3% of the market share in 2023. This growth can be attributed to the rising demand for non-invasive pain relief methods and the proven effectiveness of electromagnetic therapy. The Bone Growth segment also showed strong potential, driven by advancements in orthopedic care and an increase in bone-related disorders. Other applications, including wound healing, inflammation control, and neurological therapy, further contributed to the market’s expansion.

In terms of end use, hospitals commanded a significant share of over 51.8% in 2023, showcasing their reliance on electromagnetic therapy for patient treatments. Hospitals continue to adopt these devices due to their reliability and proven clinical results. The home care segment also gained attention, supported by device portability and ease of use. Individuals increasingly use these devices at home for wellness management. Additionally, wellness centers and smaller healthcare facilities contributed to market growth, emphasizing the therapy’s versatility across multiple care settings.

Key Market Segments

Power

- Low Frequency

- High Frequency

Application

- Pain management

- Bone Growth

- Others

End-use

- Hospitals

- Home Care Settings

- Others

Key Players Analysis

The Electromagnetic Therapy Device Market is driven by several key players contributing to technological advancement and market growth. Bedfont Scientific stands out for its innovative product development and strong focus on research and development. The company continually delivers advanced electromagnetic therapy solutions designed to meet various medical needs. Its commitment to healthcare innovation and product improvement enhances treatment efficiency and positions it as a leading force in the global market, ensuring sustained competitiveness and expanding its footprint across multiple healthcare applications.

Orthofix Holdings demonstrates significant expertise in the electromagnetic therapy sector, supported by its long-standing presence in orthopedic solutions. The company has successfully leveraged its technical capabilities and quality assurance standards to strengthen its position in this market. Orthofix’s emphasis on improving patient outcomes and ensuring product reliability enhances its reputation among healthcare professionals. Its strategic expansion into electromagnetic therapy devices further reinforces its contribution to the industry’s growth and technological advancement, making it a prominent player in the global healthcare landscape.

The I-Tech Medical Division plays an essential role in the market through its integration of innovation and clinical efficiency. The company focuses on developing user-friendly, effective, and technologically advanced devices that address specific therapeutic needs. Its strategic approach emphasizes precision and efficacy, ensuring high acceptance among healthcare providers. Through continuous innovation and product optimization, I-Tech Medical Division strengthens its market position and supports the global adoption of electromagnetic therapy devices in modern healthcare practices.

Beyond these leading companies, several other manufacturers and developers contribute significantly to market dynamism. Their unique technologies, diverse product offerings, and innovative approaches enhance competition and broaden accessibility for patients and healthcare institutions. Collectively, these players enrich the market landscape by providing varied options, fostering product development, and maintaining continuous improvement. This collaboration across industry participants supports steady market growth, ensuring effective therapeutic outcomes and expanding the reach of electromagnetic therapy solutions worldwide.

Electromagnetic Therapy Device Market Key Players are

- Bedfont Scientific

- Orthofix Holdings

- I-Tech Medical Division

- OSKA

- Medithera

- NiuDeSai

- Nuage Health

- Oxford Medical Instruments Health

- Bemer

Challenges

1) Evidence Variability and Study Heterogeneity

Clinical evidence supports PEMF therapy but remains inconsistent across conditions. Meta-analyses show short-term relief in osteoarthritis, yet long-term results are unclear. Study designs, dosing, and patient populations vary widely. This lack of uniform data makes it difficult to create universal treatment protocols. As a result, payers and clinical bodies remain cautious about adopting broad guidelines. To strengthen confidence, more standardized, large-scale clinical trials are required. Consistent data and clear outcome measures will help improve medical acceptance and payer coverage decisions.

2) Complex and Evolving Regulation

Regulations for electromagnetic therapy devices differ by region and evolve frequently. In the U.S., rTMS systems for depression are classified as Class II devices with strict performance and labeling controls. In the EU, MDR classification depends on intended use and risk, which can alter device class and evidence needs. Compliance requires significant investment, time, and specialized regulatory expertise. Manufacturers must stay updated with rule changes to avoid delays in approval. A well-defined regulatory strategy helps ensure faster market access and reduces long-term compliance risks.

3) Reimbursement Uncertainty and Regional Variation

Reimbursement policies for electromagnetic therapy devices vary by region. In the U.S., Medicare covers TMS for major depressive disorder, but conditions differ by Local Coverage Determination (LCD). Requirements such as diagnosis proof, prior treatment failure, and limited session counts restrict coverage. These conditions reduce utilization and make revenue forecasting difficult for providers. Inconsistency across regions adds to uncertainty for both clinics and manufacturers. Clearer reimbursement policies and evidence-based advocacy are essential to ensure wider access and financial stability for therapy centers.

4) Safety, Electromagnetic Interference (EMI), and Contraindications

Electromagnetic therapy devices must address potential interference risks. Patients with implants like pacemakers or metal devices face safety concerns during TMS or PEMF sessions. Even magnets in consumer electronics can disrupt cardiac devices. Manufacturers must design products that minimize EMI and provide clear usage warnings. Proper screening and operator training are critical to prevent incidents. In both clinical and home settings, strict adherence to safety protocols ensures patient confidence. Transparent guidance helps protect patients and supports trust in device safety standards.

5) Standards Compliance and Verification Burden

Medical electrical devices must comply with IEC 60601 standards for electrical safety and performance. Each product may need to meet several related parts and collateral requirements. This adds complexity, testing costs, and time to the approval process. Verification involves multiple stages, including safety, software, and electromagnetic compatibility testing. Smaller companies may find compliance particularly burdensome. However, adherence to these standards is essential for market entry and international acceptance. Streamlined testing processes and early planning can help reduce delays and costs.

6) Public Perceptions and Communications

Public skepticism about electromagnetic fields remains a challenge. Misconceptions about safety and radiation risks can affect acceptance of PEMF and TMS therapies. Companies must invest in clear education, transparent communication, and ongoing post-market monitoring. Sharing real-world data and safety reports can counter misinformation effectively. Engaging healthcare professionals and patients in awareness campaigns builds credibility. Honest communication ensures that scientific facts outweigh myths, leading to improved public trust and device adoption in the long term.

7) Clinical Workflow and Training

rTMS therapy requires skilled professionals and structured workflows. Each session demands precise patient positioning, timing, and supervision. Smaller clinics face challenges in managing costs, training staff, and maintaining schedules before achieving patient volume stability. Operational complexity can slow adoption despite clinical benefits. Standardized training programs and user-friendly devices can simplify implementation. Support from manufacturers in setup and education helps clinics improve efficiency. Building confidence among operators ultimately drives higher treatment adoption and patient satisfaction.

Opportunities

1) Diversifying, FDA-Cleared Indications

The U.S. FDA has cleared electromagnetic therapy systems for multiple uses, including major depressive disorder (MDD), migraine with aura (single-pulse TMS), obsessive-compulsive disorder (OCD), and short-term smoking cessation. This expansion of approved indications supports the growth of multi-use device platforms. Clinics can utilize the same systems for various conditions, improving efficiency and return on investment. Multi-indication systems also promote cross-referrals among specialties such as neurology, psychiatry, and pain management. This diversification helps reduce downtime, improve patient throughput, and strengthen the overall clinical and business case for electromagnetic therapy devices.

2) Unmet Needs in Pain and Musculoskeletal Care

Pulsed electromagnetic field (PEMF) therapy demonstrates measurable benefits in osteoarthritis pain relief and improved joint function. These outcomes make PEMF a valuable tool for conservative care and post-operative recovery. With growing demand for non-invasive and drug-free options, home-use PEMF devices are emerging as a key growth area. Portable and easy-to-use designs can increase patient adherence and accessibility, especially among elderly or mobility-limited patients. Manufacturers focusing on ergonomic design and digital tracking can attract both healthcare providers and consumers seeking convenient pain management solutions.

3) Reimbursement Tailwinds for Priority Indications

Reimbursement trends are favorable for electromagnetic therapies. Medicare Local Coverage Determinations (LCDs) for TMS in major depressive disorder have set a strong precedent. Commercial insurers often follow these standards, creating a wider coverage network. Providers that align with LCD criteria and document treatment outcomes can secure consistent payer adoption. These developments encourage clinics to invest in new equipment, staff training, and standardized treatment protocols. As more evidence supports clinical efficacy, reimbursement access will continue to expand, improving patient access and promoting broader market adoption.

4) Strong Safety Frameworks and Standards

Electromagnetic therapy devices benefit from mature global safety standards. Compliance with the IEC 60601 series and FDA special controls ensures product reliability and patient protection. Vendors that meet or exceed these standards can differentiate themselves through strong risk management and safety transparency. Clear engineering targets reduce regulatory uncertainty and speed up market entry. Human-factor testing and usability studies further build clinical confidence among practitioners. As safety becomes a key purchasing factor, adherence to international frameworks can enhance brand trust and drive long-term partnerships with healthcare providers.

5) Evidence Expansion and Guideline Engagement

Health authorities such as NICE are continuing to evaluate electromagnetic therapy. This presents a strong opportunity for manufacturers to expand clinical evidence through trials, registries, and real-world studies. Aligning research with guideline committees’ questions helps turn provisional recommendations into official endorsements. Demonstrating cost-effectiveness, improved outcomes, and patient satisfaction can strengthen coverage and reimbursement decisions. Companies that invest in evidence development can build long-term credibility and influence future policy updates. Continuous collaboration with research institutions and clinical leaders will support guideline evolution and accelerate market acceptance.

6) Digital and Service Add-Ons

The integration of digital tools into electromagnetic therapy devices presents a major opportunity. Add-ons such as dosing analytics, treatment planning software, and remote adherence monitoring can improve patient engagement and clinical outcomes. These features help reduce no-shows, optimize treatment schedules, and collect valuable outcomes data for payers and providers. Data-driven platforms can also support predictive maintenance and usage tracking, increasing operational efficiency. By combining regulated therapy hardware with smart digital ecosystems, manufacturers can create new revenue streams and enhance provider value through measurable treatment insights.

Conclusion

The global electromagnetic therapy device market is expected to grow steadily, driven by the rising preference for non-invasive and drug-free treatment options. Growing awareness of the therapy’s benefits in pain management, rehabilitation, and wellness is improving its acceptance in both clinical and home settings. Technological advancements such as wearable and digital-enabled devices are expanding access and usability. Despite challenges related to regulation and clinical consistency, increasing research support and strong safety standards are enhancing credibility. With expanding healthcare infrastructure and supportive policies worldwide, electromagnetic therapy devices are poised to become a key part of modern pain relief and recovery solutions in the coming years.

View More

Electronic Health Records Market | Electromechanical Dental Chair Market | Electrolyte Markers Market | Ambulatory Electrocardiography Market | Cryo Electron Microscopy Market | Portable Medical Electronic Products Market | Electrophysiology Market | Electrosurgical Devices Market | Blood Gas and Electrolyte Analyzers Market | Electroceuticals/Bioelectric Medicine Market | Electrophoresis Reagents Market | Electronic Skin Patch Market

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)