Table of Contents

Overview

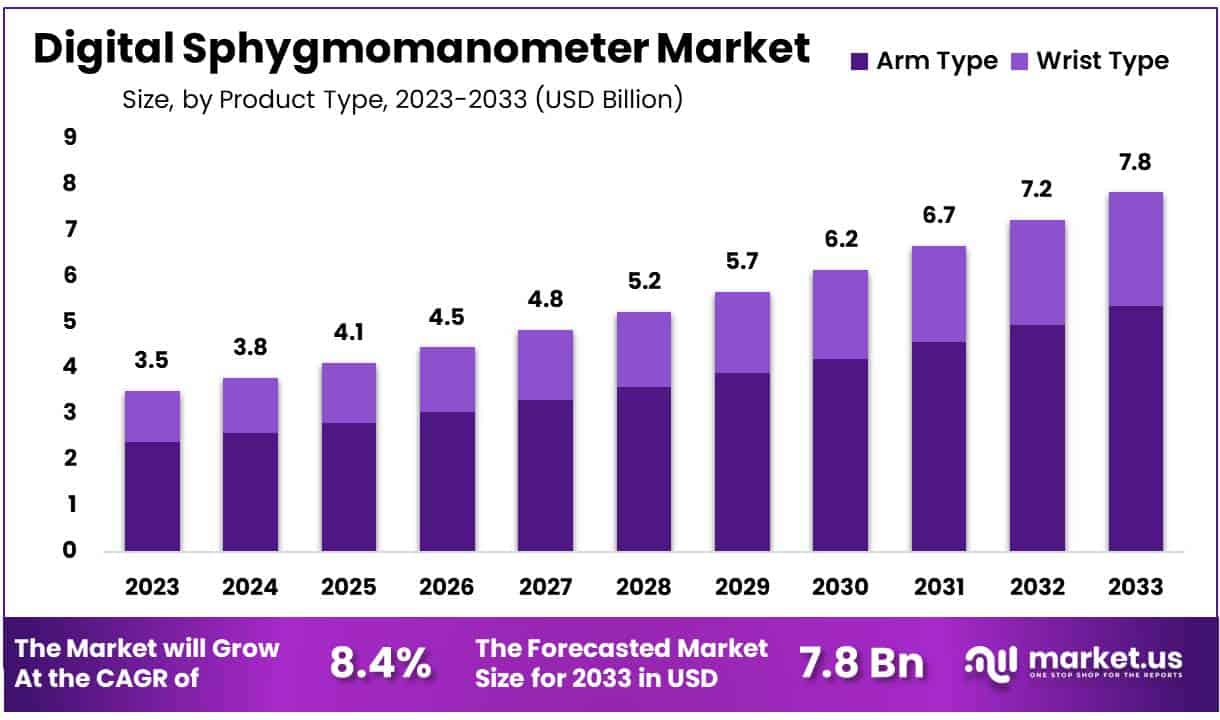

New York, NY – Jan 09, 2026 – Global Digital Sphygmomanometer Market size is expected to be worth around US$ 7.8 Billion by 2033 from US$ 3.5 billion in 2023, growing at a CAGR of 8.4% during the forecast period 2024 to 2033.

A digital sphygmomanometer is a medical device used to measure blood pressure through electronic and automated mechanisms. It is widely adopted across hospitals, clinics, and home healthcare settings due to its ease of use, accuracy, and minimal requirement for technical expertise. Unlike traditional mercury or aneroid devices, digital sphygmomanometers display blood pressure readings on a digital screen, reducing the risk of human error during measurement.

The basic formation of a digital sphygmomanometer includes an inflatable cuff, an electronic pressure sensor, a microprocessor, and a digital display unit. The cuff is wrapped around the upper arm or wrist and inflated automatically using an internal pump. As the cuff deflates, the pressure sensor detects arterial pressure changes. These signals are processed by the microprocessor, which calculates systolic and diastolic blood pressure values and displays them clearly on the screen.

Additional features such as memory storage, irregular heartbeat detection, and averaging of multiple readings are increasingly being integrated into modern devices. These features support better monitoring and long-term management of hypertension. Battery operation or rechargeable power systems further enhance portability and convenience.

The growing prevalence of cardiovascular diseases and rising awareness of preventive healthcare have contributed to increased demand for digital sphygmomanometers. The shift toward home-based health monitoring has also supported market expansion. As healthcare systems continue to emphasize early diagnosis and continuous monitoring, digital sphygmomanometers are expected to remain an essential component of routine blood pressure management.

Key Takeaways

- In 2023, the digital sphygmomanometer market generated revenue of approximately US$ 3.5 billion and is projected to expand at a compound annual growth rate (CAGR) of 8.4%, reaching an estimated US$ 7.8 billion by 2033.

- By product type, the market is segmented into arm type and wrist type devices. Among these, arm-type digital sphygmomanometers dominated the market in 2023, accounting for a leading 68.5% share, supported by higher clinical accuracy and widespread adoption.

- Based on end-user, the market is categorized into hospitals, ambulatory surgical centers & clinics, homecare settings, and others. Homecare settings emerged as the largest end-user segment, capturing a substantial 45.2% market share, driven by the growing preference for self-monitoring and remote healthcare solutions.

- From a regional perspective, North America held the dominant position in the global market, securing a 39.7% share in 2023, supported by advanced healthcare infrastructure, high awareness of hypertension management, and strong adoption of digital medical devices.

Regional Analysis

North America Leads the Digital Sphygmomanometer Market

North America accounted for the largest revenue share of 39.7% in the digital sphygmomanometer market, supported by high awareness of hypertension and the growing emphasis on routine blood pressure monitoring. The rising incidence of lifestyle-related conditions, including obesity and physical inactivity, has increased the prevalence of hypertension, thereby strengthening demand for accurate and user-friendly monitoring devices across clinical and homecare environments.

Market momentum has also been reinforced by strategic corporate developments. The completion of Baxter’s acquisition of Hillrom in December 2021 expanded Baxter’s healthcare portfolio, enabling broader delivery of advanced medical equipment and monitoring solutions. This integration has improved access to digital sphygmomanometers within hospitals and care settings.

Additionally, the rapid adoption of telehealth and remote patient monitoring has accelerated device usage in homecare settings. Ease of operation, data tracking, and compatibility with digital health platforms have positioned digital sphygmomanometers as essential tools in preventive cardiovascular care.

Asia Pacific Expected to Record the Fastest Growth

The Asia Pacific region is projected to witness the highest CAGR during the forecast period. Growth is being driven by rising healthcare awareness, urbanization, and increasing hypertension prevalence. In December 2021, OMRON Healthcare partnered with Doctor Anywhere to integrate smart monitoring devices with telehealth services, supporting remote hypertension management. Alongside supportive government initiatives, these factors are expected to sustain strong regional market expansion.

Emerging Trends

- Integration with Telehealth and Remote Patient Monitoring (RPM): Digital sphygmomanometers are increasingly being integrated into telehealth ecosystems, enabling automatic transmission of blood pressure readings to healthcare providers. This development supports the expansion of RPM programs, where self-measured blood pressure (SMBP) data can be reviewed asynchronously. As a result, reliance on routine in-office visits is reduced, while continuity of care is maintained.

- Bluetooth and Smartphone Connectivity: The adoption of Bluetooth and cellular-enabled digital sphygmomanometers has increased steadily. These features allow seamless synchronization with mobile applications, supporting real-time data sharing, longitudinal trend analysis, and improved patient engagement through alerts, reminders, and visual dashboards.

- Insurance Coverage and Policy Support: Public payer policies in the United States have increasingly recognized SMBP as a reimbursable care component. Initiatives involving the Centers for Disease Control and Prevention and the American Medical Association are evaluating Medicaid reimbursement for validated automatic upper-arm devices. Such policy support is expected to reduce patient cost burdens and encourage adoption, particularly among underserved populations.

- Increasing Device Affordability: Improvements in manufacturing efficiency and intensified supplier competition have contributed to declining prices of digital sphygmomanometers. The availability of low-cost, clinically accurate devices has expanded access to home blood pressure monitoring, reducing economic barriers that previously limited uptake.

- EHR Integration for Population-Level Surveillance: Growing emphasis on electronic health record (EHR)-based hypertension surveillance has increased demand for digital sphygmomanometers with robust data-export capabilities. Integration with EHR systems enables timely monitoring of population-level blood pressure trends and supports targeted public health planning and intervention strategies.

Use Cases

- Home Blood Pressure Management: Digital sphygmomanometers are widely used in home settings to support regular blood pressure monitoring. This application is particularly relevant given that approximately 47.7% of U.S. adults experienced hypertension between August 2021 and August 2023, while fewer than one-quarter achieved adequate control. Routine home measurements, conducted daily or weekly, enhance patient awareness and adherence to prescribed treatment regimens.

- Remote Patient Monitoring Programs: Within clinical care models, digital sphygmomanometers are deployed as core components of RPM programs. Blood pressure data are transmitted automatically to healthcare providers, enabling timely intervention. Utilization increased significantly during the COVID-19 pandemic, ensuring continuity of care for patients with chronic cardiovascular conditions.

- Team-Based Care and Improved Outcomes: Self-measured blood pressure programs combined with team-based care models, including pharmacist involvement, have demonstrated substantial long-term benefits. These approaches are projected to prevent up to 91,900 heart attacks and 139,000 strokes over five years, while generating average healthcare cost savings of approximately US$ 7,794 per individual over a 20-year period. Digital sphygmomanometers serve as the primary source of reliable patient-generated data within these models.

- Public Health Surveillance and Research: Digital sphygmomanometers with EHR connectivity are increasingly utilized in chronic disease surveillance and epidemiological research. Continuous data collection enables monitoring of hypertension prevalence and control rates over time, supporting evidence-based resource allocation and the design of targeted interventions in high-burden communities.

Frequently Asked Questions on Digital Sphygmomanometer

- How does a digital sphygmomanometer work?

The device operates by inflating an arm or wrist cuff and detecting arterial pressure oscillations during deflation. These oscillations are processed through algorithms to calculate accurate blood pressure values displayed digitally. - What are the key advantages of digital sphygmomanometers over manual devices?

Digital sphygmomanometers offer ease of use, minimal training requirements, faster readings, and improved accuracy. They eliminate the need for stethoscopes and reduce variability caused by human interpretation and environmental noise. - Are digital sphygmomanometers accurate for home use?

When clinically validated and used correctly, digital sphygmomanometers provide reliable results for home monitoring. Accuracy is influenced by proper cuff size, correct positioning, and adherence to manufacturer usage guidelines. - What factors should be considered when purchasing a digital sphygmomanometer?

Key considerations include clinical validation status, cuff size range, memory storage capacity, display readability, power source, and connectivity features. These factors influence measurement reliability, user convenience, and long-term usability. - What is the current scope of the digital sphygmomanometer market?

The market encompasses devices used across hospitals, clinics, ambulatory centers, and home healthcare settings. It includes arm-type and wrist-type monitors, supported by increasing adoption of automated diagnostic technologies globally. - What are the key drivers of the digital sphygmomanometer market?

Market growth is driven by rising hypertension prevalence, aging populations, increased home healthcare adoption, and technological advancements. Government initiatives promoting preventive healthcare further support demand for accurate blood pressure monitoring solutions. - How is technological innovation influencing the market?

Technological advancements such as Bluetooth connectivity, smartphone integration, cloud-based data storage, and AI-driven analytics are enhancing device functionality. These innovations improve patient monitoring, data tracking, and clinical decision-making efficiency. - Which end-user segment dominates the digital sphygmomanometer market?

The home healthcare segment holds a significant market share due to increasing self-monitoring awareness. Hospitals and clinics also contribute substantially, supported by routine patient monitoring requirements and standardized diagnostic protocols. - What is the future outlook for the digital sphygmomanometer market?

The market is expected to experience steady growth, supported by chronic disease management trends and digital health adoption. Expansion in emerging economies and continued product innovation are anticipated to strengthen long-term market prospects.

Conclusion

The digital sphygmomanometer market demonstrates sustained growth potential, driven by rising hypertension prevalence, expanding home healthcare adoption, and continuous technological advancements. Automated operation, improved accuracy, and digital connectivity have positioned these devices as essential tools in both clinical and home-based blood pressure management.

Strong demand from homecare settings, coupled with supportive reimbursement policies and telehealth integration, continues to reshape monitoring practices. Regional leadership by North America and rapid growth in Asia Pacific further underline global market momentum. Overall, digital sphygmomanometers are expected to remain central to preventive cardiovascular care and long-term disease management strategies.