Table of Contents

Overview

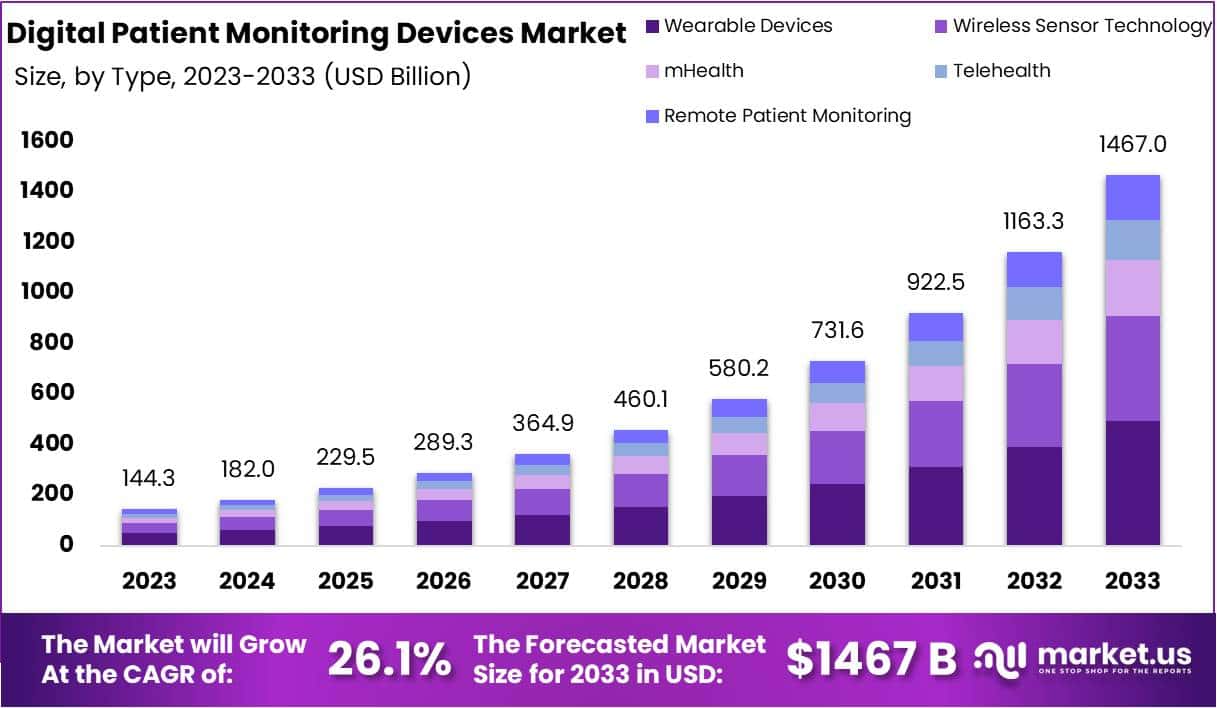

The Global Digital Patient Monitoring Devices Market is projected to reach USD 1,467 billion by 2033, rising from USD 144.3 billion in 2023. Growth is supported by the increasing need for continuous and remote health tracking. Chronic conditions such as diabetes, hypertension, and cardiovascular diseases require frequent observation. Digital tools enable real-time data collection and reduce unnecessary clinic visits. As healthcare providers shift toward efficient patient management, the demand for connected monitoring technologies continues to strengthen.

The expansion of telemedicine has accelerated adoption. Remote consultations have become more routine because they provide time savings and increase access to care. Digital monitoring devices supply accurate readings such as heart rate, oxygen saturation, and glucose levels. These measurements support clinical decisions during virtual appointments. As telemedicine platforms scale globally, integrated monitoring devices are expected to remain essential components of remote healthcare services.

The widespread use of smartphones and wearable technologies has further supported market growth. Many monitoring systems connect seamlessly with mobile applications, enabling patients to track their health independently. This simplified experience is valuable for older adults who require easy-to-use digital tools. App-based dashboards have improved awareness of personal wellness. The rise of consumer health technologies has encouraged broader acceptance of at-home monitoring solutions.

Technological advancements have also strengthened the market. Enhanced sensors, improved battery life, and reliable wireless networks have increased device accuracy and performance. Artificial intelligence is being integrated to support early detection of risks and automated alerts. These capabilities help reduce hospital admissions and promote preventive care. Healthcare providers benefit from operational efficiency, as remote monitoring reduces follow-up visits and allows staff to prioritize high-acuity patients.

Supportive government initiatives have contributed to the sector’s expansion. Many countries promote digital health frameworks and electronic health record integration, making adoption easier for hospitals and clinics. Growing awareness of personal health and the shift toward home-based care further stimulate demand. Patients increasingly prefer managing conditions from home while maintaining real-time communication with clinicians. This preference, combined with cost savings for families and healthcare systems, is expected to sustain long-term market growth.

Key Takeaways

- The global digital patient monitoring devices market was reported at USD 144.3 billion in 2023 and is projected to surpass USD 1467 billion, supported by a 26.1% CAGR.

- The wearable devices category was identified as the leading type segment in 2023, supported by a 33.6% market share driven by strong consumer and clinical adoption.

- Diagnostic patient monitoring devices were recognized as the dominant product segment, securing a significant 70.8% share due to extensive use in clinical assessment and continuous health evaluation.

- North America was highlighted as the leading regional market, accounting for 41.9% of global revenue, supported by advanced healthcare infrastructure and early technology uptake.

Regional Analysis

North America has been identified as the leading region in the digital patient monitoring devices market. The region accounted for 41.9% of total revenue in 2023. This dominance has been supported by strong healthcare infrastructure and high adoption of advanced medical technologies. Remote monitoring has become common in the United States. It has been reported that around 50 million people use such devices. These tools help patients track their conditions at home and allow clinicians to access real-time health information.

The growth of the market in North America has been attributed to the rising prevalence of chronic illnesses. Chronic diseases such as diabetes and heart conditions require continuous monitoring. Digital solutions support early detection and timely interventions. Rapid technological innovations have further strengthened the regional demand. The aging population continues to rise, creating a larger user base for these monitoring tools. As a result, the regional market is expected to maintain its leadership during the forecast period.

Asia Pacific is projected to record the highest CAGR in the digital patient monitoring devices market during the forecast period. This strong growth outlook is driven by the increasing burden of cardiovascular and respiratory diseases across several countries. Lifestyle changes, including reduced physical activity and rising stress levels, have contributed to this situation. Healthcare awareness is improving steadily. Growing focus on preventive care is also boosting product adoption. As medical needs expand, the demand for efficient monitoring systems is expected to accelerate rapidly.

The Asia Pacific region benefits from a large and diverse customer base, which strengthens long-term market potential. Expanding healthcare infrastructure in emerging economies supports device penetration. Governments are investing in digital health solutions to enhance patient care, which promotes market expansion. Increasing urbanization and rising income levels have created favorable conditions for the adoption of advanced medical technologies. These factors together indicate strong future growth. The region is expected to become a major contributor to global market revenue over the coming years.

Segmentation Analysis

The market has been classified by type into wearable devices, wireless sensor technology, mHealth, telehealth, and remote patient monitoring. Wearable devices accounted for the highest revenue share in 2023. The segment held 33.6% of the total market value. This dominance was supported by rising adoption of smart health trackers. Growth was also influenced by higher consumer awareness of preventive care. The expansion of connected devices further strengthened demand. Adoption increased steadily across developed markets. Emerging economies also showed strong uptake.

The mHealth segment is projected to expand at the fastest pace during the forecast period. Its growth is supported by the rising number of smartphone users. Internet penetration has also increased rapidly across several regions. These factors strengthened digital engagement and boosted remote care solutions. Higher acceptance of mobile-based health applications also contributed to market traction. The segment is expected to benefit from growing interest in self-health management. Improved app functionality further accelerates adoption. Supportive government programs enhance long-term prospects.

The market has also been segmented by product into diagnostic and therapeutic devices. Diagnostic patient monitoring devices remained the dominant category in 2023. The segment secured a 70.8% share of the total market. Demand growth was influenced by the rising burden of chronic diseases. Early detection needs increased across major healthcare systems. The segment also benefited from technological upgrades in monitoring tools. Wider integration of connected diagnostic systems supported adoption. Population aging further strengthened market demand. Hospitals and clinics remained the primary users.

Respiratory monitoring devices and blood glucose monitors contributed significantly to the dominance of diagnostic products. Their adoption increased in response to rising respiratory disorders and diabetes cases. These devices are widely used for continuous assessment and timely intervention. Improved accuracy and real-time data transmission supported their uptake. Manufacturers also introduced advanced measurement features. This enhanced clinical decision-making in various care settings. Home-based monitoring solutions gained more acceptance. The overall segment is expected to maintain strong momentum over the forecast period.

Key Market Segments

By Type

- Wearable Devices

- Wireless Sensor Technology

- mHealth

- Telehealth

- Remote Patient Monitoring

By Product

- Diagnostic Monitoring Devices

- Therapeutic Monitoring Devices

Key Players Analysis

The competitive structure of the digital patient monitoring devices market has been shaped by steady technological progress and rising clinical adoption. Market growth has been driven by the development of connected solutions, remote monitoring platforms, and sensor-based systems. Large companies continue to strengthen their positions through innovation pipelines and digital integration strategies. Firms such as Omron Corporation, Philips Healthcare, and GE Healthcare support this advancement with strong portfolios that address chronic disease management and real-time patient data collection needs across diverse healthcare environments.

Strategic initiatives have been widely used to secure higher market penetration and enhance product reach. The expansion of telehealth services has increased the importance of interoperability, cybersecurity, and analytics. Established participants have responded through acquisitions, partnerships, and ecosystem development to broaden monitoring capabilities. Companies including AT&T Inc., Athenahealth Inc., and AirStrip Technologies have integrated communication technologies with clinical platforms to strengthen data-sharing efficiency and improve remote patient oversight in hospitals and home-care settings.

Smaller firms and emerging innovators have contributed significantly to segment specialization. Their focus has been directed toward niche solutions that address targeted monitoring requirements and advanced wearable systems. These companies often concentrate on flexible designs, cloud-based reporting, and cost-effective tools suited for specific user groups. Entities such as Zephyr Technology Corporation and Welch Allyn provide differentiated offerings that complement the broader portfolios of major manufacturers. Their agility enables faster adoption of new features and supports unmet clinical demands in specialized care areas.

Collaborative developments continue to shape competitive dynamics by fostering integration between monitoring hardware, software platforms, and healthcare networks. Partnerships among technology providers and medical device manufacturers have improved remote diagnostics and predictive analytics. This cooperative environment strengthens market expansion and enhances user acceptance across clinical workflows. Firms like Jude Medical and other emerging players participate in these alliances to broaden product capabilities and strengthen operational presence, contributing to a market landscape defined by innovation and steady technological advancement.

Challenges

1. Data Privacy and Security Issues

Data privacy concerns have been rising as digital patient monitoring devices collect sensitive health information. Large volumes of data increase the chances of breaches and unauthorized access. Strict regulations require strong protection measures, which add pressure on manufacturers and healthcare providers. Compliance demands have also increased operational complexity. As a result, organizations are required to invest in secure systems, regular audits, and advanced encryption. These needs have slowed adoption, especially where cybersecurity capabilities remain limited.

2. High Initial Investment

Digital patient monitoring devices often require major upfront spending. Hospitals and clinics must upgrade existing systems, which creates financial strain. Budget limitations are common, especially in small facilities and public healthcare settings. The need for hardware, software, integration, and training further increases total costs. These expenses reduce the pace of adoption in emerging markets. High investment requirements also delay modernization efforts. Overall, cost barriers remain a significant challenge for wider market penetration.

3. Limited Technical Skills

Healthcare staff often lack the digital skills needed to manage advanced monitoring devices. Specialized training is required to use these systems correctly. Without proper knowledge, devices may remain underused or misconfigured. This slows workflow efficiency and affects clinical outcomes. Implementation timelines also become longer because teams need time to adjust. Technical complexity adds pressure on organizations with limited IT support. As a result, skill gaps continue to hinder smooth adoption of digital monitoring technologies.

4. Connectivity and System Integration Issues

Reliable internet connectivity is essential for real-time digital monitoring. Poor network coverage reduces device performance, especially in rural or remote areas. System integration has also been a significant challenge. Many hospitals use legacy systems that are difficult to connect with modern digital platforms. This creates operational disruptions and reduces the efficiency of data sharing. Integration failures can delay clinical decisions and increase workload. These issues continue to affect overall system reliability and adoption.

5. Concerns About Device Accuracy

Device accuracy remains a critical issue in digital patient monitoring. Some devices produce inconsistent readings due to sensor limitations or poor calibration. Any error in measurement can affect diagnosis and patient safety. Clinicians may hesitate to rely on devices that show variations in performance. This creates trust issues and slows adoption. Manufacturers are required to improve reliability through testing and validation. Accuracy concerns continue to influence purchasing decisions and overall market acceptance.

Opportunities

1. Growing Demand for Remote Healthcare

Demand for remote healthcare has been rising as more patients choose home-based care. The shift toward digital tools has supported wider adoption of remote patient management systems. Chronic diseases such as diabetes and heart conditions have benefited the most because continuous tracking helps reduce complications. The market has gained momentum as healthcare teams rely on constant data to guide decisions. This trend continues to create steady growth for digital monitoring devices.

2. Rising Adoption of Wearable Devices

Wearable devices have become common in daily life as consumers use smartwatches, fitness trackers, and connected sensors. These tools have made people more aware of their health data. Their growing use has encouraged interest in medical-grade digital monitoring products. Manufacturers have gained new opportunities as wearables bridge the gap between consumer wellness and clinical care. This broader acceptance has supported stronger market growth and created a favorable environment for digital monitoring innovation.

3. Advancements in AI and Analytics

AI and advanced analytics have improved the accuracy and speed of patient monitoring. These technologies can predict risks earlier by analyzing continuous data. Early warnings help doctors act before conditions worsen. Automation has also reduced manual work and increased the value of digital monitoring systems. The ability to process large datasets has strengthened clinical decision making. This progress has created strong opportunities for companies developing intelligent monitoring platforms.

4. Expansion of Telehealth Services

Telehealth adoption has increased quickly as more patients choose virtual consultations. Digital monitoring devices support this shift by supplying real-time health data during remote visits. Continuous analytics make online care smoother and more effective. Healthcare providers have been able to monitor patients outside clinics, which improves outcomes. This shift has created strong demand for integrated digital ecosystems. As telehealth expands worldwide, the market for monitoring devices is expected to grow further.

5. Focus on Preventive Healthcare

Healthcare systems have been moving toward prevention rather than treatment. Digital monitoring devices play a key role because they track early changes in vital signs. Early detection allows faster intervention and reduces long-term risks. This shift has created opportunities in wellness, fitness, and home-based care. Consumers are now more willing to use tools that promote healthier lifestyles. As a result, preventive healthcare has become a major driver for market expansion.

6. Rising Use in Elderly Care

The global elderly population has been increasing, creating higher demand for continuous monitoring. Digital patient monitoring devices help caregivers track vital signs and detect issues early. This support improves safety and reduces emergency risks for older adults. Families and healthcare providers rely on these tools to deliver consistent care at home. The long-term need for elderly monitoring solutions has created strong market potential. This demographic trend continues to influence future growth.

Conclusion

The digital patient monitoring devices market is expected to expand steadily as healthcare systems adopt connected and remote care solutions. Growth is driven by rising chronic health conditions, broader use of telehealth, and increasing interest in home-based monitoring. Wearable devices and mobile health applications support continuous tracking, while technological progress has improved accuracy and ease of use. Supportive government policies and a growing elderly population further strengthen long-term demand. Although challenges such as data security, high costs, and skill gaps remain, ongoing innovation and preventive care trends continue to create strong opportunities for wider adoption across global healthcare settings.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)