Table of Contents

Overview

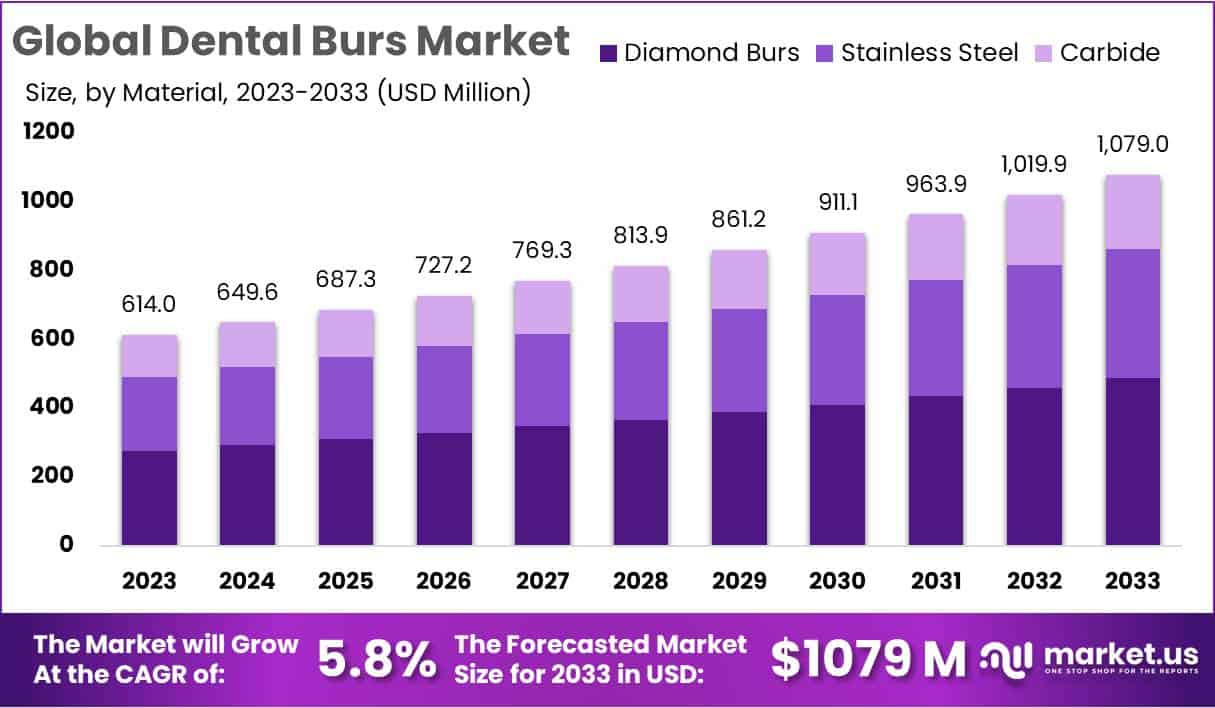

The Dental Burs Market is projected to expand significantly in the coming decade. The global market is estimated to grow from USD 614 million in 2023 to approximately USD 1,079 million by 2033. This represents a compound annual growth rate (CAGR) of 5.8% from 2024 to 2033. The market expansion is closely linked to rising demand for dental care worldwide, as oral diseases remain one of the most prevalent health concerns globally.

The Global Burden of Disease study indicates that 3.7 billion people are currently affected by oral conditions, with dental caries being the most common. The high disease burden directly increases the need for restorative and surgical interventions, which depend heavily on rotary instruments like burs. Clinics and laboratories are therefore experiencing higher utilization, leading to consistent demand for diamond and carbide burs across diverse dental procedures.

Population aging is another structural driver. The World Health Organization projects that by 2030, one in six people will be over the age of 60. Furthermore, the number of people aged 80 and older is expected to triple by 2050. Older adults show higher rates of tooth decay, periodontal disease, and tooth loss, generating increasing demand for crowns, bridges, implants, and dentures. Each of these treatments requires multiple bur applications, reinforcing long-term consumption patterns.

Healthcare data from leading countries illustrates this shift. The UK National Health Service recorded 35 million dental treatment courses in 2024/25, marking a 4% year-on-year increase. Such volume recovery in routine and urgent care directly supports a steady rise in bur utilization.

Demand Patterns and Service Utilization

Rising procedure volumes and preventive care indicators highlight growing consumption trends. Data from Eurostat shows dentist consultation rates across the European Union ranging from 0.6 to 1.7 visits per inhabitant annually, with the Netherlands reaching as high as 3.4. Such regular attendance sustains preventive, restorative, and surgical interventions, reinforcing replacement cycles for burs. These metrics underline how consistent patient inflow drives steady usage of cutting instruments in both private and public settings.

Global health policies are reinforcing this trajectory. The World Health Organization has launched a Global Strategy on Oral Health, with an action plan covering 2023 to 2030. The initiative encourages countries to integrate oral health into primary healthcare and expand treatment capacity. As national programs scale, the installed base of operatories is expected to rise, driving higher procedural volumes and greater demand for dental burs.

Infection-control regulations also shape purchasing behavior. The U.S. Centers for Disease Control and Prevention recommends single-use devices for each patient to prevent cross-contamination. This guidance supports adoption of disposable burs rather than reusable ones, particularly in clinics that prioritize compliance. Stricter validation requirements for reprocessing diamond-coated burs further encourage the purchase of sterile, ready-to-use products. This trend creates an environment in which product turnover is accelerated, expanding overall market size.

These structural changes are already visible in national healthcare systems. Governments are working to reduce treatment backlogs and expand access, as evidenced by Australia’s efforts to manage waiting times in public dentistry. As throughput increases, demand for burs across preventive, restorative, and surgical cases is expected to remain strong.

Technology and Economic Context

Technological innovation is broadening product use and replacement rates. The rapid adoption of digital dentistry, including CAD/CAM workflows, 3D imaging, and in-office fabrication, has intensified the frequency of tooth preparation and adjustment procedures. Faster preparation cycles combined with harder restorative materials increase bur wear, resulting in more frequent replacement. This trend enhances overall product demand as practices adopt advanced workflows.

Regulatory frameworks and economic trends provide additional support. Rising healthcare expenditures across OECD countries contribute to capital budgets that modernize dental equipment, including handpieces and rotary systems. As health systems recover from pandemic disruptions, public activity levels are stabilizing and expanding. These conditions underpin a resilient baseline demand for dental burs across developed and emerging markets.

Moreover, infection-prevention awareness and digital workflows converge to influence product preferences. Clinics adopting CAD/CAM systems often need a wider range of burs, with more rapid replacement cycles. Disposable burs gain an advantage in such workflows, aligning with infection-control standards and efficiency goals. The combined effect is increased product penetration across both general and specialized practices.

Looking forward, access programs in multiple countries are expected to maintain demand. Public health systems, such as Australia’s, continue to expand coverage for vulnerable populations, directly translating into higher procedure volumes. As governments and health organizations align on oral health integration, the long-term outlook for the dental burs market remains favorable, supported by demographic shifts, policy initiatives, and technological advancements.

Key Takeaways

- By 2033, the dental burs market is expected to reach USD 1,079 million, advancing steadily at a CAGR of 5.8% from 2024.

- Diamond burs held a dominant 45.1% market share in 2023, reflecting the industry’s shift toward advanced, durable, and precision-driven dental tool materials.

- Cavity preparation emerged as the leading application in 2023, accounting for 29.3% market share, underlining its significance in accurate dental procedures.

- Cavity preparation and oral surgery collectively demonstrated strong end-use dominance in 2023, shaping demand trends within the global dental burs market.

- Market growth is being driven by technological advancements, increasing global dental procedures, and rising treatment demand from a rapidly aging population.

- However, challenges include the high cost of advanced burs, limited reimbursement policies, and persistent sterilization-related concerns in clinical settings.

- Opportunities exist in specialized burs development, penetration into untapped emerging markets, and strategic collaborations aimed at fostering product innovation and accessibility.

- Emerging trends include growing adoption of diamond burs, nanotechnology integration, CAD/CAM customization, and sustainable eco-friendly material advancements in dental burs manufacturing.

- North America captured over 52% market share in 2023, driven by advanced healthcare systems, strategic alliances, and supportive regulatory frameworks.

- Going forward, technological innovations and continued collaborations are anticipated to reinforce North America’s leadership in the global dental burs market landscape.

Regional Analysis

In 2023, North America emerged as the leading region in the Dental Burs Market, with a market share surpassing 52% and a value of USD 257.2 million. The region’s dominance is attributed to a strong healthcare infrastructure and advanced dental facilities. High awareness among patients and professionals further accelerated adoption. The emphasis on modern dentistry and preference for innovative instruments have supported growth. The advanced healthcare system continues to create a favorable environment, positioning North America at the forefront of market development.

The market’s expansion is strongly supported by demographic and health trends. A rising aging population, combined with increasing cases of dental disorders, has driven the need for frequent dental procedures. Older individuals often require specialized treatments, boosting the demand for dental burs in clinical practice. The trend toward preventive dental care has also increased procedure volumes. These factors together contribute significantly to market growth, strengthening the region’s role as a primary driver of demand in the global Dental Burs Market.

Collaborations and regulations have further fueled the industry’s progress. Strategic partnerships between manufacturers and dental institutions have promoted innovation, driving the development of advanced burs. The regulatory framework in North America enforces strict quality standards, ensuring safe and reliable products. This has enhanced confidence among practitioners and patients, sustaining market momentum. Looking ahead, the focus on technology, research, and collaboration is expected to reinforce North America’s dominant position. The region is anticipated to remain a central hub for innovation and growth in the global Dental Burs Market.

Segmentation Analysis

In 2023, the Dental Burs Market recorded a strong preference for diamond burs, which captured more than 45.1% of the market share. Their durability and precision made them the leading choice for demanding dental procedures. Stainless steel burs also retained a significant presence due to their strength and resistance to corrosion. Meanwhile, carbide burs gained traction by offering efficiency and versatility, though they did not surpass diamond burs. These trends highlight a growing shift toward advanced materials that combine resilience and precision in dental applications.

From an application perspective, cavity preparation dominated the market, accounting for a 29.3% share in 2023. The segment’s leadership underscores the critical role of burs in ensuring accuracy and efficiency during dental cavity procedures. Oral surgery also maintained a strong presence, driven by the rising demand for surgical interventions. Implantology followed closely, fueled by increasing adoption of dental implants. Orthodontics contributed a significant share, reflecting evolving treatment needs. Collectively, the “Others” category demonstrated flexibility, showing the importance of burs in supporting diverse and emerging dental treatments.

In terms of end-use, hospitals emerged as the frontrunner in 2023, securing more than 48.1% of the market share. This dominance was driven by the large number of dental procedures carried out in hospital settings, where high precision is crucial. Dental clinics followed closely, holding a significant share due to their role in providing routine care and minor surgeries. The “Others” category, including ambulatory centers and specialty dental units, also showed meaningful growth. This segmentation emphasizes the importance of hospitals while also highlighting the consistent demand from clinics and alternative healthcare facilities.

Key Players Analysis

The Dental Burs Market is strongly influenced by leading manufacturers such as Dentsply Sirona, COLTENE Holding AG, SHOFU Inc., and MANI INC. These companies play a crucial role in shaping industry dynamics through innovative product offerings and strong brand presence. The market benefits from their consistent focus on research and development, which ensures reliable, durable, and precise dental burs. By addressing the needs of dental professionals worldwide, these players strengthen the market’s competitive structure and set new performance standards.

Dentsply Sirona remains a dominant participant in the Dental Burs Market due to its wide product portfolio and commitment to innovation. The company is recognized for delivering superior-quality products designed to support diverse dental procedures. Its strong emphasis on clinical efficiency and long-term reliability enhances its global presence. Meanwhile, COLTENE Holding AG adds competitive strength with advanced precision solutions. Its continuous investment in research and focus on product excellence reinforce its credibility and further boost overall industry growth.

SHOFU Inc. distinguishes itself in the market with innovative and user-friendly solutions tailored to professional needs. Its dedication to developing effective products supports its role as a key contributor to global demand. In addition to these major companies, several other participants bring diversity and expand the market offering. Their contributions provide tailored products for different dental applications, adding to market resilience. Collectively, the strong presence of established and emerging players ensures ongoing innovation, a dynamic environment, and an expanding product base for the Dental Burs Market.

Challenges

1) Stricter infection-control and reprocessing demands

Single-use burs follow a clear rule: one patient only, then dispose. This approach increases the number of units used and raises waste-handling costs. For reusable burs, strict reprocessing is required. Clinics must follow validated cleaning and sterilization steps exactly as the manufacturer instructs. Records of each process must be documented and monitored to ensure compliance. These steps reduce infection risks but add time and expense to clinic operations. The balance between patient safety, cost, and efficiency creates ongoing pressure for both dental practices and manufacturers of reusable dental burs.

2) EU MDR compliance and device identification

The EU Medical Device Regulation (MDR) sets strict requirements for dental burs. Every device must either have an individual Unique Device Identification (UDI) or be classified as single-use. Legacy products do not get exemptions. “Grandfathering” is not permitted, so all products must go through new conformity assessments. This adds work for manufacturers and creates more demand on notified bodies. Companies face higher costs for labeling, documentation, and testing. These rules increase transparency and patient safety, but they also raise administrative and compliance challenges for manufacturers who supply burs to the European market.

3) U.S. regulatory specifics for reprocessed burs

In the U.S., the FDA requires detailed validation data for reprocessed diamond-coated burs. This information must be included in 510(k) submissions. Such requirements increase testing time and add costs for reprocessors. Many Class I dental devices are exempt from 510(k). However, manufacturers must confirm the exemption rules and comply with relevant regulations. Ambiguities in these rules can create confusion, especially for smaller firms. As a result, administrative burdens rise, along with the risk of compliance errors. These regulatory complexities highlight the importance of careful planning and detailed documentation for U.S. dental bur manufacturers.

4) Standards and compatibility constraints

Dental burs must comply with ISO 1797 standards. These rules define dimensions and material requirements for bur shanks. Tolerances are strict to ensure safe use across dental handpieces. Any deviation risks poor fitting, breakage, or reduced safety. As a result, manufacturers face limits on design freedom and must maintain high levels of quality control. Strict monitoring is essential to ensure each bur performs reliably. These compatibility rules protect patient safety, but they also raise production costs and create barriers for innovation. This standardization keeps the market uniform but reduces flexibility in product development.

5) Raw-material exposure (tungsten carbide and diamond)

Tungsten carbide burs rely heavily on tungsten. This raw material faces risks from global trade regulations and export controls. Licensing changes or restrictions can disrupt the supply chain, lifting costs and extending lead times. The same applies to natural or synthetic diamonds used in cutting burs. Such fluctuations impact manufacturer margins and planning stability. Price increases also affect end-users, who may face higher procurement costs. Manufacturers must explore alternative sources, recycling strategies, or material innovations. These actions are needed to reduce dependency on volatile supply chains and protect business operations in the long term.

6) Environmental pressure from single-use waste

The shift to single-use burs supports infection control, but it also increases waste. Dental practices generate higher volumes of clinical waste, raising disposal costs. Environmental rules demand strict handling and treatment of this waste. At the same time, patients and regulators are calling for eco-friendly options. This pressure drives the need for sustainable product designs. Manufacturers must explore biodegradable materials, recycling systems, or other low-impact solutions. Balancing infection control with environmental responsibility is a major challenge. The industry is under pressure to combine safety, compliance, and sustainability in future product development.

7) Skill, training, and safety

Safe and effective bur use depends on correct training. Improper use can generate heat, reduce cutting efficiency, and increase risks for patients. Clinics must ensure that dental staff are trained in correct handling, cleaning, and sterilization. They also need to maintain stock of different shapes and grits to match clinical needs. These requirements add complexity to daily operations and costs for practices. Training is often reinforced by infection-control and instrument-processing guidelines. Without proper knowledge and skills, both patient safety and treatment outcomes can suffer. Continuous education remains essential for safe and efficient bur use.

Opportunities

1) Large and Persistent Clinical Need

Oral diseases continue to affect billions of people worldwide. High volumes of dental procedures, such as caries removal, crown preparation, bridge work, and root canal treatments, remain common. According to the WHO, oral diseases represent one of the most widespread health burdens. Older adults face higher levels of edentulism, which supports sustained demand for restorative and prosthetic procedures. The ongoing need for dental restorations ensures that burs remain essential across clinics and hospitals. This persistent clinical demand creates long-term market opportunities for dental bur manufacturers and suppliers. The stability of procedure volumes secures consistent consumption patterns globally.

2) Digital Dentistry and CAD/CAM Workflows

Digital workflows in dentistry are expanding rapidly. The adoption of CAD/CAM systems is driving demand for specialized milling burs made for zirconia, lithium disilicate, PMMA, and other materials. Both laboratory and chairside applications show increasing penetration, supported by strong evidence of clinical effectiveness. Recent surveys confirm growing interest from dentists in adopting chairside CAD/CAM solutions. The rising installed base of these systems ensures recurring use of milling burs, creating a steady supply-demand cycle. The clinical value of CAD/CAM restorations further supports this growth. This trend is expected to significantly accelerate bur consumption in the near future.

3) Premiumization via Compliance and Traceability

Regulations are reshaping procurement practices in dentistry. The Medical Device Regulation (MDR) requires unique device identification (UDI) and strict documentation. Vendors that supply sterile, traceable, and well-labeled packs benefit from compliance-driven differentiation. These features support premium pricing and increase trust among dental institutions. Hospitals and clinics prefer reliable suppliers with clear labeling and traceability, which also reduces risks during audits. Compliance therefore becomes a strong selling point and a long-term retention tool. By offering compliant solutions, vendors gain the ability to position products at higher price points and secure institutional contracts with reduced switching risks.

4) Product Differentiation Through Standards and Quality

International standards are increasingly important in dental procurement. Products aligned with ISO 1797 and FDA-recognized standards assure safety and compatibility across different handpieces and workflows. Procurement teams in hospitals and group practices prioritize these certifications when selecting suppliers. Vendors that demonstrate compliance with global standards can differentiate themselves in tenders and negotiations. This approach supports higher brand trust, longer-term partnerships, and improved contract opportunities. In a market where many products may appear similar, proven quality and documented compliance serve as effective tools for differentiation. This creates a sustainable competitive edge for leading dental bur manufacturers.

5) Single-Use Growth Niches

Single-use dental burs are gaining adoption in high-throughput settings. The Centers for Disease Control and Prevention (CDC) provides clear guidance supporting single-patient use in certain clinical contexts. Ambulatory surgery centers and busy dental chains value sterile, pre-packed burs that minimize infection risks. Vendors can capture this demand by offering specialized “procedure packs” with the required shapes bundled together. This simplifies inventory management and ensures compliance with infection control policies. The shift toward disposable instruments in selected niches generates recurring demand. For suppliers, single-use burs provide both volume opportunities and the ability to offer tailored product lines.

6) Supply-Chain Strategy as a Differentiator

Global material supply challenges create risks for dental bur manufacturers. Tungsten carbide, a key raw material, is exposed to export controls and trade disruptions. Suppliers that diversify sourcing, maintain reliable safety stocks, and provide transparent lead-time commitments gain a competitive advantage. Communication of material assurance and delivery reliability becomes a valuable differentiator in tender-based markets. Institutions favor suppliers that demonstrate resilience and continuity under volatile conditions. By building strong supply-chain strategies, companies not only manage risk but also strengthen long-term customer relationships. This strategic capability can become a decisive factor in procurement decisions worldwide.

7) Education and Workflow Tools

Beyond the product itself, value-added services create strong differentiation. Vendors can provide clinical usage guides, sterilization protocols, and evidence-based recommendations to optimize bur life. Digital tools such as bur-tracking apps help clinics monitor usage and reduce instrument failure. These services improve workflow efficiency and reduce replacement costs, aligning with infection-control rules and quality standards. Education also builds stronger customer relationships by supporting dentists in daily practice. By offering training and workflow solutions alongside products, suppliers move beyond commodity sales. This integrated approach strengthens brand loyalty and provides sustainable growth opportunities in the competitive dental burs market.

Conclusion

The global dental burs market shows steady and positive growth, supported by rising oral healthcare demand, aging populations, and the adoption of advanced dental technologies. Increasing focus on preventive care, digital workflows, and strict infection-control practices are shaping product preferences, particularly toward diamond and disposable burs. Although the industry faces challenges related to regulation, raw material supply, and environmental concerns, strong opportunities exist in premiumization, CAD/CAM workflows, and sustainable product innovation. With continuous investment in research, education, and partnerships, the market is expected to remain resilient. Overall, dental burs will continue to play a vital role in modern dentistry, ensuring safe, efficient, and high-quality patient care.

View More

Dental Implant Market || Dental Equipment Market || Dental Lasers Market || Dental Prosthetics Market || Dental Caries Detectors Market || Dental Crowns And Bridges Market || Dental Biomaterial Market || Dental Services Market || Dental X-ray Market || Dental Turbines Market || Dental Loupe Market

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)