Table of Contents

Overview

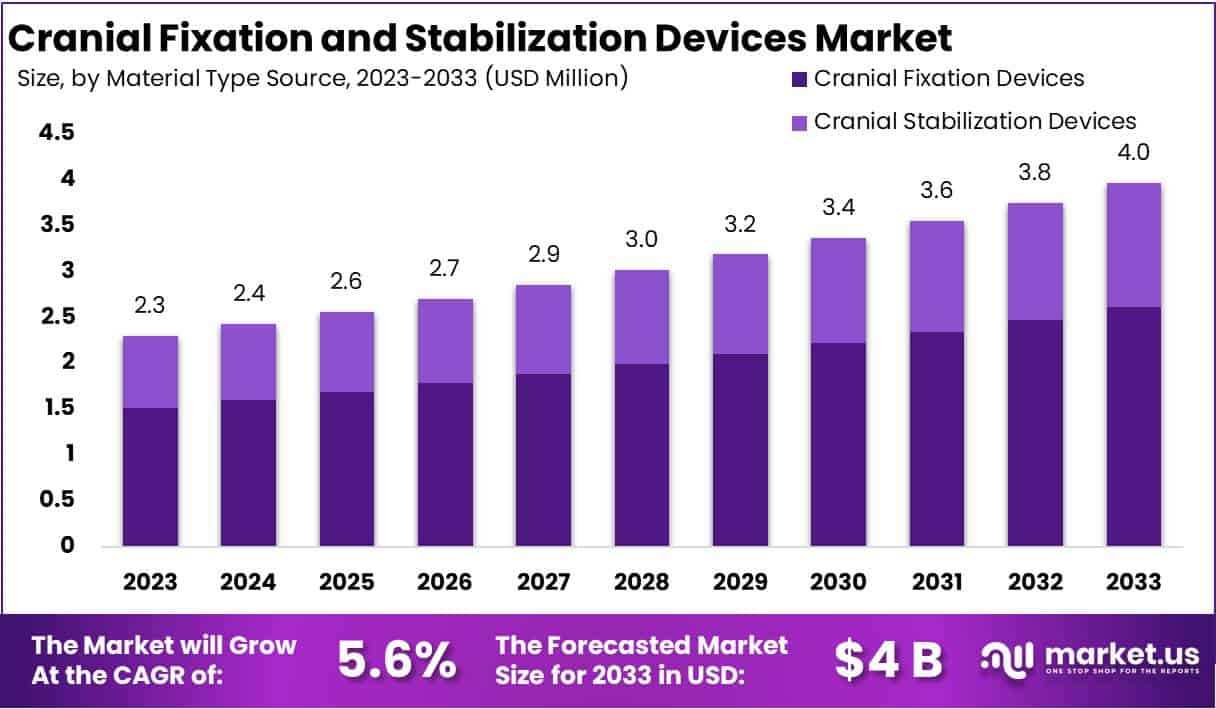

The Global Cranial Fixation and Stabilization Devices Market is projected to reach USD 4 billion by 2033 from USD 2.3 billion in 2023, reflecting a CAGR of 5.6% between 2024 and 2033. Growth is driven by the increasing burden of head injuries and neurological disorders worldwide. According to the WHO, road traffic injuries cause about 1.19 million deaths annually and remain the leading cause of death among people aged 5–29. These injuries, especially in low- and middle-income countries, significantly raise the need for cranial fixation systems following trauma surgeries.

The rising prevalence of neurological disorders further sustains market demand. More than one-third of the global population is affected by neurological conditions such as stroke, epilepsy, and brain tumors. These disorders often require neurosurgical interventions, where cranial fixation systems are essential for skull closure and stability. Growing incidence rates and improved diagnosis continue to expand the surgical base for these devices worldwide.

Oncology-related procedures add consistent demand for cranial fixation and stabilization systems. Cancer surveillance data highlight measurable rates of brain and nervous-system tumors among both adults and children. Surgical resections of these tumors typically require cranial plates and screws to ensure secure closure. Consequently, ongoing oncology caseloads across major health systems continue to support recurring use of these medical devices.

The ageing global population is another major growth driver. UN and WHO projections show that older adults represent a rapidly expanding demographic. Ageing increases susceptibility to falls, trauma, and neurological diseases, all of which contribute to higher neurosurgical volumes. This demographic shift directly enhances the utilization of cranial fixation devices in both developed and emerging healthcare systems.

Additionally, expanding surgical capacity and technological innovation reinforce market growth. Emerging economies are investing heavily in healthcare infrastructure, surgical workforce, and neurosurgical training. Alongside this, advanced materials such as titanium and bio-resorbable polymers are improving surgical outcomes. Regulatory frameworks like the U.S. FDA Class II standards and the EU MDR 2017/745 ensure safety, performance, and traceability. Together, these factors create a favorable environment for steady global adoption of cranial fixation and stabilization devices.

Key Takeaways

- The market is anticipated to reach USD 4 billion by 2033, expanding at a 5.6% CAGR from USD 2.3 billion in 2023.

- Cranial Fixation Devices accounted for over two-thirds of the market share in 2023, serving as essential tools for skull stabilization procedures.

- Resorbable Fixation Systems captured 56% of the market in 2023, offering dissolvable solutions that eliminate secondary surgeries, particularly beneficial in pediatric treatments.

- Hospitals represented 62% of market demand in 2023, while Ambulatory Surgical Centers (ASCs) exhibited a consistent upward growth trend.

- The market expansion is driven by rising neurological disorders and traumatic brain injuries, intensified by aging populations and increasing road accidents globally.

- High treatment and device costs restrict market penetration in developing nations, emphasizing disparities in healthcare affordability and access.

- Innovations in biocompatible materials and 3D printing technologies are enabling custom implant designs, improving precision and post-surgical recovery outcomes.

- The growing preference for Minimally Invasive Surgeries (MIS) enhances demand, reducing hospital stays, infection risks, and overall recovery time.

- North America led the global market with 42% share in 2023, followed by Europe, Asia-Pacific, Latin America, and the Middle East & Africa.

Regional Analysis

In 2023, North America dominated the Cranial Fixation and Stabilization Devices Market, accounting for over 42% of the global share, valued at USD 0.9 billion. The growth in this region was supported by advanced healthcare infrastructure, high healthcare spending, and strong regulatory backing for medical device innovation. The United States played a central role due to its large patient base, extensive network of neurosurgical centers, and world-class medical research institutions that fostered rapid technological advancement and adoption.

Europe maintained a significant position in the global market, driven by countries such as Germany, France, and the United Kingdom. The region benefited from a mature healthcare system, supportive reimbursement frameworks, and an increasing elderly population that required more neurosurgical procedures. The integration of advanced surgical technologies and consistent government focus on healthcare quality further strengthened Europe’s market performance.

Asia-Pacific, though holding a smaller share, showed the fastest growth rate due to expanding healthcare facilities and rising awareness of neurosurgical treatments in China, India, and Japan. Latin America and the Middle East & Africa recorded moderate yet steady growth. Their progress was supported by improving healthcare access and rising disposable income levels. However, limited infrastructure and complex regulatory environments continued to restrict full market potential in these regions.

Segmentation Analysis

Product Analysis

In 2023, the Cranial Fixation Devices segment dominated the Cranial Fixation and Stabilization Devices Market, capturing over two-thirds of the market share. This dominance is driven by their critical role in neurosurgical procedures, ensuring skull stability after trauma or surgery. The product range includes screws, meshes, and other fixation components tailored for different cranial procedures. Among these, screws led market growth due to their reliability and ease of application, while meshes contributed notably by providing coverage for larger cranial defects. On the other hand, the Cranial Stabilization Devices segment, comprising skull clamps and horseshoe headrests, held a smaller share but remained essential for maintaining head stability and precise positioning during surgery. Market growth was further supported by technological innovations, rising neurological conditions, and increasing cases of trauma requiring neurosurgical interventions.

Material Type Analysis

The Resorbable Fixation segment held a leading position in 2023, accounting for over 56% of the material type market share. These systems dissolve gradually within the body, eliminating the need for a secondary removal surgery and are particularly preferred in pediatric neurosurgery. Their growing adoption is attributed to patient-friendly design and reduced long-term complications. Nonresorbable Fixation Systems continue to maintain strong demand due to their durability and superior stability, especially for adult and long-term cases. However, the need for removal surgery limits their appeal. The market is evolving with ongoing research focused on improving the safety and performance of resorbable materials, signaling a shift toward these advanced, biocompatible systems. The overall market growth is supported by increasing neurological cases and expanding access to advanced neurosurgical care.

End-User Analysis

In 2023, hospitals dominated the end-user landscape, securing over 62% of the market share. This leadership reflects their central role in performing complex neurosurgeries and trauma management, supported by advanced infrastructure and skilled multidisciplinary teams. Hospitals remain the primary purchasers of cranial fixation and stabilization devices due to their high surgical volumes. Meanwhile, Ambulatory Surgical Centers (ASCs), though holding a smaller share, are gaining momentum with the rise of minimally invasive techniques and demand for cost-effective outpatient neurosurgical care. The segment’s growth is influenced by factors such as healthcare infrastructure, reimbursement systems, and patient preferences. Overall, while hospitals continue to drive the market, ASCs are expected to expand their role in the coming years due to efficiency and convenience advantages.

Key Players Analysis

The Cranial Fixation and Stabilization Devices Market is characterized by strong competition among leading medical technology firms. Integra LifeSciences Corporation leads the market through its extensive neurosurgical product line. Its devices are known for reliability, precision, and comprehensive application across trauma and reconstruction cases. Medtronic Plc follows closely with an innovative portfolio emphasizing surgical accuracy and patient safety. The company’s strong research foundation and commitment to advancing neurosurgical practices have established its dominant position in the global market.

Depuy Synthes, a subsidiary of Johnson & Johnson, plays a crucial role in shaping the cranial fixation segment. Its devices are widely recognized for high quality and innovation, addressing diverse neurosurgical needs, from cranial reconstruction to fracture management. The brand’s global presence and trust among surgeons underscore its contribution to market growth. Similarly, B. Braun SE has made significant advancements with patient-centric designs and safety-focused implant systems, improving surgical outcomes and aligning with rising healthcare quality standards.

In addition, Stryker Corporation and Zimmer Biomet have expanded their market reach through advanced product innovations and strong clinical collaborations. Stryker’s fixation systems are valued for precision engineering, while Zimmer Biomet emphasizes biomechanical compatibility and patient recovery optimization. These companies collectively enhance the competitive landscape, driving the development of next-generation cranial fixation technologies aimed at minimizing complications and improving surgical efficiency.

Moreover, KLS Martin and other emerging manufacturers contribute to technological diversification within the market. Their participation enhances accessibility to advanced surgical tools across regions. Through continuous product development, strategic collaborations, and regional expansion, these firms collectively strengthen the global cranial fixation and stabilization devices ecosystem. The market, driven by innovation and clinical demand, is expected to experience sustained growth supported by ongoing technological and procedural advancements in neurosurgery.

Challenges

Infections and Wound Complications

Cranioplasty for large skull defects remains at risk of infection. Infection rates depend on the type of material and patient condition. Studies show mixed results. Some report fewer infections with PEEK compared to titanium or PMMA. Others find no significant difference. This inconsistency makes it hard to create a standard guideline. Infections can delay healing, increase hospital stays, and raise costs. Proper surgical technique, sterilization, and postoperative care are vital. Consistent data and multicenter studies are needed to define the safest material and reduce infection-related complications.

Complications from Skull Clamps and Head-Holder Pins

Mayfield-type skull clamps are crucial for rigid head stabilization during neurosurgery. However, they may sometimes cause injuries. Complications include scalp lacerations, vascular injury, skull fractures, or even epidural hematoma. These events are rare but can be severe. Most cases result from improper placement or excessive pressure. Careful technique, proper pin torque, and patient-specific adjustments can prevent them. Regular inspection of the clamp system and staff training also reduce risk. Prevention remains the best approach since these injuries are mostly avoidable with strict procedural discipline.

Imaging Artifacts and Follow-Up Limitations

Metal implants such as titanium plates or meshes often create imaging artifacts. These artifacts interfere with CT or MRI scans, complicating follow-up after trauma or cancer surgery. Radiolucent polymers like PEEK reduce this issue but come with trade-offs. They may have lower mechanical strength or higher cost. Selecting the right material depends on the clinical need, patient condition, and imaging requirements. Continued innovation in radiolucent materials could improve long-term monitoring. However, achieving a balance between clarity, durability, and affordability remains challenging.

Variation in Material Performance and Evidence Quality

Performance varies widely across materials such as titanium, PEEK, PMMA, and bioresorbables. Direct comparison studies are limited and inconsistent. Existing meta-analyses often show conflicting results. This makes it difficult to establish firm clinical guidelines or procurement standards. Many hospitals rely on surgeon preference and local experience rather than clear evidence. Improving study design and standardizing outcome reporting are essential. Better comparative trials will help identify optimal materials for safety, integration, and cost efficiency, leading to more consistent global practices.

Regulatory Stringency and Compliance Load

Regulatory requirements for cranial fixation devices are becoming stricter. In the European Union, most implants are classified as Class IIb under the Medical Device Regulation (MDR). This increases demands for clinical evidence and post-market surveillance. In the United States, many systems gain approval through the FDA 510(k) pathway, but compliance expectations remain high. Manufacturers must ensure traceability, quality control, and ongoing vigilance. Meeting these standards adds time and cost to development. Yet, strict oversight enhances patient safety and product reliability across healthcare systems.

Sterilization, Reprocessing, and OR Workflow

Cranial fixation systems often include both reusable and single-use components. Reusable clamps and pins must undergo proper cleaning and sterilization. Any mistake in reprocessing can lead to surgical site infections or device failure. Maintaining traceability and following strict protocols are essential. Surgical teams must manage mixed sets efficiently to avoid workflow delays. Consistent staff training and automated tracking systems can reduce human error. Strong infection-control practices not only improve patient outcomes but also help hospitals avoid costly downtime due to reprocessing errors.

Cost Pressure and Access Gaps

Healthcare facilities face ongoing pressure to lower implant costs and speed up instrument turnaround. Advanced materials like PEEK and titanium increase costs, limiting access in low- and middle-income regions. These countries often experience high rates of traumatic brain injury but lack adequate surgical resources. Cost-effective alternatives and local manufacturing could help bridge this gap. Partnerships between device makers and public health systems are essential. Addressing affordability and equitable access remains a key step toward improving global neurosurgical care outcomes.

Opportunities

Radiolucent and Advanced Polymers

The rise of PEEK and similar polymers is transforming cranial fixation. These materials allow clear imaging and maintain mechanical stability during long-term use. They can also be shaped precisely for patient needs. New porous and surface-modified versions are being developed to enhance bone integration and soft-tissue compatibility. Their biocompatibility and strength make them ideal for implants that need both durability and radiolucency. Manufacturers focusing on innovation in polymer processing and surface treatment can gain a competitive advantage. The growing demand for non-metallic and MRI-compatible implants continues to strengthen this opportunity.

Patient-Specific, 3D-Printed Implants (PSIs)

Patient-specific implants created through digital planning and 3D printing are improving surgical outcomes. These implants provide a better anatomical fit, improved appearance, and reduced operation time. In industrial setups, production can take around five days, while hospital-based printing can be done within hours. Several clinical studies confirm their safety, cost-efficiency, and customization benefits. Adoption is expected to increase as digital surgical workflows become more common. The integration of 3D imaging, modeling, and additive manufacturing supports faster recovery and reduces intraoperative adjustments, creating strong growth potential for PSI developers and healthcare providers.

Process Innovation: Point-of-Care (POC) Printing

Point-of-care (POC) printing allows hospitals to produce implants on-site, reducing delivery time and logistics complexity. This approach can streamline operations when combined with strict quality systems and regulatory compliance. Early studies show success in using POC workflows for both degradable and permanent implants. Hospitals benefit from faster patient turnaround and lower inventory requirements. As digital manufacturing regulations mature, more healthcare systems are expected to adopt this model. Collaboration between hospitals, engineers, and regulators will be crucial to ensure safe, cost-effective, and scalable implementation of point-of-care implant production.

Infection-Risk Mitigation Technologies

Reducing infection risk remains a key focus in cranial surgery. Advances in antimicrobial coatings, optimized porosity, and integrated drainage systems are driving innovation. Products designed with soft-tissue-friendly surfaces and bacteria-resistant materials are gaining interest. Evidence comparing different infection-control technologies is still emerging, creating opportunities for differentiation. Manufacturers that invest in robust clinical validation can build stronger market credibility. As hospitals prioritize patient safety and long-term outcomes, devices offering superior infection prevention will hold a distinct advantage in competitive tenders and procurement processes.

Safer Stabilization Systems

Improvements in stabilization devices such as skull clamps are enhancing patient safety. Modern systems feature refined pin designs, better pressure control, and force-feedback mechanisms. Pediatric-specific adapters and standardized safety checklists are helping reduce the risk of complications. Training modules and digital monitoring systems are also improving procedural accuracy. Hospitals focused on zero-harm initiatives are likely to prefer systems with advanced safety features. This shift encourages manufacturers to invest in ergonomic, data-driven, and training-supported stabilization solutions for both adult and pediatric care.

Growth from Trauma Care and Neuro-Oncology

Trauma care and neuro-oncology remain major demand drivers for cranial fixation devices. Road traffic accidents continue to cause high rates of traumatic brain injury (TBI), especially in low- and middle-income countries. As global trauma systems improve and neurosurgical capacity expands, demand for fixation devices is projected to rise steadily. The increase in neuro-oncology procedures and reconstructive surgeries also contributes to sustained growth. Companies investing in cost-efficient, adaptable solutions for emerging markets will find strong opportunities in public health-driven procurement and trauma infrastructure expansion programs.

Value-Based and Bundled Offerings

Hospitals increasingly prefer value-based packages that streamline surgical workflows. Pre-sterilized low-profile plates, torque-limited drivers, and guided drilling kits reduce operation time and error risk. Single-vendor instrument sets help standardize quality and cut costs. Combining implants with digital planning, PSI services, and professional training adds value beyond hardware. This integrated approach supports hospitals’ cost-containment goals and encourages brand loyalty. Vendors offering complete, ready-to-use surgical solutions are well positioned to gain long-term contracts in both public and private healthcare systems.

Conclusion

The Cranial Fixation and Stabilization Devices Market is expected to grow steadily, supported by rising neurological disorders, head injuries, and an aging population. Continuous innovation in biocompatible materials, 3D printing, and infection-control technologies is enhancing surgical outcomes and safety. Hospitals remain the primary users, while Ambulatory Surgical Centers are gaining importance due to minimally invasive procedures. Although high costs and regulatory demands present challenges, expanding access to advanced neurosurgical care and the adoption of patient-specific implants will sustain market growth. Overall, the market is positioned for consistent progress, driven by technological advancements and increasing global healthcare investments.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)