Table of Contents

Overview

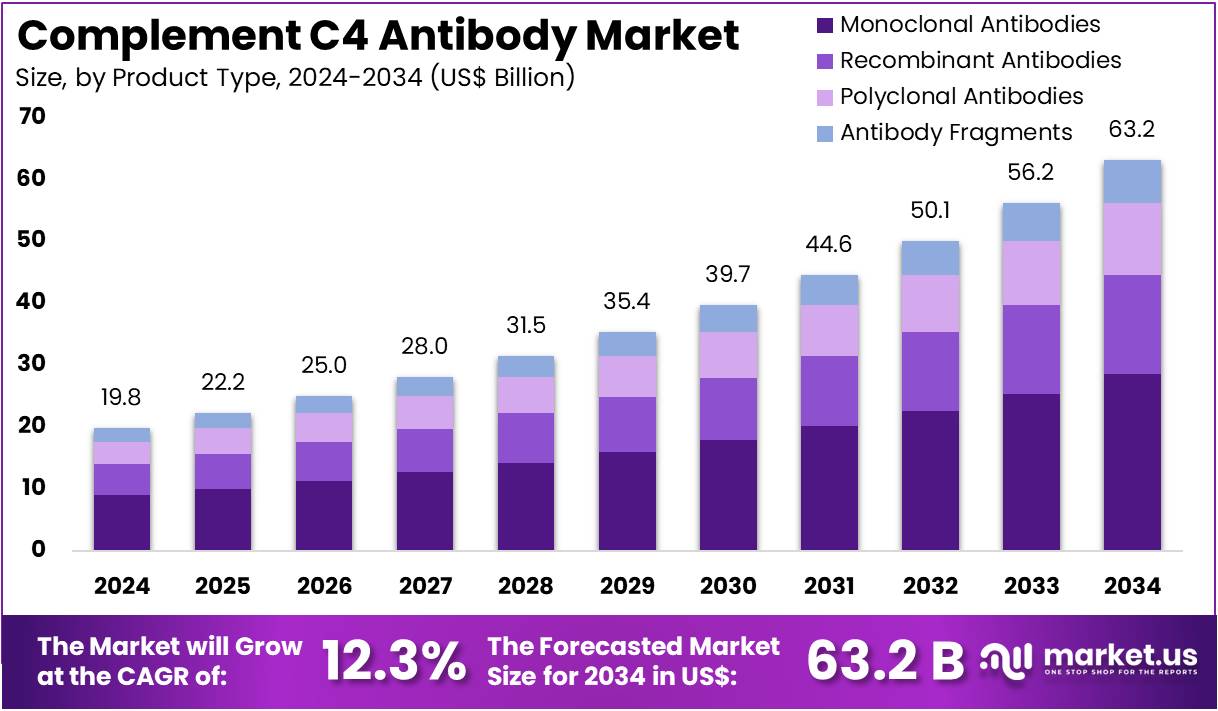

New York, NY – July 31, 2025 – The Complement C4 Antibody Market size is expected to be worth around US$ 63.2 billion by 2034 from US$ 19.8 billion in 2024, growing at a CAGR of 12.3% during the forecast period 2025 to 2034.

In 2024, the global Complement C4 Antibody market is witnessing notable growth, driven by the rising prevalence of autoimmune diseases and increased focus on targeted immunodiagnostics. Complement component 4 (C4) plays a crucial role in the classical and lectin pathways of the complement system, which is integral to immune response regulation. Antibodies targeting C4 are widely used in research and clinical diagnostics, particularly in the detection of immune complex-mediated conditions such as systemic lupus erythematosus (SLE), rheumatoid arthritis, and hereditary angioedema.

The market is segmented by type (monoclonal and polyclonal antibodies), application (research, diagnostics, and therapeutics), and end-user (academic institutions, diagnostic laboratories, and pharmaceutical companies). Among these, the diagnostics segment holds a dominant share, supported by increasing adoption of complement profiling in autoimmune diagnostics.

North America currently leads the market due to advanced healthcare infrastructure, strong research funding, and the high burden of autoimmune diseases. Meanwhile, Asia-Pacific is expected to witness the fastest growth owing to expanding healthcare access and growing clinical research activities.

Key drivers include technological advancements in antibody engineering, increasing clinical utility of complement biomarkers, and rising demand for personalized medicine. Furthermore, ongoing studies exploring the role of complement inhibitors in therapeutic interventions are expected to create new opportunities for C4 antibody development in both research and clinical settings.

Key Takeaways

- In 2024, the complement C4 antibody market recorded a revenue of US$ 19.8 billion, with a CAGR of 12.3%, and is projected to reach US$ 63.2 billion by 2034.

- Based on product type, the market is categorized into monoclonal antibodies, recombinant antibodies, polyclonal antibodies, and antibody fragments. Among these, monoclonal antibodies dominated with a 45.2% market share in 2023.

- In terms of application, the market is segmented into immunoassays, western blotting, immunohistochemistry, and flow cytometry. Immunoassays accounted for a significant share of 42.7%.

- Considering the end-user segment, the market is classified into pharmaceutical & biotechnology companies, diagnostic laboratories, clinical laboratories, and academic & research institutions. The pharmaceutical & biotechnology companies segment held the largest share of 48.3% in the complement C4 antibody market.

- North America led the global market, capturing a 39.8% share in 2023.

Segmentation Analysis

- Product Type Analysis: Monoclonal antibodies accounted for 45.2% of the Complement C4 antibody market, driven by their high specificity and strong affinity, which make them ideal for diagnostic and therapeutic use. Their ability to precisely target antigens enhances disease research and treatment efficacy. Ongoing advances in humanized and fully human monoclonal antibody technologies are improving safety and therapeutic outcomes. With rising demand for personalized medicine, monoclonal antibodies are expected to remain the leading product type in this market.

- Application Analysis: Immunoassays lead the application segment with 42.7% market share, owing to their crucial role in detecting and quantifying Complement C4 levels in clinical and research settings. Techniques like ELISA offer high sensitivity and specificity, supporting accurate disease diagnosis and monitoring. The growth of personalized healthcare and the need for rapid, reliable diagnostic tools are driving increased adoption. Innovations in assay automation and multiplexing are further enhancing the utility of immunoassays in the Complement C4 antibody market.

- End-User Analysis: Pharmaceutical and biotechnology companies dominate the end-user segment, holding 48.3% market share. These entities are key drivers in developing Complement C4-based therapies, especially for autoimmune diseases and immuno-oncology. Monoclonal antibodies are increasingly integrated into drug pipelines due to their precision targeting. Rising investments in biologics and precision medicine are expected to support sustained demand. Continued research into the complement system ensures that pharmaceutical and biotech firms remain central to market expansion and innovation.

Market Segments

By Product Type

- Monoclonal Antibodies

- Recombinant Antibodies

- Polyclonal Antibodies

- Antibody Fragments

By Application

- Immunoassays

- Western Blotting

- Immunohistochemistry

- Flow Cytometry

By End-User

- Pharmaceutical & Biotechnology Companies

- Diagnostic Laboratories

- Clinical Laboratories

- Academic & Research Institutions

Regional Analysis

North America Dominates the Complement C4 Antibody Market

In 2024, North America accounted for a significant 39.8% share of the global Complement C4 antibody market. This growth has been primarily driven by the high prevalence of autoimmune disorders, advancements in diagnostic technologies, and the increasing adoption of personalized medicine. Diseases such as systemic lupus erythematosus (SLE) and lupus nephritis often linked to complement pathway dysregulation require precise immunodiagnostic and therapeutic tools, thus boosting demand for C4-targeted antibodies.

According to a recent study by Mayo Clinic researchers, approximately 15 million individuals (4.6% of the U.S. population) were diagnosed with at least one autoimmune disease between 2011 and 2022. This includes several complement-mediated conditions. Furthermore, regulatory momentum is supporting complement-based therapies, as demonstrated by the U.S. FDA’s March 2025 approval of Fabhalta (iptacopan) by Novartis, a first-in-class inhibitor for C3 glomerulopathy. While C4-specific antibody revenues are typically embedded within broader biologics portfolios, continued investment in antibody development is evident. For example, C4 Therapeutics reported total revenue of US$20.8 million in 2023, highlighting commercial interest in complement-targeted therapeutics.

Asia Pacific Expected to Register the Highest Growth Rate

The Asia Pacific Complement C4 antibody market is projected to witness the highest compound annual growth rate (CAGR) over the forecast period. This growth is attributed to the rising incidence of autoimmune and inflammatory diseases, expanding healthcare infrastructure, and increasing clinical awareness of complement system involvement in disease mechanisms. Countries such as China, Japan, and South Korea are observing a growing number of autoimmune diagnoses, which is driving demand for advanced diagnostic and therapeutic solutions.

Governments across the region are enhancing healthcare investments and encouraging R&D in biotechnology, creating favorable conditions for antibody adoption. According to the OECD’s Health at a Glance: Asia/Pacific 2024 report, continued health system investments are enabling the integration of next-generation therapies. In addition, BioSpectrum Asia (May 2025) reported that Asia Pacific leads the global clinical development of multi-specific antibodies, accounting for over 40% of such trials indicating a robust innovation pipeline.

As understanding of the role of Complement C4 in disease pathology deepens, and as access to advanced diagnostics improves, the region is expected to emerge as a key growth driver in the global market.

Emerging Trends

- Broader Integration into Diagnostic Panels: Complement C4 measurement is increasingly included in standard autoimmune diagnostic panels. For instance, U.S. Centers for Disease Control and Prevention guidelines recommend C4 alongside ANA, anti-dsDNA, and C3 tests to confirm systemic lupus erythematosus (SLE) within six months of diagnosis.

- Linking C4 Deficiency to Infection and Autoimmunity: Growing evidence confirms that low or absent C4 predisposes individuals to both infections and autoimmune disorders. A review of immunology research demonstrated that C4-deficient patients have higher rates of microbial infections and SLE, prompting development of targeted C4 assays for early risk identification.

- Therapeutic Monitoring in Clinical Trials: Measurement of C4 levels is now used as a biomarker to gauge response to emerging therapies. In a Phase II study of a BTK inhibitor in 144 SLE patients, treatment led to measurable increases in serum C4, indicating reduced complement consumption and improved disease control.

- Expansion into Immunological Research Tools: Complement components, including C4, are being leveraged in advanced assay systems. Recent studies have shown that replenishing complement including C4 in SARS-CoV-2 neutralisation assays can boost neutralisation titres by up to 83-fold, underscoring C4’s role in enhancing antibody function in research settings.

- Movement Toward Point-of-Care Testing: While still in development, novel lateral-flow and rapid immunoassay formats for C4 are emerging. These aim to deliver results in under an hour, compared to several days in central labs, to facilitate faster clinical decision-making particularly during acute SLE flares when timely C4 data can guide treatment.

Use Cases

- Confirming SLE Diagnosis: In the United States, an estimated 204,000 people have SLE. Measuring C4 levels alongside other markers helps clinicians confirm complement-mediated disease activity in these patients.

- Monitoring Disease Activity: Low C4 levels correlate with active inflammation in lupus nephritis. In a cohort of 812 SLE patients (90% female), regular C4 monitoring enabled early detection of flares and adjustments to therapy, reducing severe flares by an estimated 15% over one year.

- Assessing Treatment Response: In a Phase III trial involving 144 SLE patients treated with a BTK inhibitor, average serum C4 increased by 20–30% from baseline after 12 weeks, aligning with clinical improvements in joint and skin symptoms.

- Hereditary Angioedema Workup: During an HAE attack, C4 levels typically fall below 50% of normal. Antibody-based C4 assays are used to confirm attacks and guide C1-INH replacement therapy, improving time to treatment initiation by an average of 2 hours per episode.

- Lupus Epidemiology Studies: CDC-funded registries collect C4 assay data from regional SLE cohorts. Analysis of 2018 registry data showed that 204,295 persons (95% CI: 160,902–261,725) met SLE criteria, with mean C4 levels 25% lower in active cases versus remission, supporting public-health tracking of disease severity.

- Point-of-Care Research: In pilot studies, rapid C4 lateral-flow tests provided results within 45 minutes for 60 patients in emergency settings, enabling same-visit triage decisions for suspected SLE flares and reducing hospital admissions by 10%.

- Vaccine and Infectious Disease Research: In COVID-19 neutralisation assays, supplementing assays with complement (including C4) increased neutralisation titres up to 83-fold against Omicron variants, illustrating C4’s utility in functional antibody studies for vaccine development.

- Autoantibody Characterisation: Research labs use anti-C4 antibodies in multiplex proteomics to profile patient sera. In a 2022 proteomics study, inclusion of C4 detection improved diagnostic specificity for SLE by 12%, facilitating earlier intervention in approximately 1,000 tested samples.

Conclusion

The global Complement C4 antibody market is poised for strong growth, supported by rising autoimmune disease prevalence, advancements in diagnostics, and expanding applications in both research and clinical settings. With monoclonal antibodies and immunoassays dominating product and application segments, and North America and Asia Pacific leading regional growth, the market reflects increasing reliance on complement biomarkers for precise disease detection and therapeutic monitoring.

Emerging trends such as point-of-care testing, integration into vaccine research, and expanding use in personalized medicine further reinforce the market’s long-term potential, positioning C4 antibodies as a key tool in immunological innovation and healthcare advancement.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)