Table of Contents

Overview

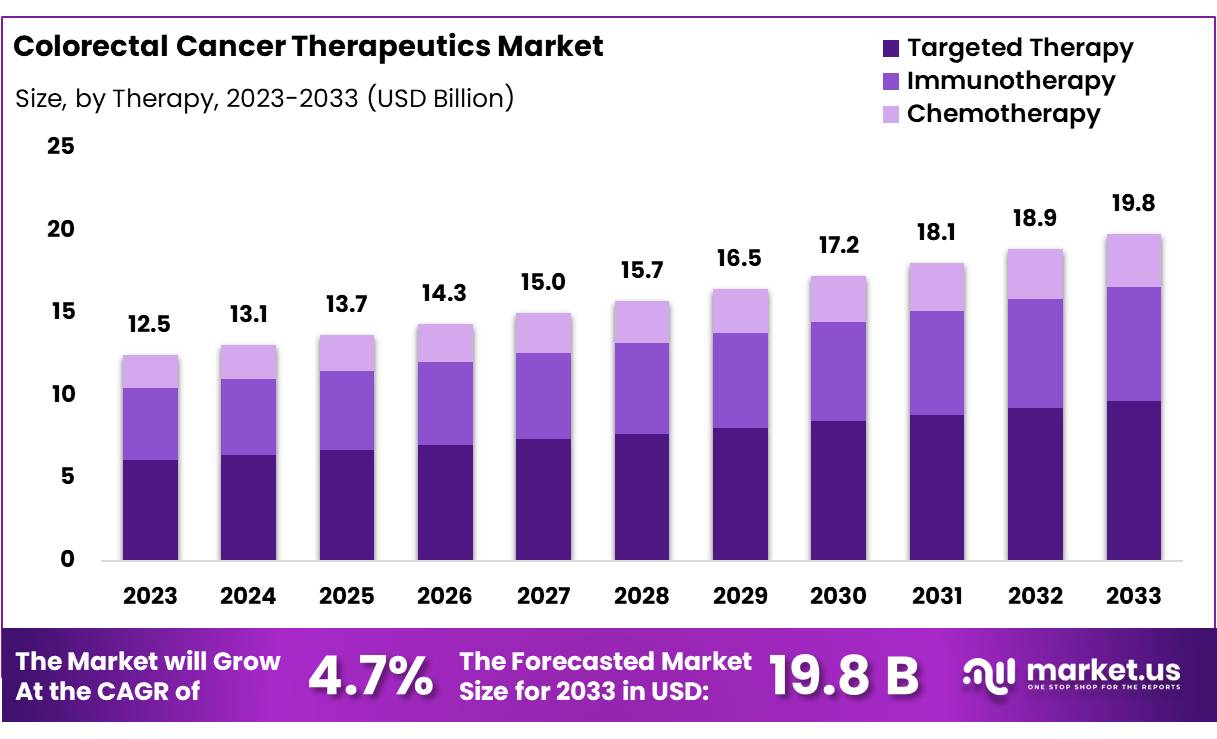

New York, NY – Oct 29, 2025 – Global Colorectal Cancer Therapeutics Market size is expected to be worth around US$ 19.8 Billion by 2033 from US$ 13.1 Billion in 2024, growing at a CAGR of 4.7% during the forecast period from 2025 to 2033. In 2023, North America led the market, achieving over 40% share with a revenue of US$ 5.0 Billion.

The global colorectal cancer therapeutics market is experiencing steady growth, driven by a rising disease burden and advancements in targeted therapies. Colorectal cancer remains one of the leading causes of cancer-related deaths worldwide, and increasing diagnosis rates have resulted in higher demand for effective treatment options. The adoption of precision oncology is expanding, and the development of biologics, immunotherapies, and combination therapies is expected to strengthen market performance in the coming years.

The growth of the market can be attributed to continuous improvements in drug discovery and the approval of novel therapeutics that enhance patient survival outcomes. Increased awareness campaigns and government initiatives supporting early screening are contributing to the expansion of the patient pool eligible for treatment. In addition, the rising geriatric population is expected to be a major factor supporting market growth.

Pharmaceutical companies are investing heavily in research and clinical trials to introduce more effective and safer therapies targeting molecular pathways. Immunotherapies, including checkpoint inhibitors, have gained significant acceptance due to their ability to offer durable responses in advanced-stage patients. The shift toward personalized medicine is creating new opportunities for market players, particularly in biomarker-based drug development.

North America continues to dominate the market due to favorable reimbursement policies and strong healthcare infrastructure. However, Asia Pacific is expected to record the fastest growth, supported by improving access to cancer care services. The market outlook remains positive, with a strong focus on innovation and improved treatment accessibility worldwide.

Key Takeaways

- Global Colorectal Cancer Therapeutics Market size is expected to be worth around US$ 19.8 Billion by 2033 from US$ 13.1 Billion in 2024, growing at a CAGR of 4.7% during the forecast period from 2025 to 2033.

- In terms of therapy type, the Immunotherapy segment accounted for 49% of the global revenue share in 2023, maintaining its position as the leading treatment category.

- Based on treatment provider segmentation, hospitals represented the dominant end-user group, contributing to 45% of the total market revenue in 2023.

- North America remained the largest regional market, holding more than 40% of the global revenue share in 2023, supported by well-established healthcare infrastructure and high treatment adoption.

Regional Analysis

North America accounted for approximately 40% of the global colorectal cancer therapeutics market, supported by the high prevalence of colorectal cancer in the region. The United States represents the major contributor, where lifestyle-related risk factors, including rising alcohol consumption, unhealthy dietary patterns, and reduced physical activity, continue to drive colorectal cancer incidence.

The region benefits from a well-established healthcare infrastructure that enables extensive access to advanced treatment modalities such as immunotherapy, targeted therapies, and precision medicine. The availability of these premium therapeutics, combined with comparatively higher healthcare expenditure, supports increased treatment adoption and market revenue generation.

Further, strong patient awareness and the implementation of comprehensive screening programs facilitate early disease detection, resulting in improved clinical outcomes and sustained demand for effective treatment solutions. As healthcare investments and innovation continue to progress, North America is expected to retain its leading position in the global colorectal cancer therapeutics market throughout the forecast period.

Emerging Trends

- Neoadjuvant Immunotherapy for MSI-H/dMMR Tumors

The adoption of checkpoint inhibitors before surgery is expanding, particularly for tumors with high microsatellite instability (MSI-H) or mismatch repair deficiency (dMMR). Combinations such as nivolumab with ipilimumab are demonstrating strong tumor reduction, positioning this approach as a preferred initial therapy for advanced MSI-H colorectal cancers. - Precision-Targeted Therapy for BRAF-Mutant mCRC

The approval of encorafenib combined with cetuximab and the FOLFOX regimen for BRAF V600E-mutated metastatic colorectal cancer marks a major advancement. This mutation accounts for nearly 5% of colorectal cancer cases, and the therapy is expected to significantly enhance outcomes in this patient group. - KRAS G12C Inhibition for Previously Treated Patients

The regulatory approval of sotorasib plus panitumumab provides a new option for KRAS G12C-mutated metastatic colorectal cancer, a mutation present in approximately 4% of cases. This therapy offers clinical benefit for patients who have exhausted standard chemotherapy treatments. - Liquid Biopsy–Driven Treatment Decisions

Research into circulating tumor DNA (ctDNA) is accelerating to determine postoperative chemotherapy needs in stage II colon cancer patients. ctDNA testing can detect minimal residual disease by identifying tumor-derived DNA fragments that make up less than 1% of total cell-free DNA. - Blood-Based Early Detection Screening

Non-invasive screening options are improving, with the FDA approving the Shield blood test for average-risk individuals in 2024. Clinical findings among nearly 8,000 participants demonstrated a detection rate exceeding 83% for colorectal cancers confirmed through colonoscopy.

Frequently Asked Questions on Colorectal Cancer Therapeutics

- What is driving the growth of the colorectal cancer therapeutics market?

Market growth is driven by rising colorectal cancer incidence, advancements in targeted and immune-based drugs, improved diagnostic screening programs, and increasing healthcare expenditure. Expanding access to innovative treatments continues to strengthen revenue growth worldwide. - Which treatment type dominates the colorectal cancer therapeutics market?

Immunotherapy currently leads the market due to its effectiveness in advanced cancer stages and its ability to produce long-lasting responses. The adoption of checkpoint inhibitors and personalized immuno-oncology drugs continues to increase rapidly. - Why is North America the largest regional market?

North America holds a major revenue share due to high disease prevalence, early diagnosis programs, strong reimbursement systems, and widespread accessibility to premium therapies. Continuous healthcare advancements support sustained market dominance. - What role does personalized medicine play in colorectal cancer treatment?

Personalized medicine enables therapies to be matched to specific genetic markers in patients. This approach improves treatment accuracy, reduces unwanted effects, and offers better outcomes, especially for advanced or metastatic colorectal cancer cases. - Which key challenges affect the market?

High treatment costs, limited access in developing regions, and side effects from certain advanced therapies remain challenges. Additionally, drug resistance and late diagnosis rates create unmet needs that the industry continues to address. - How is the market expected to evolve by 2033?

The market is projected to expand steadily through ongoing research, approvals of next-generation therapeutics, and rising global screening initiatives. Continued innovation in biologics and immunotherapy is expected to sustain long-term market growth.

Conclusion

The global colorectal cancer therapeutics market is poised for steady expansion, supported by rising disease prevalence, advances in immunotherapy, and the growing adoption of personalized medicine. Strong research investments and increased approvals of innovative targeted therapies continue to improve survival outcomes and broaden treatment access.

North America is expected to maintain market dominance due to its advanced healthcare systems, while the Asia Pacific region shows promising growth potential. Despite challenges related to treatment costs and late diagnosis, early screening programs and biomarker-driven approaches are driving improved management. Overall, the market outlook remains positive with sustained innovation expected through 2033.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)