Table of Contents

Overview

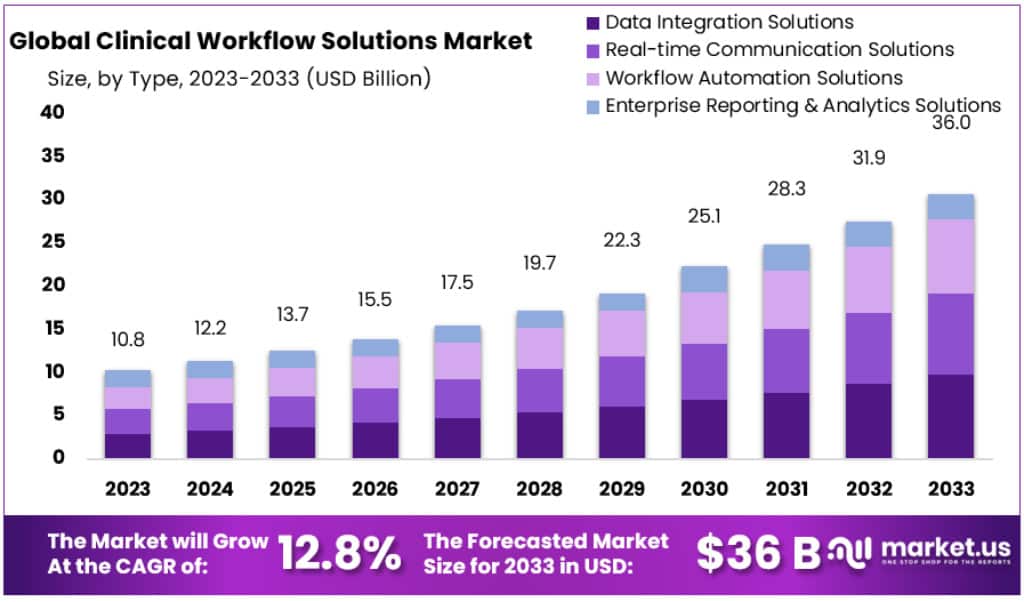

The Global Clinical Workflow Solutions Market is projected to grow from USD 10.8 billion in 2023 to USD 36.0 billion by 2033, registering a CAGR of 12.8%. This growth is being driven by the rapid digitization of healthcare, increasing demand for efficiency, and the need to improve patient outcomes. Hospitals and clinics are investing in electronic health records, computerized physician order entry, and integrated platforms to enhance clinical efficiency and comply with government-led digital record mandates.

A significant driver of adoption is the growing pressure to reduce costs and manage workforce shortages. Workflow solutions streamline administrative tasks, reduce redundancies, and improve care delivery efficiency. Automation in patient management and resource utilization allows providers to minimize delays and errors, thus ensuring better outcomes while maintaining operational sustainability. The demand for such systems is further reinforced by the rising prevalence of chronic diseases that place additional strain on healthcare infrastructure.

The market is also witnessing strong momentum from technological advancements, particularly the integration of artificial intelligence and analytics. Predictive tools and machine learning algorithms are supporting faster diagnostics, personalized treatment planning, and improved triage management. These innovations align closely with the growing emphasis on value-based care models, where data-driven decision-making is essential for efficiency and patient satisfaction.

In addition, the expansion of telehealth and remote care since the COVID-19 pandemic has accelerated the demand for solutions that integrate virtual consultations, remote monitoring, and digital communication. Clinical workflow platforms that support seamless integration of telemedicine into existing healthcare systems are becoming essential. Regulatory and compliance requirements, including HIPAA and GDPR, are further encouraging adoption, as providers need secure, structured systems for patient data management and audit readiness.

Investment in healthcare IT infrastructure, especially in developed markets, is further boosting the uptake of these solutions. The transition toward patient-centered care, coupled with modernization initiatives such as cloud-based deployments and interoperability programs, is reinforcing the growth outlook. Clinical workflow solutions now play a critical role in enhancing patient engagement, ensuring continuity of care, and meeting rising expectations for transparency and coordinated treatment delivery.

Key Takeaways

- The global clinical workflow solutions market is forecasted to rise from USD 10.8 billion in 2023 to USD 36.0 billion by 2033.

- This expansion reflects a Compound Annual Growth Rate (CAGR) of 12.8% during the analysis period, highlighting strong long-term demand for workflow solutions.

- Data integration solutions accounted for over 27.2% of the 2023 market share, supported by rising healthcare data volumes and regulatory compliance requirements.

- The hospital segment led the end-use category in 2023, generating more than 45.4% of revenues, underscoring hospitals’ reliance on workflow optimization solutions.

- North America represented the largest regional market, capturing over 42.1% of the share in 2023 due to established healthcare infrastructure and digital adoption.

- The Asia Pacific region is projected to grow fastest, achieving a CAGR of 13.8%, driven by surging healthcare investments and digital transformation initiatives.

Regional Analysis

North America dominated the market in 2023, accounting for the largest share of more than 42.1%. The regional market was valued at USD 4.3 billion during the same period. Growth in this region can be attributed to the increasing adoption of electronic health records and interoperability solutions. Factors such as government initiatives, rising patient admissions, and greater R&D spending are strengthening the market. Furthermore, a heightened focus on quality patient care is contributing to the consistent expansion across healthcare organizations in this region.

The region’s healthcare providers are prioritizing digitization to enhance secure data exchange within organizations. Substantial healthcare spending has been directed toward modern digital systems. This includes investments in electronic records and interoperable platforms that streamline processes. Moreover, collaborations between healthcare institutions and technology companies are accelerating adoption. Such efforts are also driven by regulatory frameworks that emphasize security and efficiency. The combination of these factors ensures the long-term growth of North America’s healthcare information technology market.

Asia Pacific is expected to grow at the fastest compound annual growth rate of 13.8% during the forecast period. The regional market expansion is supported by increasing investments from emerging economies. Governments are promoting eHealth initiatives, which encourage wider adoption of digital health solutions. Improved healthcare infrastructure and strong policy support are creating favorable conditions for growth. In addition, rising demand for advanced healthcare IT services reflects the growing awareness of patients and providers. This demand positions the region as a key driver of global market expansion.

Medical tourism is also emerging as a critical growth factor for Asia Pacific. Countries across the region are attracting patients through advanced care facilities and cost-effective services. This has increased the need for high-quality information technology solutions to manage rising patient volumes. Furthermore, initiatives that promote digitization and innovation are accelerating the deployment of modern systems. The region’s rising healthcare standards, together with its growing population, are ensuring sustained market demand. These factors collectively reinforce Asia Pacific’s role as the fastest-growing regional market.

Segmentation Analysis

The clinical workflow solutions market was led by the Data Integration Solutions segment in 2023, holding more than 27.2% revenue share. The dominance of this type is driven by rising healthcare data volumes and increasing operational costs. Healthcare providers prefer integrated systems that allow access to patient information across the continuum of care. The growth of this segment is further supported by the widespread adoption of electronic medical records, the introduction of interoperability standards, regulatory reforms, and the industry-wide transition to value-based healthcare services.

The Care Collaboration Solutions segment is projected to expand at a notable pace during the forecast period. Growth is attributed to the rising demand for patient-centric care models and coordinated services. Payers, government bodies, and employer groups increasingly favor integrated platforms that support streamlined management and care coordination. These solutions help enhance patient care outcomes and reduce inefficiencies in workflows. Their cost-effectiveness and operational efficiency are making them more attractive, driving adoption across multiple healthcare settings.

Technological progress in wireless communication and computing capabilities has accelerated the use of connected health devices. These tools can capture, analyze, and transmit patient data in real time, thereby improving decision-making and care delivery. By connecting devices and sensors, providers can enhance workflow efficiency while ensuring better patient monitoring. This trend is expected to stimulate demand for advanced workflow solutions. The increasing need for efficient workflow management in medical facilities will continue to be a central growth factor for this segment.

In terms of end-use, the Hospital segment held the largest share of over 45.4% in 2023. This leadership is supported by the rising number of hospitals, growing demand for integrated communication systems, and government initiatives to strengthen healthcare infrastructure. Hospitals continue to adopt workflow solutions to simplify data management and improve operational efficiency. Meanwhile, ambulatory care centers and home healthcare services are projected to grow significantly. These facilities benefit from IT-enabled solutions that reduce errors, streamline communications, and support value-based and cost-effective healthcare delivery.

Key Players Analysis

The clinical workflow solutions market is highly competitive, dominated by established companies. The top ten players hold nearly 60% of the global share, while the remaining 40% is fragmented among niche providers. Growth is supported by rising investments from these leaders in advanced healthcare management systems. Hospitals and healthcare providers are increasingly renewing licensing agreements or forming new partnerships. These developments are enhancing distribution channels, improving operational efficiency, and boosting adoption rates across healthcare systems, driving momentum in the overall clinical workflow solutions market.

Sustained competition is being fueled by continuous promoting activities, strategic partnerships, and merger agreements among leading players. For example, ePlus Inc., founded in September 2020, entered this dynamic sector with innovative solutions. Its partner, Mobile Heartbeat, launched MH-CURE, a Unified Clinical Communication Platform designed to enhance clinical workflows and patient care. Such innovations reflect the emphasis placed on efficient communication tools in modern healthcare. Companies are actively seeking collaborations and product upgrades to sustain growth and increase their competitive positioning.

Prominent players in the market include Hill-Rom Holdings Inc., athenahealth Inc., Koninklijke Philips NV, Cisco Systems Inc., Capsule Technologies Inc., NXGN Management LLC, McKesson Corporation, Koch Industries (Infor Inc.), and General Electric Company. These organizations are expanding their presence by offering diverse workflow solutions tailored to hospitals, clinics, and healthcare systems. Hillrom and Philips, for example, have strengthened their positions through acquisitions and product innovations. Collectively, these companies shape industry dynamics and account for the majority of market revenues, reflecting strong consolidation at the top.

Collaboration between industry leaders and government organizations also drives innovation. A notable example is the American Medical Association’s partnership with Google in 2018, which launched the AMA Health Care Interoperability and Innovation Challenge. This initiative encouraged new mobile health technologies, including apps and wearables, that improve information sharing and chronic disease management. Over the forecast period, such programs are expected to accelerate adoption of clinical workflow solutions globally. They highlight the growing alignment of healthcare technology providers with public initiatives aimed at digital transformation and patient care improvement.

FAQ

1. What are clinical workflow solutions?

Clinical workflow solutions are healthcare IT systems designed to streamline and automate day-to-day clinical tasks. They improve communication between doctors, nurses, and staff while reducing manual errors. These solutions help in organizing patient data and supporting quick decision-making. By integrating with Electronic Health Records (EHRs), they ensure smooth operations and better patient care. Their main goal is to save time, reduce costs, and allow healthcare providers to focus more on patients instead of administrative work.

2. What are the key components of clinical workflow solutions?

The key components include tools for patient data management, workflow automation, and collaboration. They also provide real-time monitoring and seamless integration with Electronic Health Records (EHRs). These components work together to enhance care coordination and ensure data accuracy. Automation reduces manual processes, while communication platforms connect different teams instantly. Real-time monitoring helps in quick decision-making. Together, these components create a connected environment where tasks are managed efficiently, and patients receive timely, accurate, and better-quality care across all healthcare settings.

3. How do clinical workflow solutions benefit healthcare providers?

Clinical workflow solutions deliver clear benefits for healthcare providers. They reduce administrative burdens by automating repetitive tasks and help manage patient records efficiently. Staff members gain quicker access to accurate information, which supports better decision-making. Improved communication among teams ensures smoother coordination. This leads to fewer errors and improved patient safety. With reduced time spent on manual work, providers can focus on direct patient care. These benefits collectively enhance patient outcomes, operational efficiency, and overall satisfaction within healthcare organizations.

4. Which healthcare settings use clinical workflow solutions?

Clinical workflow solutions are used across multiple healthcare settings. Hospitals use them to manage complex patient loads and maintain clear communication between departments. Outpatient clinics and specialty centers rely on them for streamlined processes and faster service. Ambulatory care facilities benefit from efficient patient flow and record handling. Diagnostic laboratories use workflow solutions to integrate results with patient histories quickly. These solutions adapt to the unique needs of each environment, helping ensure better productivity, reduced errors, and enhanced quality of patient care.

5. What are the challenges in implementing clinical workflow solutions?

Implementing clinical workflow solutions comes with several challenges. High setup costs can be difficult for smaller healthcare facilities. Integration with older legacy systems often causes delays and technical issues. Staff may resist adopting new technology, which can slow down efficiency. Data security is another concern as sensitive patient records must be protected. Training employees on how to use the system is time-consuming but essential. Despite these challenges, effective planning and strong support can help organizations achieve long-term success with these solutions.

6. What is the size of the clinical workflow solutions market?

The clinical workflow solutions market is valued in billions of dollars and continues to grow steadily. This growth is driven by rising digital transformation in healthcare and the increasing adoption of electronic health records. Government support for digital health initiatives also plays a key role. The demand for streamlined workflows and efficient communication tools is expanding rapidly. Growth rates are projected to remain positive over the coming years, reflecting the strong need for technology-driven solutions that improve efficiency and patient outcomes globally.

7. What factors are driving market growth?

Several factors are driving the growth of the clinical workflow solutions market. The adoption of electronic health records has increased the need for integrated solutions. Healthcare providers are focusing on reducing errors and improving efficiency. Rising patient loads create demand for faster, streamlined workflows. Regulatory support is encouraging investment in digital health. Hospitals and clinics also aim to cut costs while enhancing patient care. Together, these factors make workflow solutions essential for modern healthcare systems and drive significant growth across different regions worldwide.

8. Which segments are included in the market?

The clinical workflow solutions market is segmented into different categories. By type, it includes workflow automation, communication tools, data integration systems, and real-time monitoring solutions. By end-user, hospitals, outpatient clinics, diagnostic centers, and ambulatory facilities are the key segments. Geographically, the market covers North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Each segment has specific needs and growth opportunities. This structured segmentation helps stakeholders analyze demand patterns, prioritize investment decisions, and design targeted strategies for sustainable business growth.

9. Which region dominates the market?

North America dominates the clinical workflow solutions market due to its advanced healthcare systems and faster adoption of digital health technologies. Government programs and favorable regulations further support this growth. Hospitals and clinics in the region have invested heavily in healthcare IT systems. Europe follows with strong adoption rates, supported by healthcare reforms and digitalization initiatives. The Asia-Pacific region is expected to grow the fastest, driven by large patient populations and rising investments. These regional dynamics highlight both established strength and emerging opportunities.

10. Who are the key players in the clinical workflow solutions market?

The market is shaped by several leading companies. GE Healthcare and Cerner Corporation (Oracle Health) are prominent global players. Philips Healthcare and Allscripts Healthcare Solutions also provide innovative systems. Hill-Rom Holdings and Vocera Communications contribute with specialized workflow and communication tools. These companies compete through product innovation, strategic partnerships, and expanding service portfolios. Their presence ensures continuous development of advanced solutions. New entrants and regional firms are also emerging, further intensifying competition. Together, these players drive innovation and market expansion worldwide.

11. What are the emerging trends in the market?

The clinical workflow solutions market is witnessing several key trends. Artificial Intelligence (AI) and Machine Learning (ML) are being integrated to improve decision-making and automation. Cloud-based solutions are gaining popularity for cost-effectiveness and scalability. Interoperability between systems is becoming a priority for healthcare providers. Telehealth integration is rising, especially after the global pandemic. Mobile healthcare applications are also being adopted rapidly by both patients and providers. These trends highlight the market’s shift toward smarter, more connected, and patient-centric digital healthcare solutions globally.

Conclusion

The global clinical workflow solutions market is on a strong growth path, supported by the rapid digitalization of healthcare and rising demand for efficient care delivery. These solutions are becoming essential as providers face cost pressures, workforce shortages, and increasing patient volumes. By integrating electronic health records, automation, and advanced communication tools, workflow systems are improving decision-making and reducing errors. The adoption of artificial intelligence, cloud platforms, and telehealth integration is further shaping the market’s future. With growing investments in healthcare IT infrastructure and supportive government initiatives, clinical workflow solutions will remain central to modern healthcare, enabling better outcomes and stronger patient engagement worldwide.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)