Table of Contents

Overview

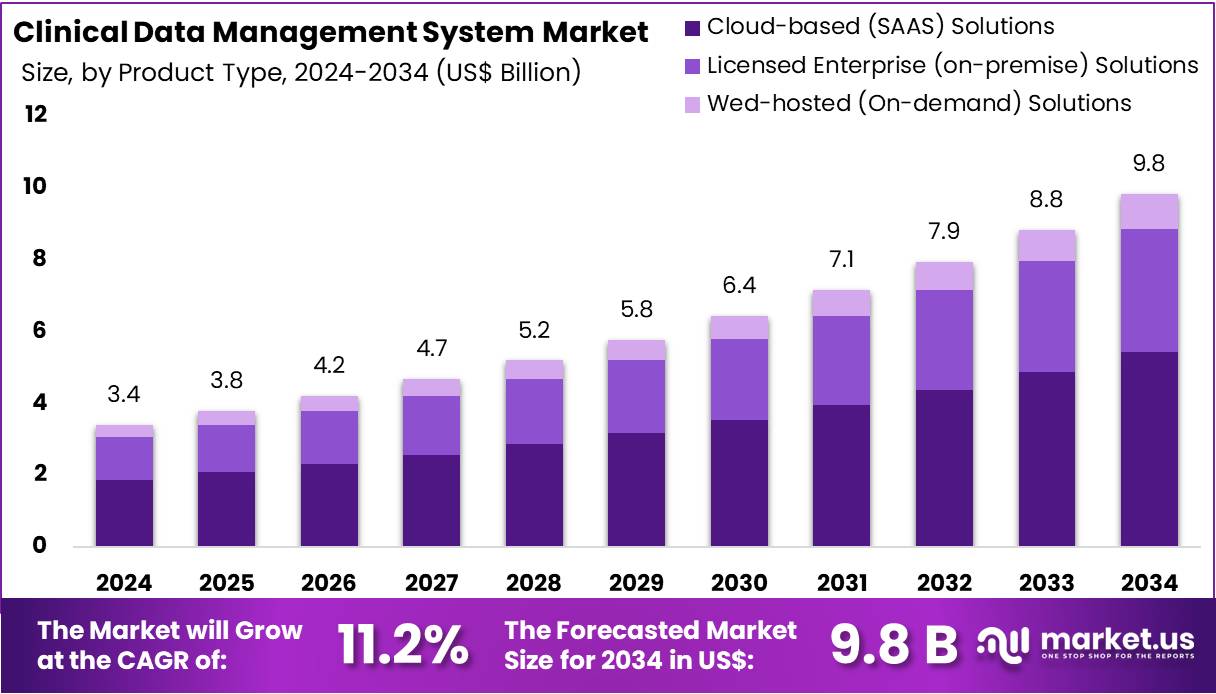

New York, NY – July 29, 2025 – The Global Clinical Data Management System Market size is expected to be worth around US$ 9.8 Billion by 2034, from US$ 3.4 Billion in 2024, growing at a CAGR of 11.2% during the forecast period from 2025 to 2034.

The global market for Clinical Data Management Systems (CDMS) is witnessing notable expansion, driven by the rising complexity of clinical trials and an increasing need for efficient, accurate, and compliant data management solutions. These systems are designed to streamline the collection, validation, integration, and storage of clinical trial data, ensuring the integrity and reliability of outcomes throughout the research process.

The growing emphasis on regulatory compliance and quality assurance has led to widespread adoption of CDMS across pharmaceutical companies, contract research organizations (CROs), academic research centers, and medical device manufacturers. The increasing use of electronic data capture (EDC), remote monitoring, and real-time analytics has further fueled the transition from traditional paper-based methods to advanced digital platforms.

The market is segmented based on component, deployment model, and end-user. Cloud-based deployment is gaining popularity due to its flexibility, ease of access, and cost-efficiency. Additionally, integration with artificial intelligence and machine learning tools is enhancing data accuracy and predictive capabilities.

North America currently leads the adoption of clinical data management technologies due to a strong clinical research ecosystem and supportive regulatory infrastructure. However, Asia Pacific is emerging as a high-growth region with expanding clinical trial activity and improving healthcare infrastructure.

Key Takeaways

- The global clinical data management system market reached a valuation of USD 3.4 billion in 2024 and is projected to grow to USD 9.8 billion by 2034, registering a CAGR of 11.2% over the forecast period.

- In 2024, cloud-based (SaaS) solutions dominated the deployment segment, accounting for 55.2% of the total market revenue.

- Pharmaceutical and biotechnology companies led the end-user segment, capturing 44.0% of the global market share in 2024.

- North America held the largest regional share in 2024, contributing over 48.2% of the total market revenue.

Segmentation Analysis

- Product Type Analysis: The clinical data management system market is segmented into cloud-based (SaaS) solutions, licensed enterprise (on-premise) solutions, and web-hosted (on-demand) solutions. Among these, cloud-based (SaaS) solutions held the leading share of 55.2% in 2024. This dominance is attributed to their scalability, cost-efficiency, and support for decentralized trials. Cloud platforms enable real-time collaboration, efficient data sharing, and remote monitoring, all of which are essential for modern clinical trial operations and regulatory compliance.

- Application Analysis: By application, the market is segmented into pharmaceutical/biotech companies, contract research organizations (CROs), medical device companies, and others. In 2024, pharmaceutical and biotechnology companies accounted for 44.0% of the global market share. Their dominance is driven by the increasing complexity of clinical trials and the need for accurate, compliant, and large-scale data management. The integration of AI and machine learning into CDMS platforms further enhances trial efficiency, supporting faster drug development and reinforcing the segment’s leadership.

Market Segments

By Product Type

- Cloud-based (SAAS) Solutions

- Licensed Enterprise (on-premise) Solutions

- Wed-hosted (On-demand) Solutions

By Application

- Pharma/biotech Companies

- Contract Research Organizations (CROs)

- Medical Device Companies

- Others

Regional Analysis

North America continues to lead the global Clinical Trial Management System (CTMS) market, supported by the presence of advanced research institutions, top-tier universities, and major pharmaceutical and medical device companies. These entities actively engage in clinical trials and rely on CTMS platforms for streamlined planning, monitoring, and regulatory adherence. The region also benefits from a well-established healthcare infrastructure, creating favorable conditions for clinical research activities.

Government initiatives further reinforce this leadership. In January 2023, the Canadian government announced multiple healthcare-focused programs, including national training platforms, clinical trial consortia, and public health research projects. Approximately USD 60 million was allocated to support 22 projects aligned with Canada’s Biomanufacturing and Life Sciences Strategy (BLSS). These investments aim to enhance the nation’s clinical research capacity and foster innovation across the healthcare sector.

Such developments have significantly contributed to the rising demand for CTMS solutions in the region. The combination of strong institutional capabilities, strategic government funding, and ongoing technological innovation ensures that North America remains the dominant regional market for clinical trial management systems.

Emerging Trends

- Standardized Data Submission via CDISC Dataset-JSON: In April 2025, the FDA issued a Federal Register notice (Docket No. FDA-2025-N-0129) requesting comments on adopting the CDISC Dataset-JSON v1.1 as a new exchange format for electronic study data submissions to CDER and CBER. This move can reduce the reliance on legacy SAS XPT files and streamline data interchange between sponsors and regulators.

- Adoption of HL7 FHIR for Real-World Data Integration: The FDA published a notice on April 23, 2025 (Docket No. FDA-2025-N-0287), exploring the use of HL7 FHIR to submit clinical study data derived from real-world sources. Aligning with ONC’s 2020 final rule, this initiative can enhance interoperability between EHR systems and CDMS platforms, reducing mapping challenges for real-world data.

- API-Driven Access via ClinicalTrials.gov FHIR Interface: ClinicalTrials.gov launched a public FHIR API in early 2025, enabling programmatic retrieval of trial registration and results data. This API supports standardized R4 resources, making it easier for CDMS platforms to integrate and analyze information from over 440,000 registered studies.

Use Cases

- Regulatory Submission of Structured Data: Sponsors preparing marketing applications can leverage the proposed CDISC Dataset-JSON standard to submit electronic study data to the FDA. As of July 29, 2025, 48 public comments had been received on this proposal, reflecting broad stakeholder engagement in shaping the future submission format.

- Programmatic Trial Data Integration: Biotechnology firms and academic researchers can use the ClinicalTrials.gov FHIR API to automatically ingest and synchronize trial metadata and results. The API provides access to R4 resources for more than 440,000 studies, facilitating real-time updates and reducing manual data entry efforts by up to 30% in some analytics workflows.

- Remote Patient-Generated Data Collection: In a cluster-randomized trial (ClinicalTrials.gov NCT04098913), 89 families (181 children and 164 adults) used wearable devices and mobile apps to record physical activity and sleep data in everyday settings. This approach improved data completeness and timeliness, with over 95% of expected daily measurements successfully captured and uploaded to the CDMS platform.

Conclusion

The global Clinical Data Management System (CDMS) market is undergoing rapid transformation, driven by the increasing complexity of clinical trials, regulatory demands, and technological advancements. Cloud-based solutions, AI integration, and real-world data interoperability are redefining how trial data is captured, managed, and submitted.

North America remains the market leader, supported by strong research infrastructure and government initiatives. Meanwhile, the adoption of emerging standards like CDISC Dataset-JSON and HL7 FHIR is streamlining regulatory submissions and enhancing system interoperability. As clinical research continues to evolve, the demand for robust, flexible, and scalable CDMS platforms is expected to accelerate further.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)