Table of Contents

Overview

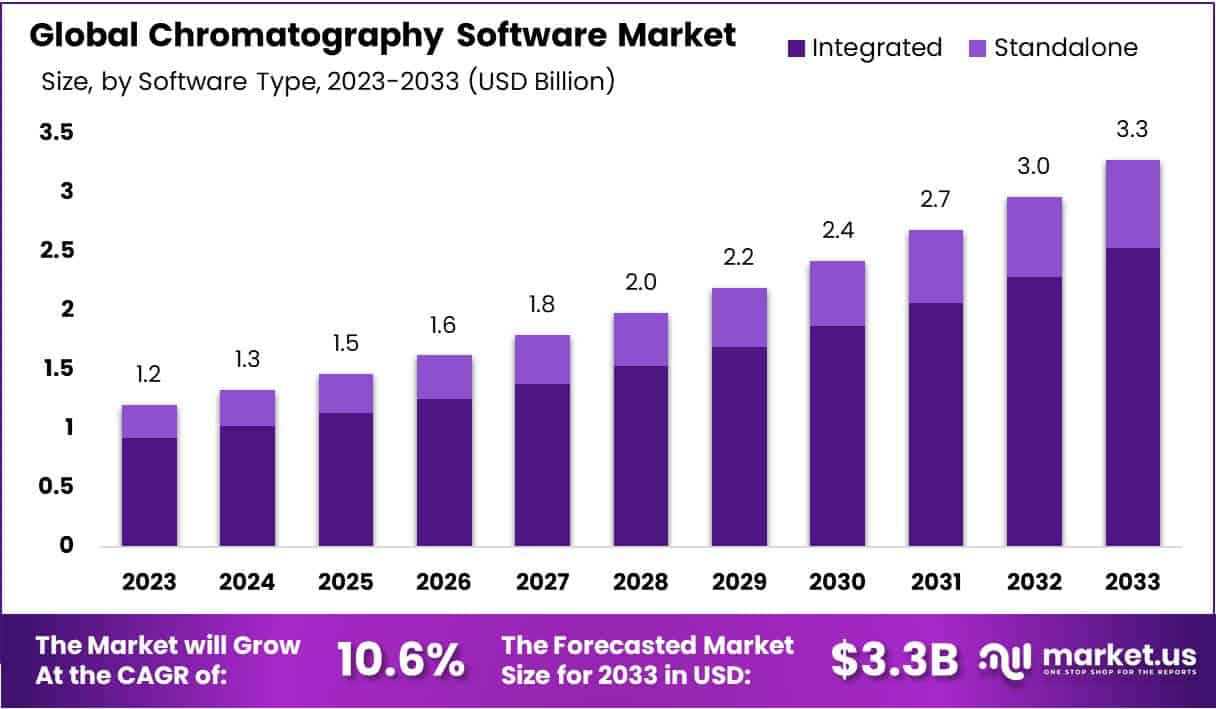

The Global Chromatography Software Market is projected to reach USD 3.3 billion by 2033, growing from USD 1.2 billion in 2023. A CAGR of 10.6% is expected during 2024–2033. The expansion is supported by rising demand for accurate laboratory data management. Regulatory agencies emphasize secure, traceable, and validated digital records. Laboratories adopt software with compliance features, including audit trails, controlled access, and electronic signatures. These systems help reduce human errors and ensure data reliability. Market growth is further driven by growing awareness of data integrity standards and the increasing need to standardize analytical workflows across diverse research environments.

Pharmaceutical and biopharmaceutical companies remain leading adopters. The development of complex biologics and precision medicines requires advanced separation and detection methods. Chromatography software supports analytical tasks, including purity testing, impurity profiling, and quality verification. The increasing number of drug candidates in clinical pipelines enhances software demand. Research teams prioritize platforms with intelligent analysis, faster processing, and automation capacity. Efficient data review and reporting optimize decision-making in regulated drug development processes. As analytical requirements rise, vendors focus on enhancing scalability, multidimensional data handling, and compatibility with emerging instrumentation.

Digital transformation in laboratories is accelerating software uptake. Organizations transition from manual data logging to automated systems that connect instruments, databases, and laboratory information management systems. Cloud-based deployment enables real-time monitoring, centralized data storage, and secure sharing across sites. Remote operations, especially in distributed research networks, support business continuity and improve collaboration. Modern chromatography software also integrates predictive analytics and enhanced visualization tools. These capabilities simplify method development and reduce analysis time. The shift toward automation increases throughput and improves operational consistency across routine and advanced testing workflows.

Market opportunities are expanding across new industries. Demand is rising in environmental testing, chemical manufacturing, food and beverage safety, and forensic sciences. These sectors require accurate separation science to detect contaminants, maintain quality standards, and support regulatory compliance. Legacy laboratory systems are being upgraded to meet current data requirements. Modernization initiatives encourage replacement of outdated chromatography data systems with secure and scalable solutions. Vendors offer improved interoperability with contemporary hardware and digital ecosystems. This enhances long-term adoption prospects. Continuous innovation in usability and analytical intelligence ensures that chromatography software remains a critical enabler of advanced science, industrial safety, and efficient laboratory performance.

Key Takeaways

- The chromatography software market is set to reach USD 3.3 billion by 2033, growing steadily at a 10.6% CAGR from 2024–2033.

- Integrated software currently leads the market with a 77.1% share, and cloud-based deployment is preferred by 68.9% of users.

- The pharmaceuticals sector holds the largest share at 35.2%, followed by strong demand from food and beverage and environmental testing industries.

- Market growth is being driven by rising pharmaceutical needs, strict regulatory compliance, and increasing investment in research and development.

- High costs of chromatography systems remain a major challenge, especially for smaller companies and research institutions with limited budgets.

- AI and machine learning are improving data analysis, while cloud-based solutions are offering better scalability and operational efficiency.

- Cloud adoption continues to rise as laboratories seek easier access to data and seamless remote collaboration.

- North America maintains a dominant 45% market share thanks to its advanced healthcare systems and strong regulatory support.

- The market outlook remains positive as innovation and technology improvements are expected to shape future competitiveness and growth.

Regional Analysis

In 2023, North America held the dominant position in the Chromatography Software Market. The region captured more than 45% market share and achieved a market value of USD 0.4 billion. This leadership was supported by the presence of major industry vendors and a strong technological base. Significant R&D investments also supported growth. Pharmaceutical and biotechnology companies in the region depend on chromatography techniques. This reliance increased the need for advanced software. Strict regulatory frameworks, including FDA guidelines, encouraged organizations to adopt compliant chromatography software.

The pharmaceutical and biotechnology industries remain vital contributors to software adoption. Chromatography software supports drug discovery, testing, and production quality. Strong healthcare infrastructure further accelerates usage. Government programs promoting personalized medicine also encourage demand. Clinical diagnostics and academic laboratories use chromatography tools for accurate analysis. Due to these conditions, software integration continues to grow steadily. Investments in digital laboratory automation strengthen growth. The market outlook shows continuous expansion supported by innovation and high research activities. This solid foundation ensures ongoing development.

North America is expected to maintain its market leadership. Advancements in automation and data-driven solutions will support this position. Cloud-based platforms and improved data management tools are gaining popularity. These technologies improve speed, accuracy, and regulatory compliance. The region’s research landscape remains highly competitive. Companies focus on enhancing healthcare outcomes through modern analytical systems. Increased collaboration among industry players fosters innovation. Continuous improvement in laboratory workflows drives new opportunities. The demand for efficient and reliable analytical software continues to rise.

However, staying competitive requires strategic flexibility. Regulatory policies continue to evolve, creating compliance challenges for businesses. Firms must monitor these changes and respond quickly. Innovators targeting emerging trends will gain an advantage. Stakeholders must focus on quality improvement and advanced digital tools. Partnerships with research institutions strengthen product capabilities. Strong customer support and training enhance market presence. As North America drives global market growth, innovative solutions will remain essential. Adaptability and investment in technology will define long-term success in this sector.

Segmentation Analysis

In 2023, the integrated software segment led the Chromatography Software Market with over 77.1% share. Its strong position is linked to advanced features supporting complex chromatography analysis. Integrated systems combine acquisition, analysis, reporting, and data management on one platform. This combination enhances efficiency and ensures accuracy in laboratory workflows. High adoption reflects the need for reliable results in research environments. Standalone software remains relevant for specialized tasks or lower budgets. It supports specific processes and allows customization. It continues to serve laboratories needing targeted functionalities.

The preference for integrated solutions highlights growing demand for interoperability and coordinated workflows. Researchers seek smooth data flow across instruments and systems. Integrated platforms support collaboration and handle complex datasets. This trend is influenced by rising research complexity in pharmaceuticals and biotechnology. Cloud-based architecture is also helping integrated platforms grow faster. It offers flexible scaling and better access to shared data. These advantages support advanced analytics. The shift reflects the need for unified solutions that improve productivity, compliance, and overall performance in modern laboratories.

In 2023, cloud-based deployment dominated the market with over 68.9% share. Its growth is supported by low upfront costs and remote data access. Laboratories benefit from improved collaboration in distributed research settings. Automatic updates enhance operational efficiency. On-premise solutions remain important for strict data control. They are preferred in regulated industries requiring secure internal systems. Higher installation and maintenance costs limit adoption. Yet strong cybersecurity safeguards keep this segment relevant. Market growth is driven by digital transformation in research and quality control processes.

The pharmaceutical industry led the market in 2023 with over 35.2% share. Chromatography software is widely used in drug discovery, analysis, and quality assurance. High demand for biopharmaceuticals supports continued investment. Food and beverage companies use chromatography tools to ensure product safety. Environmental laboratories depend on precise pollutant monitoring. Forensic organizations require accurate analysis for chemical evidence. Other sectors such as petrochemicals and academia also contribute. Growth is driven by innovation, rising testing volumes, and the need for reliable data management across industries.

Key Market Segments

Software Type

- Standalone

- Integrated

Deployment Mode

- Cloud-Based

- On-Premise

End-Use Industry

- Pharmaceuticals

- Food & Beverage

- Environmental Testing

- Forensic Testing

- Other End-Use Industries

Key Players Analysis

The chromatography software market is driven by innovation and strong competitive strategies. Key players focus on advanced analytical solutions that increase productivity and ensure data integrity in laboratories. Their continuous R&D supports technological enhancements and regulatory compliance. Thermo Fisher Scientific Inc. maintains a leading role due to its broad solution range and investment capabilities. The company strengthens customer trust by offering reliable software systems. Its strong market presence, strategic expansions, and integration of automation position it well for future growth and sustained performance across global industries.

Strategic product diversification and global reach support prominent competitors in capturing higher market shares. Agilent Technologies Inc. uses its extensive customer network and advanced platforms to improve adoption across pharmaceutical and biotechnology sectors. Its software enhances workflow efficiency and reduces operational errors. Continuous upgrades support compliance and data traceability. Market growth is encouraged by user-friendly interfaces and cloud-enabled features. Customer-centric approaches reinforce loyalty while helping clients achieve better analytical outcomes in demanding environments.

Innovative technologies and high-precision solutions create strong differentiation among market participants. Waters Corporation focuses on digital transformation and its expertise strengthens operational accuracy. Advanced chromatography software supports data-driven decisions in research and quality control labs. The company improves performance through real-time analytics and integrated systems. Competitive pricing and technical support further reinforce its market relevance. Its strategic investments aim to expand applications in environmental, life sciences, and industrial testing, ensuring sustainable competitive positioning in the evolving marketplace.

Reputed instrument manufacturers strengthen market competitiveness through integrated product offerings. Shimadzu Corporation leverages its engineering excellence to improve laboratory automation and data quality. It emphasizes robust partnerships and service capabilities to attract new users. Other emerging players also drive innovation by adopting cloud technologies and artificial intelligence. The overall market sees balanced competition. Companies improve strengths through acquisitions and targeted expansions. SWOT assessments support strategic planning. These approaches reinforce customer satisfaction and long-term revenue growth across the chromatography software market.

Market Key Players

- Thermo Fisher Scientific Inc.

- Agilent Technologies Inc.

- Waters Corporation

- Shimadzu Corporation

- PerkinElmer Inc.

- Bruker Corporation

- Danaher Corporation

- Bio-Rad Laboratories Inc.

- Gilson Inc.

- KNAUER

- Restek Corporation

- SCION Instruments

- Other Key Players

Challenges

1) Growing Pressure on Data Integrity

Data integrity requirements continue to increase in regulated laboratories. Electronic records must be complete, accurate, and protected from changes. Regulators expect secure and time-stamped audit trails that show the full history of any result. FDA 21 CFR Part 11 rules guide how records and signatures must be controlled. Implementing these expectations is complex. Labs often manage many instruments, multiple users, and global sites. Aligning policies, system configurations, and workflows takes significant effort. Continuous monitoring is also required. Any gaps can lead to compliance risk, inspection findings, or delayed product release. Data must remain trustworthy at every stage.

2) Audit Trail Quality and Review Burden

Audit trail design and review are key compliance areas. It is not enough to capture who made a change, what happened, when it happened, and why. Teams must review audit trails on a routine basis. They must also show that review procedures are effective. As the number of instruments grows, the review workload rises quickly. Legacy systems can make access and trending more difficult. Poor audit trail structures lead to missing context and long investigations. Regulators often focus on audit trail weaknesses during inspections. Better automation and standardized records reduce the effort and assure stronger oversight.

3) Heavy Validation Workload

Computerized system validation is required when software supports regulated processes. USP <1058> links instrument qualification with validation steps for the software environment. Each upgrade, configuration change, or security update can trigger new testing and documentation. Labs with diverse instruments and frequent vendor releases face high ongoing effort. Validation demands clear requirements, traceability, and documented evidence that systems function as intended. Without a risk-based approach, the workload becomes difficult to maintain. Many teams struggle to keep validation current, especially with limited resources. Efficient planning and governance are essential to avoid compliance gaps and delays.

4) Cloud Adoption Under GxP Rules

Cloud deployment models provide flexibility and lower infrastructure costs. However, use in GxP environments requires strict validation and security controls. FDA guidance on Computer Software Assurance supports a risk-based approach. Even so, responsibilities must be clearly defined between the vendor and the regulated company. Control over data, access, and configuration must be maintained. Remote access and shared resources increase complexity. Evidence is needed that the service remains compliant throughout its lifecycle. Clear agreements, documented procedures, and ongoing oversight are necessary. Otherwise, cloud benefits may be offset by regulatory risks and unplanned delays.

5) Integration Gaps Across Laboratory Systems

Laboratories rely on many digital systems. These include LIMS, ELN, SDMS, ERP, and chromatography data systems. When data are not connected, information stays in silos. Manual data transfers increase errors and slow operations. Different data formats and naming rules make integration difficult. Real-time interfaces require stronger performance and monitoring than batch uploads. Vendor APIs may not support all required metadata. Poor integration reduces productivity and traceability. It also limits automation of approval workflows. Eliminating silos supports better decision-making and faster reporting. Strong data governance and standardization are essential to reach this goal.

6) Interoperability and FAIR Data Challenges

Organizations now focus on FAIR data principles. Data should be easy to find, access, integrate, and reuse. Chromatography data often fall short of these goals. Output files may lack detailed metadata or use formats that only vendor software can read. This limits secondary analysis and long-term value. Data stored in isolated systems cannot support advanced analytics. Consistent standards, controlled vocabularies, and harmonized structures are needed. FAIR maturity improves collaboration across sites and tools. It also enables AI and predictive models. Better interoperability creates a strong data foundation for future digital transformation.

7) AI Readiness Versus Compliance Reality

Artificial intelligence can improve data interpretation. Examples include peak detection and deconvolution. However, AI models require training data, performance monitoring, and strict validation. Regulators expect explainable results and controlled model updates. Real-time use in GxP workflows needs clear justification. Audit trails must capture how algorithms influence outcomes. Any bias or drift must be addressed. Teams must manage version control and documented risk assessments. Without proper governance, AI can increase compliance risk rather than reduce effort. Progress depends on aligning innovation with regulatory expectations.

8) Cybersecurity and Access Control

Cybersecurity threats continue to increase. Chromatography systems store critical data that must be protected. Electronic signatures, user authentication, and secure storage are required. Role-based access ensures only trained personnel perform key actions. Remote access expands the system attack surface. Strong password policies, network segmentation, and encryption help reduce risk. Continuous monitoring is needed to detect suspicious activity. Audit trails must show who accessed records and what actions occurred. A cybersecurity incident can stop operations and damage data integrity. Robust controls maintain trust in analytical results and support regulatory compliance.

Opportunities

1) Risk-based validation with CSA

Risk-based validation helps focus efforts where the highest risks exist. The FDA Computer Software Assurance (CSA) guidance supports applying critical thinking during validation. It promotes flexibility in testing and documentation. This helps avoid excessive paperwork. Upgrades can move faster when reviewers trust targeted evidence. Teams can reduce test cases for low-risk features. More attention can be placed on critical functions like data integrity and result calculation. A streamlined approach saves time during implementation. It also supports continuous improvement. Quality and compliance remain fully protected while operational delays are minimized.

2) Built-in compliance features in modern CDS

Modern Chromatography Data Systems (CDS) come with compliance features already included. They provide electronic signatures and advanced audit trails. Access control can be managed by roles and permissions. Standard report templates help organizations meet Part 11 and Annex 11 expectations. These features reduce the need for custom development work. Fewer customizations mean fewer validation challenges. This improves consistency across labs. Inspection readiness also improves because compliance controls are embedded. Organizations can deploy updates more confidently. This allows faster technology adoption and a lower long-term compliance burden.

3) End-to-end system integration

APIs and vendor-neutral connectors enable easy integration between CDS, LIMS, ELN, SDMS, and ERP platforms. Data can move automatically across systems. This reduces transcription tasks and lowers human error. Analysts spend less time copying and checking data. Review and approval become faster and more accurate. Real-time data helps in trending, quality decisions, and batch release. Operations gain better transparency. Integrated workflows support digital quality systems. It also strengthens control over sample lifecycles. The result is greater efficiency and improved decision-making across the lab and supply chain.

4) FAIR-by-design metadata

FAIR data principles make chromatographic data easier to find and reuse. Metadata standards create clear structure and meaning. Persistent identifiers help track files over time. Provenance shows how data was generated and processed. These elements raise long-term value. They also help with regulatory review. Scientists can compare data across studies with less effort. Searching archives becomes simpler. FAIR-by-design improves method transfer and data exchange. It encourages harmonization across sites. Good metadata supports advanced analytics. Organizations gain more from each experiment and reduce repetition.

5) AI for peak processing and interpretation

Artificial intelligence improves peak detection and characterization. Machine learning models excel in complex chromatograms. They reduce false positives and manage overlapping peaks well. AI can learn from past results to improve future predictions. Fewer manual adjustments are needed. Reviewers spend less time correcting integration. Accurate identification supports stronger data integrity. Documented and validated models meet compliance expectations. Early adoption shows improved reliability. Faster interpretation accelerates decision-making. AI tools help maximize instrument performance. Labs can process more samples with the same resources.

6) Cloud scalability with shared responsibility

Validated cloud platforms support fast global deployment. Teams can access CDS securely from anywhere. Storage expands easily as data grows. Disaster recovery becomes simpler to maintain. Vendors provide strong infrastructure controls. A clear shared-responsibility model protects compliance. Defined roles for validation and change control reduce confusion. Security patches can be applied faster. Downtime becomes less frequent. Cloud systems support collaboration in real time. Updates are easier to manage across multiple locations. Overall operational performance improves while risk remains well controlled.

7) Stronger audit analytics

Centralized audit trails improve monitoring and oversight. Automated tools can scan for risky activity. They find unusual log-in patterns or repeated reprocessing. Alerts can highlight possible data issues early. Reviewers spend less time checking every event manually. This increases efficiency. Trend reporting strengthens compliance dashboards. Audit analytics also support internal inspections. Teams are better prepared for regulatory audits. Consistent data visibility across the lab reduces operational risk. Better traceability protects product quality. Continuous monitoring creates a culture of control and compliance.

Conclusion

The chromatography software market is expected to show strong and steady growth in the coming years. The demand is rising due to the need for accurate data handling and secure digital records in laboratories. Pharmaceutical, biotechnology, and other testing industries continue to adopt advanced software to improve quality and meet regulatory rules. Cloud technology, automation, and artificial intelligence are helping users simplify workflows and reduce errors. Vendors are focusing on better integration and strong data protection features. Although costs and compliance challenges exist, ongoing innovation will support wider adoption. The market outlook remains positive as modern laboratories shift toward smart, connected, and efficient digital systems.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)