Table of Contents

Overview

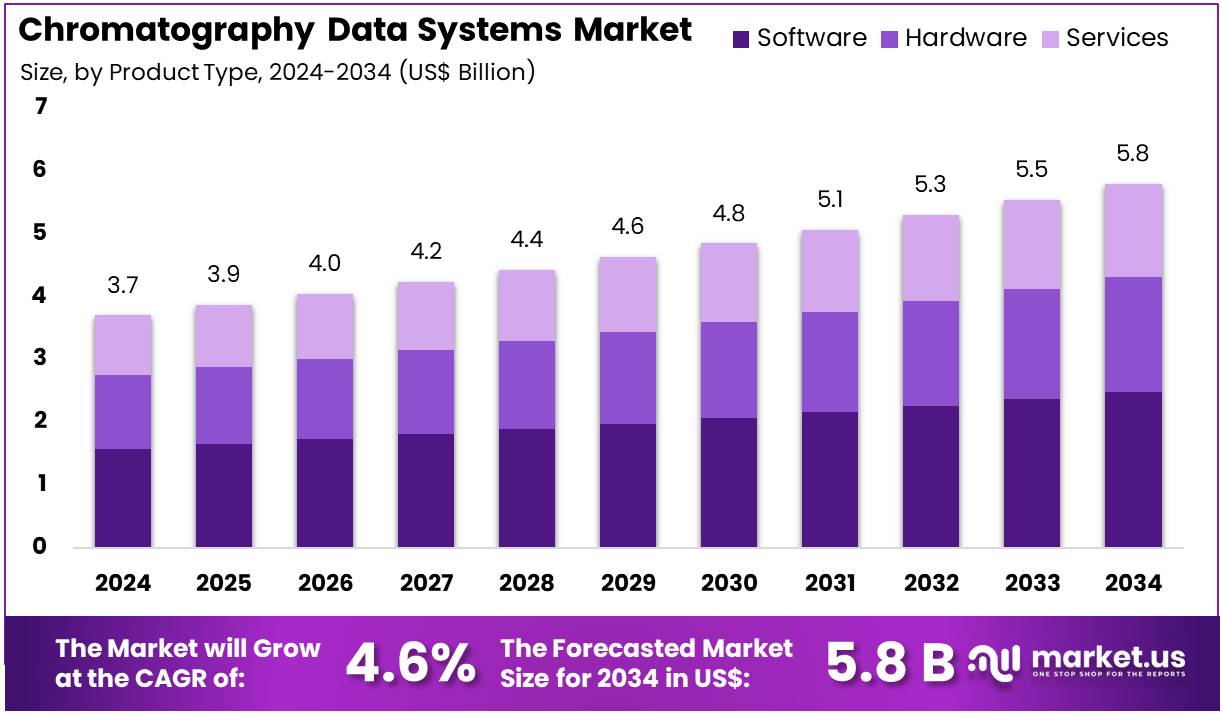

New York, NY – July 29, 2025 – The Chromatography Data Systems Market size is expected to be worth around US$ 5.8 billion by 2034 from US$ 3.7 billion in 2024, growing at a CAGR of 4.6% during the forecast period 2025 to 2034.

In 2024, the global Chromatography Data Systems (CDS) market is witnessing significant growth, driven by the increasing demand for precise analytical data management and regulatory compliance across pharmaceutical, biotechnology, environmental, and food testing sectors. Chromatography Data Systems serve as essential software platforms that collect, process, and manage chromatographic data, ensuring integrity, traceability, and efficiency in laboratory workflows.

The market is experiencing accelerated adoption due to the expanding volume of chromatography-based research and quality control activities, particularly in regulated environments governed by FDA 21 CFR Part 11 and EU Annex 11 standards. The integration of CDS with laboratory information management systems (LIMS) and enterprise resource planning (ERP) tools is further enhancing automation and data connectivity across organizations.

Cloud-based deployment models are gaining momentum, offering scalability, remote access, and cost-effective data management. Additionally, advancements in artificial intelligence (AI)-powered analytics are enabling predictive insights, thereby improving decision-making in pharmaceutical development and environmental monitoring.

North America currently dominates the CDS market due to a strong regulatory framework, high R&D investments, and the presence of major market players. Meanwhile, Asia Pacific is projected to exhibit the fastest growth owing to increasing laboratory digitization and expanding pharmaceutical manufacturing capabilities. The global CDS market is expected to continue its upward trajectory, supported by digital transformation initiatives and growing reliance on data-driven laboratory environments.

Key Takeaways

- In 2024, the global chromatography data systems market recorded a revenue of US$ 3.7 billion, and it is projected to reach approximately US$ 5.8 billion by 2034, expanding at a compound annual growth rate (CAGR) of 4.6% during the forecast period.

- Based on product type, the market is categorized into hardware, software, and services. Among these, software emerged as the leading segment in 2023, accounting for a market share of 42.7%, driven by increased demand for data integration and compliance functionalities.

- By technology, the market is segmented into on-premise, cloud-based, and hybrid solutions. The on-premise segment held the largest share in 2023, contributing 45.3% of the total market, due to its widespread use in highly regulated laboratory settings.

- In terms of application, the market includes pharmaceuticals, clinical research, academic research, and others. The pharmaceuticals segment dominated the market, capturing a revenue share of 47.9%, reflecting the sector’s high dependency on analytical data accuracy and regulatory adherence.

- Regarding end-users, the market is segmented into pharmaceutical companies, academic institutions, research laboratories, and contract research organizations. Pharmaceutical companies led this category, holding a market share of 43.8% in 2023.

- North America was the leading regional market, accounting for a 37.5% share, supported by strong R&D infrastructure and regulatory enforcement.

Segmentation Analysis

- Product Type Analysis: The software segment accounted for 42.7% of the market share, driven by rising demand for automation, regulatory compliance, and efficient chromatographic data management. CDS software supports integration with LIMS and lab instruments, enhancing operational performance and data integrity. Features such as remote access, real-time analytics, and 21 CFR Part 11 compliance are key adoption drivers. As digital transformation advances, software is expected to maintain strong growth, particularly in high-throughput and regulated laboratory settings.

- Technology Analysis: On-premise technology held a 45.3% market share due to its suitability for regulated sectors like pharmaceuticals and forensic science. These systems offer high data security, real-time control, and offline access, meeting stringent GMP and IT compliance requirements. Organizations prefer on-premise setups for customization, legacy instrument compatibility, and infrastructure sovereignty. Continued IT investments and data privacy concerns are expected to sustain demand in compliance-focused laboratories and industries throughout the forecast period.

- Application Analysis: The pharmaceuticals segment led with a 47.9% revenue share, fueled by expanding drug development and rising regulatory requirements. Chromatography data systems support precision analysis, GMP-aligned documentation, and integration with bioanalytical tools. The increase in global clinical trials and complex compound workflows strengthens demand for robust data platforms. With growing reliance on audit trails and automated reporting, pharmaceutical firms are expected to drive sustained adoption, particularly as R&D and manufacturing operations scale up globally.

- End-user Analysis: Pharmaceutical companies generated 43.8% of the market revenue, driven by their need for accurate, compliant, and traceable data systems. These firms use CDS for multi-site lab management, quality control, and regulatory alignment. With increasing R\&D investment and product pipeline expansion, demand for validated and secure data platforms is rising. As digital solutions improve throughput and reduce errors, pharmaceutical companies are likely to remain the dominant end-user segment, supported by internal operations and outsourced partnerships.

Market Segments

By Product Type

- Hardware

- Software

- Services

By Technology

- On-Premise

- Cloud-Based

- Hybrid

By Application

- Pharmaceuticals

- Clinical Research

- Academic Research

- Others

By End-user

- Pharmaceutical Companies

- Academic Institutions

- Research Laboratories

- Contract Research Organizations

Regional Analysis

North America Leads the Chromatography Data Systems Market

North America accounted for the largest revenue share of 37.5% in the chromatography data systems market, driven by the increasing adoption of advanced laboratory software by regulatory bodies. Notably, the U.S. Food and Drug Administration (FDA) has integrated Waters Corporation’s Empower Chromatography Data Software and NuGenesis Laboratory Management Software across its field science laboratories. This implementation has enhanced regulatory testing capabilities, reflecting the region’s focus on quality assurance and data integrity.

The presence of key industry players such as Thermo Fisher Scientific, Agilent Technologies, and Waters Corporation continues to support innovation and product development in the region. In addition, significant government investment in pharmaceutical and chemical research has sustained the adoption of chromatography data systems. These factors collectively reinforce North America’s leading position in the global market.

Asia Pacific Set to Record the Fastest CAGR

The Asia Pacific region is projected to register the highest compound annual growth rate (CAGR) during the forecast period, supported by increased investment in pharmaceutical R&D and rising regulatory standards. India is expected to emerge as a major growth driver due to initiatives like the Pharma Vision 2047 and the Pharma and MedTech sector scheme launched in September 2023. This government-led scheme, backed by US$ 61 million (INR 5,000 crore), is designed to boost research and development in pharmaceuticals and medical technologies.

Under this initiative, over US$ 13.41 million (INR 1,100 crore) is allocated to nine pharmaceutical firms for dedicated research activities. These developments are expected to increase the adoption of chromatography data systems across laboratories engaged in drug development, diagnostics, and quality control. As regulatory frameworks tighten and data compliance standards rise, the Asia Pacific market is poised for strong and sustained growth.

Emerging Trends

- ntegration of Artificial Intelligence and Machine Learning: The application of AI and machine learning (ML) within chromatography data systems has been expanding rapidly. These models are now assisting in method development by predicting retention times and optimizing separation conditions, thereby reducing experimental iterations. Machine-learning algorithms have been shown to achieve faster and more accurate chromatographic predictions, streamlining workflows in both research and quality control laboratories.

- Enhanced Regulatory Compliance and Data Integrity: Chromatography data systems are increasingly designed to ensure conformance with FDA 21 CFR Part 11 and current Good Manufacturing Practice (CGMP) requirements. Systems now embed features such as secure audit trails, electronic signatures, and user-access controls. This emphasis on data integrity has led to the tracking of up to 185 authorized system users with detailed privilege settings, significantly reducing the risk of unapproved data modification.

- Shift Toward Structured Data Exchange: Regulatory bodies are promoting structured-data submissions to improve review efficiency. The FDA’s Knowledge-Aided Assessment and Structured Application (KASA) initiative exemplifies this by requiring data in machine-readable formats. Chromatography data systems are adapting by providing export functions that align with these structured-data standards, facilitating faster regulatory review and reducing manual data re-formatting.

- Support for Multidimensional Chromatography Workflows: Advances in two- and three-dimensional chromatography (e.g., GC×GC and 3D-LC) are generating larger, more complex data sets. Modern CDS platforms are now capable of handling these data volumes through enhanced processing power, sophisticated peak-deconvolution algorithms, and improved visualization tools. This capability supports applications such as comprehensive impurity profiling in complex matrices.

Use Cases

- Drug Development and ADME Studies: In pharmaceutical research, CDS platforms integrated with mass spectrometry are routinely used to process thousands of samples in absorption, distribution, metabolism, and excretion (ADME) studies. These systems automate data acquisition and reporting, enabling high-throughput screening of drug candidates with reproducibility rates exceeding 99%.

- Environmental Pesticide Monitoring: Environmental laboratories employ CDS in LC-MS/MS methods to detect and quantify up to 50 medium- to highly-polar pesticide residues in sediment samples. Validated workflows achieve limits of detection in the low ng/g range, with precision (relative standard deviation) maintained below 20% across replicate analyses.

- Regulatory Compliance in CGMP Environments: Within FDA-regulated manufacturing facilities, CDS are used to enforce electronic record-keeping standards. Systems maintain detailed audit trails for as many as 185 authorized personnel, ensuring that every data modification is recorded with a timestamp and electronic signature. This capability is central to meeting both 21 CFR Part 11 and CGMP expectations.

Conclusion

The global Chromatography Data Systems (CDS) market is poised for steady expansion, driven by increasing regulatory compliance requirements, laboratory digitization, and the integration of AI-powered analytics. With a projected market size of US$ 5.8 billion by 2034 and a CAGR of 4.6%, the demand for reliable data systems continues to grow across pharmaceutical, environmental, and research sectors.

North America maintains market leadership, while Asia Pacific shows the fastest growth. As CDS platforms evolve to support multidimensional workflows and structured data exchange, their role in ensuring precision, data integrity, and regulatory adherence will remain critical in modern laboratory environments.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)