Table of Contents

Overview

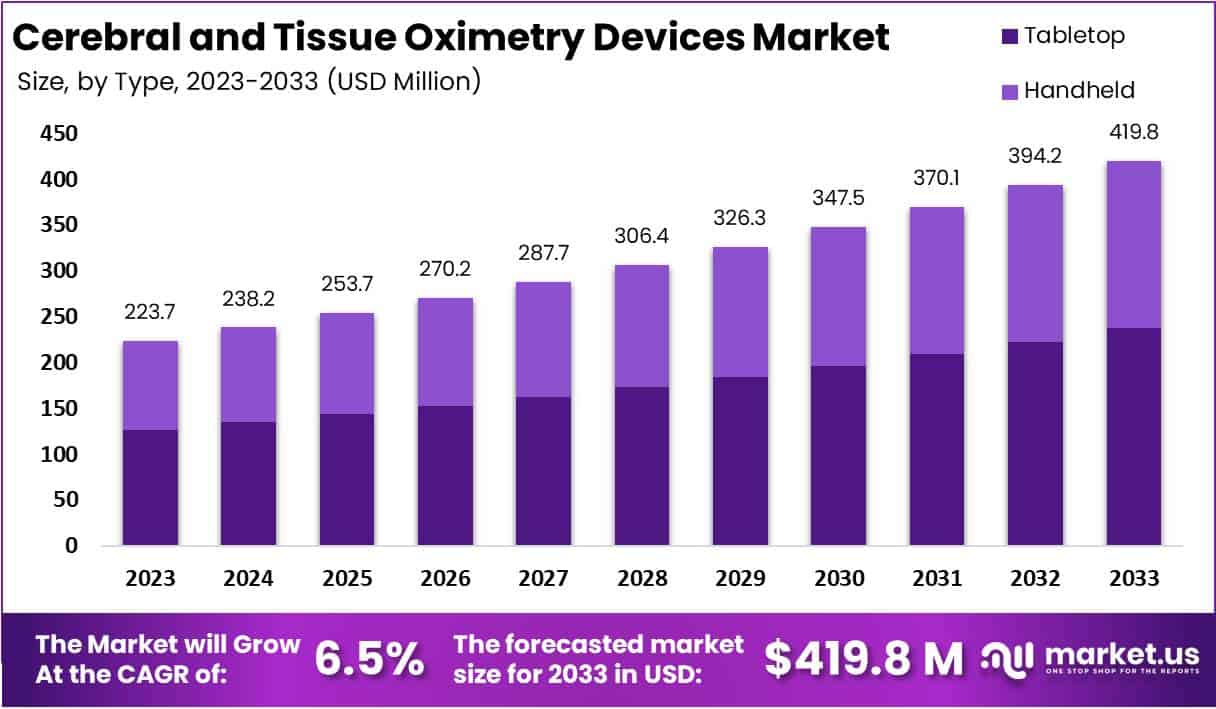

The Cerebral And Tissue Oximetry Devices Market is projected to reach approximately USD 419.8 million by 2033, up from USD 223.7 million in 2023. This reflects a compound annual growth rate (CAGR) of 6.5% from 2024 to 2033. Growth is driven by increasing clinical demand for brain oxygen monitoring to reduce neurological injuries during surgeries. Rising stroke prevalence, estimated to cost over USD 890 billion annually, reinforces the need for such monitoring solutions in hospitals and intensive care units.

Population ageing significantly contributes to market expansion. According to the World Health Organization, one in six people will be aged 60 or older by 2030, with the 80+ population expected to triple by 2050. Older patients undergoing complex surgical procedures face higher risks of hypoperfusion and cognitive complications. Hospitals are therefore adopting regional oximetry to monitor real-time tissue oxygenation during and after procedures, ensuring improved patient outcomes and reduced recovery times.

Neonatal care represents another key growth segment. In 2023, around 2.3 million newborn deaths were reported globally, with birth asphyxia as a leading cause. Continuous cerebral and somatic oximetry enables early detection of hypoxia, improving survival outcomes in neonatal intensive care units (NICUs). As healthcare systems enhance neonatal care quality, adoption of noninvasive oximetry devices continues to accelerate, particularly in emerging economies focusing on reducing infant mortality.

In trauma and peri-operative care, cerebral oximetry is increasingly recognized as essential. The U.S. Centers for Disease Control and Prevention reported over 69,000 traumatic brain injury-related deaths in 2021. Noninvasive oximetry assists clinicians in detecting cerebral hypoxia early, supporting faster stabilization in emergency settings. Additionally, peri-operative quality initiatives, such as NHS guidelines, promote near-infrared spectroscopy to prevent tissue hypoxia, driving broader adoption across cardiac, vascular, and neurosurgical procedures.

Supportive regulatory frameworks and innovation trends are further propelling the market. The FDA and MHRA have streamlined device approvals, encouraging development of advanced sensors and algorithms. Meanwhile, initiatives to improve device accuracy across skin tones are fostering equity and clinical trust. Combined with rising surgical volumes and expanding clinical evidence, these factors are expected to sustain steady growth in cerebral and tissue oximetry devices through 2033.

Key Takeaways

- The Cerebral and Tissue Oximetry Devices Market is projected to reach USD 419.8 million by 2033, registering a steady CAGR of 6.5%.

- Tabletop devices dominated in 2023 with over 56.5% market share, attributed to advanced features and ease of use in clinical environments.

- Hospitals captured 52.1% of the market in 2023, reflecting their crucial role in adopting oximetry devices for critical patient monitoring.

- Preference for tabletop devices surged in 2023, supported by their seamless clinical workflow integration and superior real-time monitoring capabilities.

- Demand for non-invasive monitoring technologies rose as clinicians prioritized safer and more comfortable oxygen saturation tracking solutions for patients.

- Technological innovations such as wireless connectivity and intelligent sensors are driving faster adoption of oximetry devices in healthcare systems.

- Rising inpatient and outpatient surgical procedures have intensified the requirement for cerebral and tissue oximetry during surgical monitoring.

- Market expansion remains restrained by high initial costs, reimbursement challenges, and occasional accuracy limitations affecting smaller healthcare facilities.

- Growth opportunities exist in neonatal care, home-based health monitoring, emerging economies, and research collaborations with medical technology innovators.

- North America led the global market in 2023, accounting for 36.5% share and USD 76.6 million in revenue, supported by strong healthcare infrastructure.

Regional Analysis

In 2023, North America dominated the Cerebral and Tissue Oximetry Devices market with a 36.5% share, valued at USD 76.6 million. This leadership was supported by the region’s advanced healthcare infrastructure, which enabled smooth integration of these devices into medical practices. The presence of highly developed hospitals, clinics, and diagnostic centers has accelerated the adoption of modern monitoring technologies, reinforcing North America’s position as the leading market for cerebral and tissue oximetry devices.

The increasing prevalence of chronic diseases, such as cardiovascular and neurological disorders, has boosted the demand for cerebral and tissue oximetry devices. These devices are crucial in tracking tissue oxygenation levels, assisting in early diagnosis and management of complex conditions. Rising awareness among healthcare professionals regarding the benefits of continuous monitoring has further fueled market adoption. Consequently, North America continues to experience high utilization rates for these devices across intensive care units and surgical settings.

Favorable reimbursement policies across the United States and Canada have significantly driven the market. The availability of coverage for procedures using cerebral and tissue oximetry devices encourages healthcare providers to adopt these technologies. This financial support reduces patient costs and improves accessibility, thereby strengthening market expansion. Moreover, the growing alignment of healthcare reforms with technology-driven care models continues to promote investments in advanced medical equipment, including oximetry systems.

Collaborations among hospitals, research institutes, and manufacturers have contributed to continuous innovation in the market. These partnerships promote research and development, ensuring a steady pipeline of technologically advanced devices. Furthermore, strict regulatory frameworks in North America enhance confidence among healthcare professionals by ensuring product safety and performance. The combined impact of regulatory compliance, innovation, and institutional support has sustained North America’s dominant position in the global cerebral and tissue oximetry devices market.

Segmentation Analysis

In 2023, the Tabletop segment dominated the Cerebral and Tissue Oximetry Devices Market with a market share exceeding 56.5%. This dominance was attributed to its easy-to-use design and advanced functionalities, making it the preferred option for healthcare professionals. Tabletop devices, designed for stable placement on surfaces, offer convenience and precision in monitoring oxygen levels. Their intuitive interfaces enhance user experience, contributing to wide adoption across hospitals and clinics seeking reliable and efficient cerebral and tissue oxygen monitoring solutions.

Tabletop oximetry devices gained popularity due to their stable performance and consistent accuracy. Healthcare practitioners preferred these devices for critical monitoring, as they ensured precise readings during surgeries and intensive care. The devices’ ergonomic design and operational simplicity allowed effortless integration into existing medical workflows. Furthermore, their technological enhancements improved diagnostic efficiency, leading to their dominance in medical facilities. As a result, the tabletop segment maintained a stronghold in the market, appealing to professionals prioritizing reliability and consistency in patient monitoring.

In contrast, the Handheld segment also achieved a substantial share of the Cerebral and Tissue Oximetry Devices Market in 2023. Its appeal stemmed from portability and operational flexibility, making it ideal for mobile healthcare settings. These compact devices provided accurate oxygen readings even in space-constrained environments. Their lightweight design and wireless capability enabled healthcare professionals to monitor patients conveniently. Although facing strong competition from tabletop devices, the handheld category remained relevant due to its adaptability and essential role in emergency and field medical scenarios.

From an end-use perspective, hospitals accounted for over 52.1% of the global market share in 2023, underscoring their leadership in adopting cerebral and tissue oximetry devices. Hospitals integrated these devices for real-time monitoring during surgeries and critical care. Their emphasis on patient safety and technology adoption strengthened market growth. Clinics and other healthcare facilities followed, exhibiting promising potential for increased usage. The market’s growth trajectory indicated that hospitals would continue to drive demand, supported by ongoing technological advancements and the growing importance of continuous patient monitoring.

Key Players Analysis

The Cerebral and Tissue Oximetry Devices Market is driven by the strategic presence of leading players such as Artinis Medical Systems, Edwards Lifesciences Corp., Hamamatsu Photonics KK, and HyperMed Imaging Inc. Their combined technological advancements and product innovations contribute significantly to market expansion. Each company focuses on enhancing patient safety, improving accuracy in oxygen monitoring, and introducing advanced non-invasive devices, thereby strengthening the global adoption of oximetry solutions across clinical and research applications.

Edwards Lifesciences Corp. remains a dominant participant in the market with a focus on patient-centric innovations. The company develops cutting-edge oximetry devices designed to optimize monitoring accuracy and patient outcomes in critical care. Its products support medical professionals in precise hemodynamic assessments. Continuous investments in R&D and product enhancement have positioned Edwards Lifesciences as a vital contributor to advancing cerebral and tissue oxygen monitoring technologies worldwide.

Hamamatsu Photonics KK brings specialized expertise in photonics technology to the oximetry sector. The company integrates optical precision into its oximetry devices, allowing real-time, high-accuracy tissue oxygenation assessments. Its focus on innovation through optical sensor development enhances clinical decision-making and diagnostic accuracy. Hamamatsu’s technological leadership underscores the value of diverse engineering approaches in improving medical imaging and oxygen monitoring capabilities across various healthcare settings.

HyperMed Imaging Inc. plays an essential role in expanding the capabilities of tissue oximetry through hyperspectral imaging solutions. By merging imaging and oximetry technologies, the company provides comprehensive insights into tissue perfusion and oxygenation. This integrated approach improves diagnostic visualization and patient assessment accuracy. Alongside other industry leaders such as Masimo Corp., Medtronic Plc, and Nonin Medical Inc., HyperMed Imaging contributes to a competitive market environment that drives innovation, product quality, and technological advancement in the global oximetry landscape.

FAQ

Cerebral and Tissue Oximetry Devices – Product FAQs

1. What are Cerebral and Tissue Oximetry Devices?

Cerebral and tissue oximetry devices are non-invasive tools used to measure oxygen levels in brain and body tissues. They work using near-infrared spectroscopy (NIRS) to track real-time oxygen saturation. These devices help doctors identify oxygen imbalances quickly. They are especially useful during surgeries and in critical care units. By monitoring oxygen supply and demand, these systems help prevent hypoxia and improve patient outcomes. Their continuous monitoring supports safer and more effective clinical decisions.

2. How do these devices work?

Cerebral and tissue oximetry devices use near-infrared light to pass through biological tissues. The light reflects differently based on oxygen levels in the blood. The device sensors read these signals to calculate oxygen saturation. This technology offers real-time, continuous monitoring of tissue oxygenation. It allows doctors to detect changes early and respond quickly. The system is painless, fast, and reliable. It helps improve patient safety in both surgical and critical care environments.

3. What are the primary applications of these devices?

These devices are used across several clinical areas, including cardiac surgeries, neonatal care, trauma treatment, and neurosurgery. They help in monitoring oxygen levels in real-time during operations. In neonatal intensive care units, they detect early signs of oxygen deficiency. In trauma care, they guide rapid interventions. Their application supports better decision-making, reduces the risk of brain injury, and enhances surgical outcomes. Continuous monitoring also helps improve recovery and prevent long-term complications in patients.

4. What is the difference between cerebral oximetry and tissue oximetry?

Cerebral oximetry measures oxygen saturation in the brain, while tissue oximetry monitors it in muscles and other body regions. Both use near-infrared light to detect oxygen levels. Cerebral oximetry focuses on brain health during surgeries and critical care. Tissue oximetry, on the other hand, is used to monitor localized tissue oxygenation. Together, they give a complete view of the patient’s oxygen balance. These methods help reduce hypoxic injuries and support accurate clinical decisions.

5. What types of technologies are used in these devices?

Most devices use near-infrared spectroscopy (NIRS) to measure oxygen levels. Some advanced models use spatially resolved spectroscopy and multi-distance sensors for better accuracy. These technologies analyze how light interacts with blood to calculate oxygenation. They offer continuous, real-time results without requiring blood samples. The systems are non-invasive, reliable, and easy to use. Constant improvements in sensor design and signal processing have enhanced precision, making these technologies vital in modern patient monitoring.

6. What are the major advantages of using these devices?

Cerebral and tissue oximetry devices offer continuous and non-invasive oxygen monitoring. They allow early detection of oxygen drops, reducing the risk of brain or tissue injury. Their data helps clinicians make quick and informed decisions. These devices improve surgical safety, reduce postoperative complications, and support better recovery. They also eliminate the need for repeated blood tests. Overall, they help improve patient outcomes by ensuring stable oxygen balance and preventing unnoticed hypoxia during critical procedures.

7. What are the limitations of cerebral and tissue oximetry devices?

These devices have a few limitations. Near-infrared light has limited depth, which restricts measurement in deep tissues. Skin color, fat levels, and ambient light can affect accuracy. Calibration can vary among patients, especially in complex cases. The devices also require stable positioning for consistent readings. Despite these limits, they remain valuable for continuous oxygen monitoring. Their benefits in reducing hypoxic events and guiding timely interventions outweigh these technical challenges in clinical practice.

8. Who are the key end-users of these devices?

Hospitals, ambulatory surgical centers, and trauma units are the main users of cerebral and tissue oximetry devices. They are widely used in operating rooms and intensive care units for continuous monitoring. Neonatal and pediatric centers use them to track oxygen levels in newborns. Research institutions also use them to study oxygen dynamics in various tissues. Their growing adoption across clinical settings shows their reliability and accuracy in supporting better patient care and clinical decision-making.

9. Which companies manufacture cerebral and tissue oximetry devices?

Leading manufacturers include Medtronic plc, Edwards Lifesciences, Masimo Corporation, Hamamatsu Photonics, Nonin Medical, and ISS Inc. These companies focus on innovation, clinical validation, and user-friendly designs. They invest heavily in research to improve accuracy and device connectivity. Many also offer integrated systems that link with hospital monitoring networks. The presence of established players ensures technological advancements, strong regulatory compliance, and global availability. Their continued innovation drives growth in this specialized medical device segment.

10. Are these devices approved by regulatory bodies?

Yes, most cerebral and tissue oximetry devices are approved by global regulatory authorities. They hold certifications such as FDA clearance and CE Mark for clinical use. These approvals confirm the devices meet strict safety and performance standards. Regulatory acceptance has increased their adoption in hospitals and surgical centers. Continuous updates in compliance requirements ensure better device quality and patient safety. Manufacturers maintain these standards through clinical testing and consistent technological improvement in their products.

Cerebral and Tissue Oximetry Devices Market – Market FAQs

1. What is the current size of the Cerebral and Tissue Oximetry Devices Market?

As of 2025, the global market for cerebral and tissue oximetry devices is valued between USD 253.7 million. This market shows steady expansion as healthcare systems adopt more advanced patient monitoring solutions. Increasing surgical volumes and demand for precision care drive this growth. Hospitals and clinics are also investing in real-time monitoring technology. The growing need for safer, data-driven healthcare supports strong market performance across major regions worldwide.

2. What is the expected market growth rate?

The global cerebral and tissue oximetry devices market is expected to grow at a compound annual growth rate (CAGR) of around 6.5%. This growth is supported by increased use in hospitals and surgical centers. Advancements in near-infrared spectroscopy and rising awareness about non-invasive monitoring also contribute. Demand for continuous oxygen tracking in critical care settings is increasing. These factors are expected to maintain consistent growth in the coming years.

3. What are the key factors driving market growth?

Several factors drive the growth of this market. Rising cases of cardiovascular and neurological diseases have increased the need for real-time oxygen monitoring. More surgical procedures and intensive care cases require these devices. Technological advancements have improved accuracy and portability. Healthcare providers are focusing on patient safety and early diagnosis. Growing awareness among medical professionals and improved reimbursement policies are also contributing to higher adoption and market expansion globally.

4. Which regions dominate the market?

North America leads the global market due to its advanced healthcare infrastructure and strong research base. The United States accounts for a major share with wide adoption in hospitals and surgical centers. Europe follows closely, driven by high demand for precision monitoring during surgeries. The Asia-Pacific region is projected to grow the fastest, supported by rising healthcare investments and an expanding patient base. Developing countries are becoming key growth areas for future expansion.

5. What are the major market challenges?

High device costs remain a primary challenge in this market. Limited reimbursement in some regions restricts adoption. Technical challenges, such as accuracy variations among patient groups, also affect market growth. In developing countries, lack of awareness and trained staff limits use. Despite these barriers, ongoing research and cost-effective solutions are improving accessibility. As technology evolves, these challenges are expected to reduce, supporting broader acceptance of oximetry devices in clinical care.

6. What are the major trends shaping the market?

The market is moving toward smart, portable, and wireless oximetry systems. Integration with digital health platforms allows remote and continuous monitoring. Artificial intelligence and data analytics are being used for predictive insights. Growing use in neonatal and pediatric care is another key trend. Wearable oximetry solutions are gaining attention for home monitoring. These trends show how innovation and digital integration are transforming patient monitoring and enhancing the efficiency of healthcare delivery globally.

7. What segments does the market consist of?

The market is divided by product type, end-user, and region. Product segments include cerebral oximeters and tissue oximeters. End-users include hospitals, ambulatory centers, and specialty clinics. Regionally, the market covers North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Each segment shows unique growth patterns depending on healthcare infrastructure and investment levels. This segmentation helps manufacturers and investors identify high-potential areas for market expansion and targeted product development.

8. Who are the leading market players?

Key market players include Medtronic plc, Edwards Lifesciences, Masimo Corporation, Nonin Medical, Hamamatsu Photonics, and Moor Instruments. These companies lead through technological innovation and strong global distribution networks. Their focus on product accuracy, wireless integration, and clinical validation drives competitiveness. Partnerships and acquisitions are common strategies to expand market presence. Continuous R&D investments help improve performance and user experience, strengthening these firms’ positions in the global oximetry devices market.

9. What opportunities exist for new entrants?

New entrants can focus on affordable and portable oximetry devices for emerging markets. Developing AI-powered systems for predictive monitoring offers high potential. Startups can also explore integration with telehealth and remote patient monitoring platforms. There is growing demand in Asia, Latin America, and Africa. Innovation in design, data analytics, and connectivity can create competitive advantages. By targeting cost-efficiency and accuracy, new players can establish strong positions in this expanding global healthcare segment.

10. How has COVID-19 impacted the market?

The COVID-19 pandemic initially slowed elective surgeries but highlighted the value of non-invasive monitoring. Hospitals adopted cerebral and tissue oximetry devices to manage oxygen-related complications. As the healthcare system adapted, demand for continuous oxygen monitoring increased. The pandemic also accelerated digital health adoption, supporting remote monitoring integration. Post-pandemic recovery of surgical volumes has further boosted market growth. Overall, the pandemic positively influenced long-term adoption and innovation in this medical device category.

Conclusion

The cerebral and tissue oximetry devices market is expected to grow steadily, driven by increasing demand for accurate and non-invasive monitoring solutions in healthcare. The rise in complex surgeries, aging populations, and focus on neonatal care are key factors supporting market expansion. Continuous technological improvements, including advanced sensors and wireless systems, are enhancing device efficiency and usability. Growing awareness among clinicians about real-time oxygen monitoring further accelerates adoption. Although high costs and accuracy limitations remain challenges, innovation, supportive regulations, and strong healthcare infrastructure are expected to maintain positive market momentum, positioning cerebral and tissue oximetry devices as essential tools in modern clinical care.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)