Table of Contents

Overview

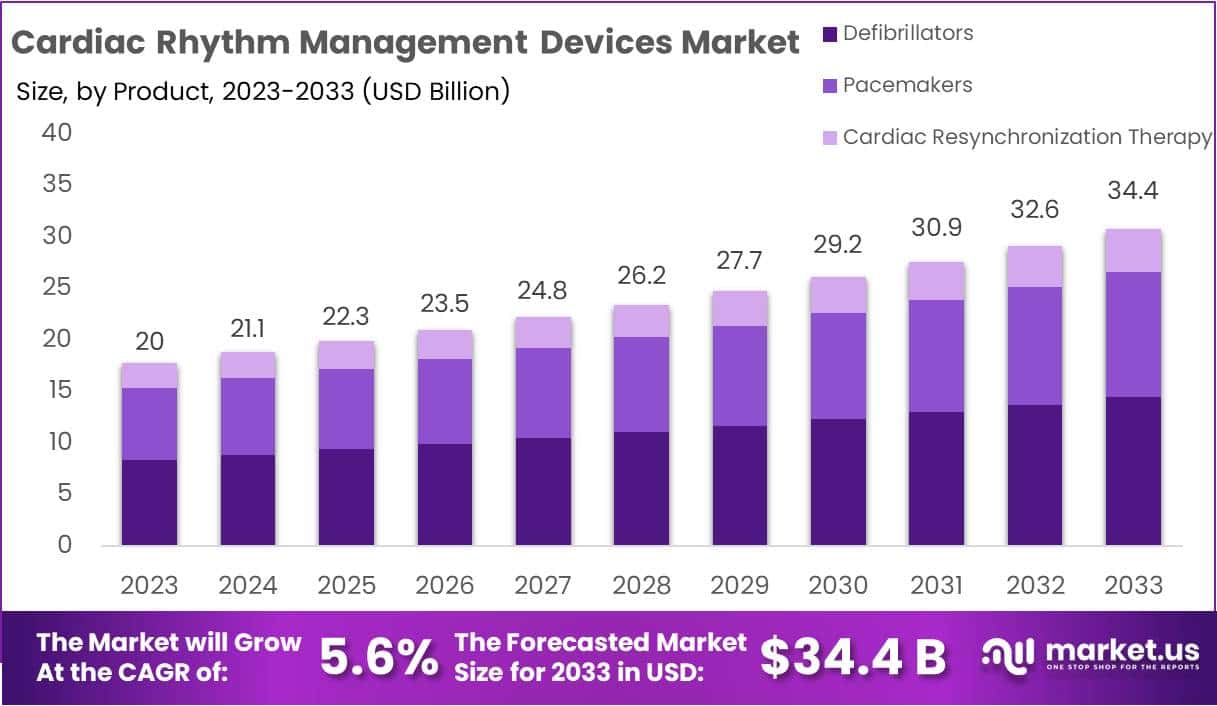

The Global Cardiac Rhythm Management (CRM) Devices Market is projected to grow from USD 20 billion in 2023 to approximately USD 34.4 billion by 2033. This reflects a compound annual growth rate (CAGR) of 5.6% during the forecast period. Growth is strongly supported by the persistent burden of cardiovascular diseases, which remain the leading cause of death worldwide. According to the World Health Organization, around 19.8 million people died in 2022 due to heart attacks and strokes, ensuring sustained demand for CRM devices.

Pacemakers, implantable cardioverter-defibrillators (ICDs), and cardiac resynchronization therapy (CRT) systems are crucial in preventing sudden cardiac death and correcting rhythm disorders. Their clinical relevance is reinforced by the rising prevalence of atrial fibrillation, conduction diseases, and heart failure. Increasing incidence rates translate into a steady requirement for new implants and replacement cycles. These devices are life-sustaining interventions, and their consistent demand is tied directly to global epidemiological patterns and rising chronic disease prevalence.

Ageing demographics represent a critical driver of the CRM devices market. United Nations data indicate that the share of the global population aged 65 years and older is expected to rise significantly over the next three decades. This demographic shift expands the addressable patient pool, as elderly individuals are disproportionately affected by heart rhythm disorders and heart failure. The ageing trend is therefore increasing both the volume of device implants and the replacement cycle demand, since patients are living longer with chronic conditions.

Policy frameworks and clinical guidelines are also accelerating adoption. In the United Kingdom, the National Institute for Health and Care Excellence (NICE) recommends ICDs and CRTs for patients with defined criteria, anchoring evidence-based practice within the National Health Service. In the United States, Medicare provides reimbursement codes for device checks and remote interrogations, ensuring financial clarity. Such structured frameworks create consistent clinical uptake while minimizing uncertainty for healthcare providers and payers. This institutional backing strengthens confidence in adoption across high-income markets.

Technological Innovation and Market Enablers

The CRM devices sector is also benefitting from rapid technological advancements. Miniaturized and leadless pacemakers approved by the U.S. Food and Drug Administration reduce the need for surgical pockets and transvenous leads. MRI-conditional labeling allows patients safe access to critical diagnostic imaging. These features improve patient acceptance and expand eligibility. Innovation is lowering barriers to treatment, reducing complication risks, and supporting the broader use of advanced devices, thereby strengthening overall market penetration.

Remote monitoring has transitioned from optional to routine follow-up care for patients with implanted devices. Evidence shows that remote systems detect complications earlier, reduce unnecessary in-person visits, and enable timely therapy adjustments. National health systems and hospital networks now regard remote monitoring as a standard of care. In the United States, Medicare has introduced reimbursement policies for remote interrogations, which further increases long-term service revenue streams. These practices improve patient management and enhance the economic viability of device therapies.

Underlying disease trends further strengthen the case for expansion. Rising rates of atrial fibrillation and heart failure have been documented across multiple geographies. These conditions create continuous demand for rhythm management interventions and resynchronization therapies. Global statistical reviews confirm that the prevalence of these conditions is unlikely to decline, ensuring durable growth in implant volumes and replacements. Sustained epidemiological pressure ensures that demand will remain robust across both developed and emerging markets.

Health spending patterns are another supportive factor. According to OECD reports, per-capita healthcare expenditure continues to grow across high-income economies. The United States and several OECD countries maintain healthcare spending at high levels as a share of GDP. Such financial stability enables both public and private payers to fund device therapy and associated infrastructure, including follow-up platforms and monitoring systems. In combination, demographic, epidemiological, technological, and macroeconomic factors are reinforcing long-term expansion prospects in the CRM devices sector.

Key Takeaways

- The cardiac rhythm management devices market is forecasted to reach USD 34.4 billion by 2033, expanding steadily at a CAGR of 5.6%.

- In 2023, defibrillators held the leading 41.5% market share, supported by growing demand for effective solutions to life-threatening cardiac arrhythmias worldwide.

- Arrhythmias dominated the application segment with 26.4% share in 2023, underscoring strong demand for addressing irregular heartbeat conditions across global patient populations.

- Hospitals and clinics accounted for more than 48.7% of end-user share in 2023, highlighting their central role in advanced cardiac care delivery.

- North America led the global market in 2023 with a 39.8% share, supported by robust healthcare infrastructure and favorable regulatory frameworks.

- Prominent players include Physio-Control Inc. (Stryker), Schiller, Medtronic, Abbott, Boston Scientific, Philips, Zoll, BIOTRONIK, Progetti Srl, and LivaNova Plc.

- The global cardiac rhythm management devices market was valued at USD 20 billion in 2023, reflecting its substantial size and strategic healthcare significance.

- Technological advancements such as leadless pacemakers and wearable cardiac monitoring devices continue transforming treatment outcomes and minimizing patient complications.

- Europe and Asia-Pacific are projected to witness considerable growth, driven by rising healthcare expenditure and increasing geriatric populations across both regions.

Regional Analysis

In 2023, North America dominated the cardiac rhythm management devices market with a share exceeding 39.8%. The market value reached USD 7.96 billion, highlighting its strong global position. The dominance of the region is supported by advanced healthcare infrastructure and a high prevalence of cardiovascular diseases. The United States played a key role with its developed healthcare system and large patient population. Furthermore, an efficient regulatory framework and rising awareness among patients and professionals enhanced the adoption of innovative technologies in the region.

North America’s leadership was further strengthened by collaborations between leading manufacturers and healthcare institutions. These strategic partnerships encouraged the development of technologically advanced cardiac rhythm management devices. Such efforts ensured smooth innovation and rapid penetration in the market. Healthcare providers in the region increasingly integrated next-generation devices into treatment practices. These advances reflect the region’s commitment to adopting medical innovations that improve patient outcomes. The synergy between industry players and medical institutions supported steady growth momentum in 2023.

While North America held a dominant position, Europe and Asia-Pacific are expected to witness strong growth. Europe benefits from rising healthcare expenditure, an aging population, and increasing focus on preventive measures. Asia-Pacific is experiencing accelerated adoption due to expanding healthcare infrastructure, higher disposable incomes, and growing awareness of cardiac health. The region’s vast and aging population presents lucrative opportunities for manufacturers. Both regions are expected to emerge as attractive growth destinations, making them vital for global players seeking to expand their market footprint.

Segmentation Analysis

In 2023, the cardiac rhythm management devices market was led by defibrillators, which captured a market share exceeding 41.5%. This dominance was due to their critical role in preventing sudden cardiac arrests and improving survival rates. Defibrillators, designed to restore normal heart rhythm through electrical shocks, gained strong adoption with technological advancements making them more efficient and user-friendly. Pacemakers also maintained a strong position, addressing irregular heartbeats and contributing significantly to the management of bradycardia and other cardiac rhythm disorders.

Applications of cardiac rhythm management devices showed diverse contributions in 2023, with arrhythmias securing over 26.4% of the market share. The rising prevalence of arrhythmias and growing awareness of treatment options strengthened this segment. Congestive heart failure also demonstrated significant uptake, supported by the increasing cases of heart failure and the effectiveness of these devices in managing the condition. Additionally, bradycardia and tachycardia applications showed consistent demand, reinforcing the versatility of these devices in addressing multiple cardiac health issues across patient populations.

From an end-user perspective, hospitals and clinics emerged as the leading segment, holding over 48.7% of the market share in 2023. Their dominance stemmed from their role as primary healthcare providers offering comprehensive cardiac care. Ambulatory surgical centers also gained prominence by catering to outpatient cardiac procedures, reflecting a steady growth trend. Other end-users, including specialized clinics, contributed further to the overall expansion. Continuous technological innovations and the rising burden of cardiac disorders are expected to sustain growth across all segments, with hospitals and clinics maintaining their leading role in the near future.

Key Players Analysis

Physio-Control Inc. (Stryker) has established a strong presence in the Cardiac Rhythm Management Devices Market. The company delivers advanced defibrillators and monitoring devices designed for precision and ease of use. Its focus on user-friendly technology supports healthcare professionals in providing efficient cardiac care. This commitment to innovation and quality has positioned Stryker as a trusted leader. By consistently upgrading its portfolio, the company contributes significantly to the global adoption of cardiac rhythm management solutions, driving growth across multiple healthcare settings.

Schiller is recognized for its reliable cardiac monitoring solutions and emphasis on diagnostic accuracy. Its product portfolio includes advanced ECG systems that ensure timely identification of cardiac conditions. Schiller’s dedication to innovation and quality positions the company as a dependable partner for healthcare providers. The precision embedded in its devices enhances clinical outcomes and patient safety. This reliability strengthens Schiller’s reputation in the industry. Its consistent product development strategy ensures steady growth in the cardiac rhythm management devices market worldwide.

Medtronic and Abbott dominate the market through diverse and innovative product offerings. Medtronic leads with implantable devices and continuous monitoring systems that set industry standards. Its research-driven strategies and collaborations reinforce its leadership role. Abbott, on the other hand, focuses on integrating advanced technology with patient-centric designs. Its pacemakers and implantable defibrillators cater to varied patient needs. Both companies leverage global networks to ensure accessibility. Their combined impact shapes market competitiveness, fosters innovation, and supports improved outcomes in cardiac healthcare delivery across key regions.

FAQ

1. What are cardiac rhythm management devices?

Cardiac rhythm management devices are medical devices that help regulate abnormal heartbeats known as arrhythmias. They include pacemakers, implantable cardioverter defibrillators (ICDs), and cardiac resynchronization therapy (CRT) devices. These devices deliver electrical impulses to the heart when its natural rhythm is too slow, too fast, or irregular. By doing so, they restore proper heartbeat function and improve overall heart performance. They are widely used in patients with heart failure, sudden cardiac arrest risk, or severe arrhythmia conditions.

2. What types of CRM devices are available?

CRM devices fall into three major categories. Pacemakers are used to correct slow heart rhythms by sending small electrical pulses. Implantable cardioverter defibrillators (ICDs) are designed to prevent sudden death by delivering strong shocks during dangerous fast rhythms. Cardiac resynchronization therapy (CRT) devices are implanted in patients with heart failure to improve the heart’s pumping efficiency. Each device serves a unique purpose and is prescribed based on patient conditions, heart function, and the severity of rhythm abnormalities.

3. How do CRM devices work?

CRM devices monitor the electrical signals of the heart and deliver electrical pulses when needed. Pacemakers send gentle signals to maintain steady rhythms in cases of slow heartbeat. ICDs continuously track heart activity and deliver powerful shocks if life-threatening arrhythmias occur. CRT devices coordinate the contractions of both heart ventricles to improve pumping efficiency. These devices are small, battery-powered, and implanted under the skin. Their primary function is to restore heart rhythm balance and help prevent serious cardiac complications.

4. Who requires CRM devices?

CRM devices are recommended for patients diagnosed with certain cardiac disorders. Those with bradycardia, which causes slow heartbeats, often need pacemakers. People at high risk of sudden cardiac arrest, particularly due to ventricular fibrillation or tachycardia, are prescribed ICDs. Patients with heart failure and abnormal electrical signaling in the ventricles benefit from CRT devices. Doctors assess medical history, symptoms, and heart test results before recommending an implant. These devices are vital in reducing risks and improving patient quality of life.

5. Are CRM devices safe and effective?

CRM devices are clinically proven to be safe and effective in restoring heart rhythms. Pacemakers reduce symptoms of bradycardia and improve exercise tolerance. ICDs significantly lower the risk of sudden cardiac death by intervening during dangerous arrhythmias. CRT devices help heart failure patients live longer and healthier lives. Although complications like infection, bleeding, or lead displacement may occur, these risks are rare. Overall, these devices improve survival rates, reduce hospitalizations, and enhance the quality of life for heart patients.

6. What are the recent advancements in CRM devices?

Recent advancements in CRM devices focus on safety, comfort, and connectivity. MRI-compatible pacemakers and defibrillators allow patients to undergo MRI scans safely. Leadless pacemakers eliminate surgical leads, reducing complications. Subcutaneous ICDs are placed under the skin, avoiding insertion into veins. Remote monitoring technology enables doctors to track device performance and patient data in real time. Many devices now include smart features powered by advanced software. These innovations improve patient outcomes, reduce follow-up visits, and simplify cardiac rhythm management.

7. What is the average lifespan of CRM devices?

The average lifespan of CRM devices depends on the type and usage. Pacemakers usually last between 5 and 15 years. ICDs function for about 5 to 7 years, while CRT devices last between 5 and 10 years. Battery depletion is the main reason for replacement. Modern devices use advanced lithium batteries to extend service life. When batteries run low, minor surgery is needed for replacement. Device performance and lifespan also depend on patient condition and how often electrical therapy is delivered.

8. What are the risks or complications?

CRM devices are generally safe, but some risks and complications may occur. Common issues include infection at the implant site, bleeding, or swelling. In rare cases, device leads may dislodge or break, requiring correction. ICDs may sometimes deliver unnecessary shocks, although modern algorithms reduce this risk. Device malfunction is uncommon due to strict safety standards. Regular medical follow-ups ensure proper function and early detection of issues. Despite potential risks, the overall benefits of CRM devices outweigh the possible complications.

9. How large is the CRM devices market?

The Cardiac Rhythm Management Devices Market Size is anticipated to reach approximately USD 34.4 Billion by 2033, exhibiting substantial growth from USD 20 Billion in 2023. This represents a compound annual growth rate (CAGR) of 5.6% during the forecast period spanning from 2024 to 2033. Growth is driven by rising heart disease cases, an aging global population, and demand for advanced medical devices. Increasing awareness of heart health and healthcare investments further support market expansion. Overall, the market outlook remains stable and positive.

10. What are the main growth drivers?

Several factors are driving the growth of the CRM devices market. The increasing prevalence of heart failure and arrhythmias is a key driver. Rising healthcare spending and the growing elderly population are boosting demand. Technological advancements such as leadless pacemakers, remote monitoring, and MRI-compatible devices also support adoption. Greater awareness of sudden cardiac death risks is influencing treatment decisions. In addition, government programs promoting healthcare access in developing regions contribute to the strong growth of CRM device sales worldwide.

11. Which regions dominate the CRM market?

North America holds the largest share of the CRM devices market due to advanced healthcare infrastructure and high adoption rates. Europe follows closely, supported by an aging population and strong medical device penetration. The Asia-Pacific region is growing fastest, fueled by large patient populations, rising healthcare investments, and improved access to treatments. Emerging economies like India and China are key contributors to this growth. Latin America and the Middle East also show increasing demand, driven by expanding healthcare systems.

12. Who are the leading market players?

The CRM devices market is led by several multinational companies. Physio-Control Inc. (Stryker), Schiller, Medtronic, Abbott, Boston Scientific Corporation, Koninklijke Philips N.V., Zoll Medical Corporation, BIOTRONIK, Progetti Srl, LivaNova Plc, Other Key Players. Competition in the market is intense, with companies focusing on miniaturization, safety, and smart device capabilities. Continuous investments in research and development ensure these players maintain leadership in the cardiac rhythm management sector.

13. What challenges does the market face?

The CRM devices market faces several challenges despite strong demand. High device costs limit adoption, especially in developing countries with restricted healthcare budgets. Reimbursement policies vary widely, which affects patient access. Device-related complications or recalls can harm market growth. Competition from alternative treatments like catheter ablation is increasing. Regulatory approval processes are also complex and time-consuming. These factors can delay product launches and limit availability. Addressing affordability and improving reimbursement policies will be essential to overcome these challenges.

14. What are the emerging trends in the market?

Emerging trends in the CRM devices market focus on innovation and patient convenience. Leadless pacemakers and subcutaneous defibrillators are gaining popularity due to reduced surgical risks. Remote monitoring systems allow physicians to track patients and device performance in real time. Artificial intelligence is being integrated into devices for predictive analytics and early detection of heart problems. There is also a shift toward value-based healthcare, which emphasizes improved outcomes and cost-effectiveness. These trends are shaping the next phase of market growth.

15. How is the post-COVID-19 scenario influencing the market?

The COVID-19 pandemic had a temporary negative effect on the CRM devices market, as elective surgeries were delayed worldwide. However, the market is recovering with increased focus on remote monitoring solutions. The crisis highlighted the importance of digital health technologies in managing chronic conditions. Hospitals and clinics are now adopting telemedicine and digital connectivity at a faster pace. This shift has created long-term opportunities for CRM devices with smart monitoring features. The post-COVID market environment is more technology-driven and patient-focused.

16. What is the future outlook of the CRM market?

The future of the CRM devices market appears promising, with steady growth expected. Rising global cases of cardiovascular disease will keep demand strong. Continuous innovation, such as miniaturized devices and AI integration, will improve adoption. The expansion of healthcare access in emerging markets will further fuel growth. Companies will likely focus on smart and connected devices, creating new opportunities. Although cost and regulatory challenges remain, long-term prospects suggest sustainable development and positive momentum for the global CRM devices market.

Conclusion

The global cardiac rhythm management devices market shows steady and positive growth. Demand is supported by the high burden of cardiovascular diseases, ageing populations, and continuous technological progress. Advancements such as leadless pacemakers, MRI-compatible devices, and remote monitoring are transforming treatment outcomes and improving patient care. North America leads due to strong infrastructure, while Europe and Asia-Pacific are emerging as high-growth regions. Despite challenges like cost and reimbursement barriers, long-term prospects remain favorable. Strong industry competition, innovation, and rising healthcare investments will keep shaping the market, ensuring that cardiac rhythm management devices remain an essential part of advanced heart care worldwide.

View More Related Reports Here:

Cardiac Biomarkers Market || Cardiac Resynchronization Therapy Market || Cardiac Ultrasound Systems Market || Cardiac Safety Services Market || Remote Cardiac Monitoring Market || Cardiac Arrhythmia Monitoring Devices Market

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)