Table of Contents

Overview

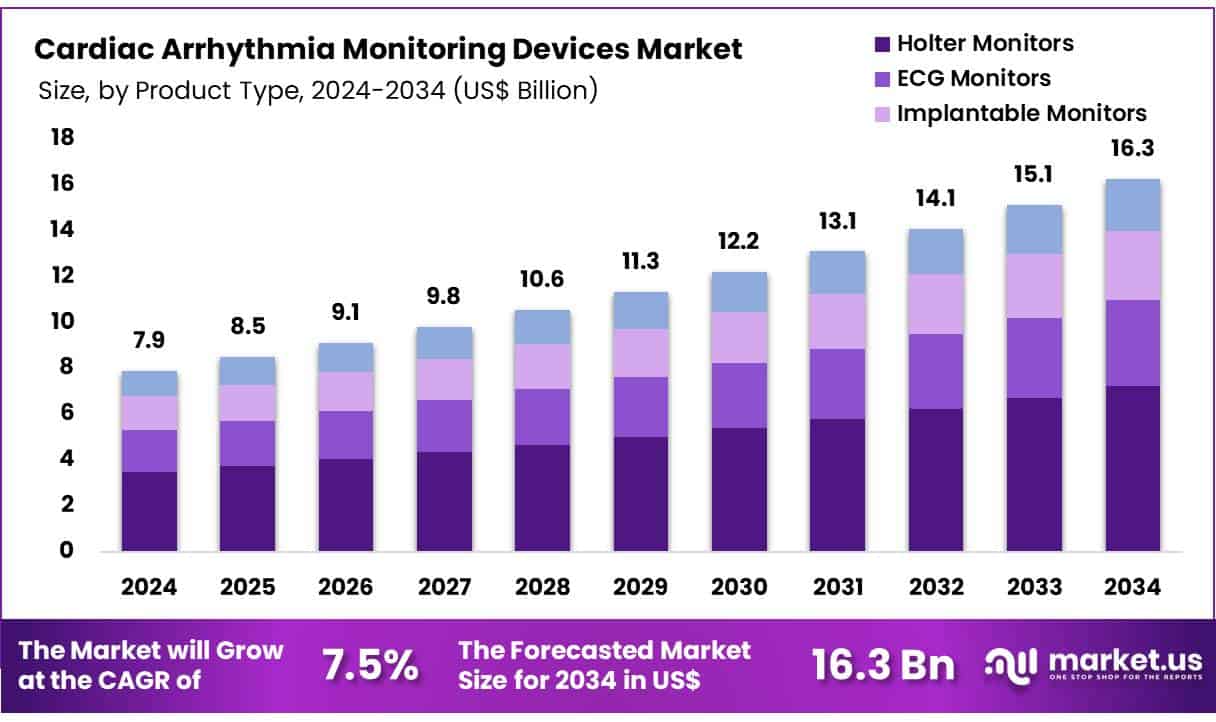

New York, NY – June 30, 2025 – The Global Cardiac Arrhythmia Monitoring Devices Market size is expected to be worth around US$ 16.3 billion by 2034 from US$ 7.9 billion in 2024, growing at a CAGR of 7.5% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 39.4% share with a revenue of US$ 3.1 Million.

The global Cardiac Arrhythmia Monitoring Devices Market is expected to witness steady growth over the forecast period, driven by the increasing prevalence of cardiovascular diseases, particularly atrial fibrillation and other rhythm disorders. These devices play a crucial role in the early detection and continuous monitoring of abnormal heart rhythms, enabling timely diagnosis and reducing the risk of complications such as stroke and heart failure.

Advancements in monitoring technologies such as wireless ECG patches, implantable loop recorders, and mobile cardiac telemetry have improved diagnostic accuracy and patient comfort. The integration of artificial intelligence and cloud-based systems has further enhanced data analysis, allowing healthcare professionals to make more informed decisions. The demand for home-based and wearable arrhythmia monitors is also increasing, fueled by the shift toward remote patient monitoring and telehealth services.

North America currently holds a dominant position in the market, supported by well-established healthcare systems and rising adoption of digital health tools. However, the Asia-Pacific region is expected to register the fastest growth due to increasing healthcare awareness, expanding access to medical devices, and supportive government initiatives for cardiac health screening.

The market is further supported by ongoing research, favorable regulatory developments, and increasing public and private investment in cardiovascular diagnostics and digital health infrastructure.

Key Takeaways

- In 2023, the cardiac arrhythmia monitoring devices market generated a revenue of US$ 7.9 billion, growing at a compound annual growth rate (CAGR) of 7.5%. The market is projected to reach approximately US$ 16.3 billion by 2033.

- By product type, the market is segmented into Holter monitors, ECG monitors, implantable monitors, and mobile cardiac telemetry. Among these, Holter monitors emerged as the leading segment in 2023, accounting for a 44.3% market share.

- In terms of application, the market is categorized into atrial fibrillation, bradycardia, tachycardia, ventricular fibrillation, premature contraction, and others. Atrial fibrillation was the dominant application segment, holding a 36.4% share in 2023.

- With respect to end users, the market includes hospitals and clinics, ambulatory centers, diagnostic centers, and others. The hospitals and clinics segment accounted for the highest revenue contribution, representing 41.2% of the market share.

- Regionally, North America led the global market in 2023, securing a 39.4% share, supported by advanced healthcare infrastructure, high disease prevalence, and rapid adoption of monitoring technologies.

Segmentation Analysis

- Product Type Analysis: Holter monitors accounted for 44.3% of the market due to their reliability, ease of use, and ability to offer continuous 24–48 hour monitoring. The increasing prevalence of arrhythmias and demand for ambulatory cardiac diagnostics support this segment’s growth. Their affordability compared to implantable devices and compatibility with remote monitoring platforms also contribute to adoption. Rising geriatric populations and patient awareness of early detection further enhance the segment’s market potential in both hospital and outpatient settings.

- Application Analysis: Atrial fibrillation represented a 36.4% market share, driven by rising global cases linked to hypertension, obesity, and diabetes. The condition’s strong association with stroke risk makes early diagnosis critical, increasing demand for real-time heart rhythm monitoring devices. Advancements in wearable and implantable technologies tailored for atrial fibrillation support wider adoption. Additionally, proactive health screening, growing geriatric populations, and the need for personalized treatment are expected to fuel sustained growth in this application segment.

- End-User Analysis: Hospitals and clinics held 41.2% of the market, supported by their focus on comprehensive cardiac care and investment in advanced diagnostics. These facilities benefit from integrated infrastructures and skilled professionals, enabling effective arrhythmia detection and management. Clinics also prefer portable monitors for outpatient care. Government initiatives, favorable reimbursement, and increased use of telehealth technologies further drive device procurement. Growing patient volumes and industry collaborations enhance access to cutting-edge monitoring tools, reinforcing demand in this segment.

Market Segments

Product Type

- Holter Monitors

- ECG Monitors

- Implantable Monitors

- Mobile Cardiac Telemetry

Application

- Atrial Fibrillation

- Bradycardia

- Tachycardia

- Ventricular Fibrillation

- Premature Contraction

- Others

End-user

- Hospitals and Clinics

- Ambulatory Centers

- Diagnostic Centers

- Others

Regional Analysis

North America led the global cardiac arrhythmia monitoring devices market, accounting for the largest revenue share of 39.4%. This dominance is attributed to the high prevalence of cardiac arrhythmias, particularly atrial fibrillation. According to the Centers for Disease Control and Prevention (CDC), approximately 12.1 million individuals in the U.S. are projected to be affected by atrial fibrillation by 2030. This growing patient base necessitates advanced cardiac monitoring solutions.

Moreover, technological innovations such as wearable monitors and extended-use implantable devices are supporting widespread adoption. The presence of a well-established healthcare infrastructure and strong clinical awareness further promotes early diagnosis and continuous monitoring in the region.

In contrast, the Asia Pacific region is anticipated to register the fastest compound annual growth rate (CAGR) over the forecast period. Factors such as a growing geriatric population, increasing prevalence of cardiovascular diseases, and rising awareness are key contributors. Enhanced healthcare infrastructure, government initiatives for cardiac health, and the adoption of telehealth services are driving regional expansion. The Asia Pacific Heart Rhythm Society (APHRS) supports widespread atrial fibrillation screening, which is expected to further increase the use of arrhythmia monitoring technologies across the region.

Emerging Trends

- The burden of atrial fibrillation is growing rapidly. It is estimated that 12.1 million people in the United States will have AFib by 2030, up from approximately 5 million today.

- Remote monitoring has become mainstream. Modern cardiac implantable electronic devices (CIEDs) can record detailed data on device function, arrhythmias, physiological status, and hemodynamic parameters in real time.

- Artificial intelligence is being embedded in ECG monitoring. The FDA now lists AI/ML-enabled medical devices, and services combining up to 14 days of ECG data with deep-learned algorithms have been cleared for clinical use.

- Telehealth and remote patient monitoring are now standard components of cardiac care. Following the COVID-19 pandemic, telehealth integration with arrhythmia monitoring tools has been widely adopted to enhance access and care quality.

Use Cases

- Extended ambulatory ECG monitoring is used to uncover irregular heartbeats that short tests miss. For example, a 14-day ECG patch can capture transient arrhythmias, improving detection rates by up to 30 percent compared with 24-hour Holter monitors.

- Implantable pulmonary artery sensors guide heart failure management. The CardioMEMS HF System was associated with a 37 percent reduction in heart failure hospitalizations over 15 months in NYHA Class III patients.

- Smartphone-based AF screening apps enable point-of-care detection. A finger-over-camera method requires just a 60-second recording and has gained FDA clearance for identifying atrial fibrillation.

- Hemodynamic-guided therapy via remote monitoring platforms has been shown to reduce hospitalizations. A meta-analysis of over 1,350 HFrEF patients reported a 36 percent decrease in heart failure hospital admissions at 12 months when managed by pulmonary artery pressure data.

Conclusion

The global cardiac arrhythmia monitoring devices market is poised for steady growth, driven by rising cardiovascular disease prevalence, especially atrial fibrillation. Technological advancements in wearable, implantable, and AI-enabled devices are enhancing early detection and real-time monitoring. With North America leading in adoption and Asia Pacific emerging rapidly, regional dynamics support market expansion.

Integration of telehealth and remote monitoring solutions is reshaping cardiac care delivery. Increasing patient awareness, aging populations, and supportive government initiatives further reinforce demand. As clinical outcomes improve through continuous innovation, cardiac arrhythmia monitoring devices are expected to play a critical role in personalized and preventive cardiovascular care.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)