Table of Contents

Overview

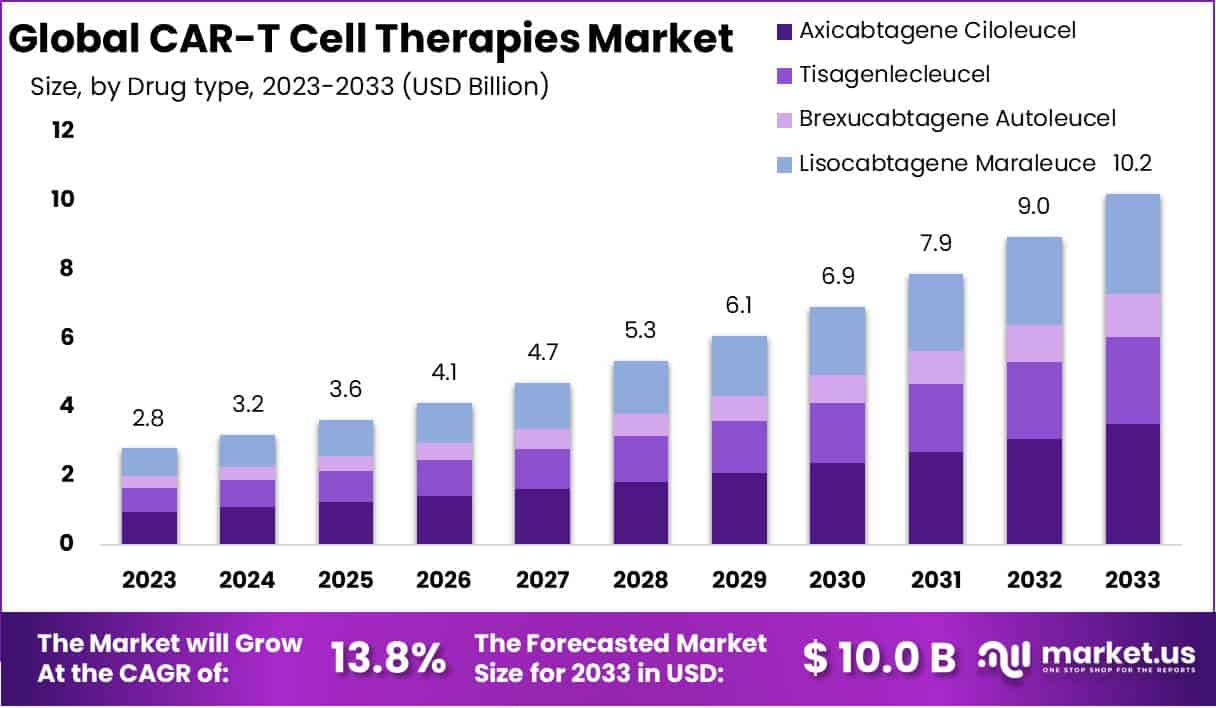

New York, NY – August 22, 2025: The global CAR-T cell therapies market is projected to reach USD 10.2 billion by 2033, growing from USD 2.8 billion in 2023 at a CAGR of 13.8%. CAR-T therapy is an advanced cancer immunotherapy where T cells are genetically engineered to identify and attack cancer cells. Approved by the U.S. FDA for certain leukemias, lymphomas, and multiple myeloma, this therapy offers new hope for patients with relapsed or refractory cancers. The treatment process includes collecting T cells, modifying them in a lab, and infusing them back into the patient. Its precision and high remission rates have positioned CAR-T as a transformative option in oncology.

A major driver of market growth is the rising global cancer burden, particularly hematologic malignancies. According to the World Health Organization (WHO), cancer accounted for nearly 20 million new cases in 2022 and remains the second-leading cause of death worldwide. Standard therapies often fail in advanced cases, creating demand for effective alternatives. CAR-T therapies demonstrate durable responses and higher remission rates, especially for patients with limited treatment options. This clinical advantage is accelerating adoption and creating strong opportunities for market expansion over the forecast period.

Regulatory advancements and clinical pipeline growth further boost the sector. Initially approved for B-cell acute lymphoblastic leukemia, CAR-T therapies are now expanding to indications like multiple myeloma and solid tumors. The FDA and EMA continue to accelerate approvals, while global clinical trials are exploring next-generation therapies such as dual-targeting constructs, allogeneic “off-the-shelf” CAR-T, and armored CAR-T cells. These innovations address challenges in safety, scalability, and manufacturing, while opening new therapeutic avenues. With hundreds of ongoing trials, the pipeline represents a key engine of market growth.

Strategic collaborations and supportive policies are also driving adoption. Leading companies, including Novartis, Gilead/Kite, and Bristol Myers Squibb, are investing heavily in research and commercialization. Partnerships with contract manufacturing organizations and technology providers are improving logistics, automation, and cryopreservation, reducing barriers to patient access. Government initiatives such as accelerated approvals, orphan drug designations, and reimbursement frameworks further strengthen the ecosystem. In the U.S., the Centers for Medicare & Medicaid Services (CMS) has introduced coverage models for CAR-T therapies, while similar efforts in Europe and Asia-Pacific are broadening patient access. Together, these factors highlight the sector’s strong growth trajectory and its potential to redefine cancer treatment worldwide.

Key Takeaways

- The CAR-T cell therapies market is projected to grow from USD 2.8 Billion in 2023 to USD 10.2 Billion by 2033, at 13.8% CAGR.

- Axicabtagene Ciloleucel leads with 34.4% share in 2023, boosted by FDA approval for large B-cell lymphoma treatment applications.

- The research segment dominates with 71.5% market share in 2023, reflecting strong research institution involvement and multiple therapies in clinical development.

- CD19/CD22 antigens represent 53.9% market share in 2023, proving highly effective for treating B-cell malignancies and advancing therapeutic success.

- Lymphoma holds the largest indication share of 57.1% in 2023, driven by FDA-approved CAR-T therapies targeting multiple lymphoma subtypes.

- Hospitals captured 62.8% market share in 2023, supported by advanced medical infrastructure, treatment capabilities, and rising patient admissions for specialized therapies.

- North America dominated with 61.49% share and USD 1.8 Billion in 2023, powered by chronic disease prevalence and strong R&D activities.

Regional Analysis

North America currently dominates the global CAR-T cell therapy market. The region accounted for 61.49% of the market revenue share and generated a market value of USD 1.8 billion in the year. The dominance is supported by a rising burden of chronic diseases, including autoimmune disorders and cancer. In addition, the growing investment in research and development is fueling market growth. A strong base of leading pharmaceutical companies and biotech players is also strengthening the regional market position.

The growing burden of cancer cases remains a key factor in the North American CAR-T market. According to the American Cancer Society, around 1,958,310 new cancer cases were reported, along with 609,820 cancer-related deaths in the region. These alarming figures are creating strong demand for innovative therapies such as CAR-T cell treatment. Moreover, the availability of approved therapeutic options and faster regulatory pathways is further boosting adoption across hospitals, clinics, and specialty care centers.

The presence of strong market players also enhances North America’s leadership in CAR-T therapies. Companies are investing in clinical trials, product innovations, and collaborations to expand therapeutic applications. Strategic initiatives, including partnerships and acquisitions, are helping accelerate commercialization. The favorable healthcare infrastructure and advanced reimbursement frameworks in the region are also contributing to higher acceptance. This supportive environment ensures that patients have better access to advanced cell therapies, strengthening North America’s market dominance during the forecast period.

The Asia-Pacific CAR-T cell therapy market is projected to grow rapidly in the coming years. Rising awareness about CAR-T therapy and its benefits is driving patient adoption across the region. Additionally, the increasing number of patients suffering from cancer and autoimmune disorders is expanding the target population base. Governments in several countries are also supporting advanced therapies through favorable policies and investments. This is expected to position Asia-Pacific as one of the fastest-growing markets, capturing a larger revenue share in the forecast period.

Key Players Analysis

Juno Therapeutics Inc.

Juno Therapeutics’ CAR-T asset, Breyanzi (lisocabtagene maraleucel), advanced strongly in 2024–2025. In 2024, U.S. approvals expanded to CLL/SLL (accelerated, March), follicular lymphoma (accelerated, May 15), and mantle cell lymphoma (May 30), broadening eligible patients across multiple B-cell malignancies. Commercial momentum followed: Q2-2024 Breyanzi sales reached $153 million, up 53% year over year, indicating rising adoption. In 2025, U.S. regulators streamlined cell-therapy labels by removing REMS and easing monitoring requirements, which is expected to reduce operational burden and support wider use.

Bristol-Myers Squibb Company

Bristol-Myers Squibb (BMS) remained a leading player in CAR-T cell therapies with two commercial assets: Breyanzi (CD19) and Abecma (BCMA). In 2024, the U.S. FDA broadened Breyanzi’s label to adults with relapsed/refractory chronic lymphocytic leukemia or small lymphocytic lymphoma after prior BTK and BCL-2 inhibitors, and approved it for relapsed/refractory follicular lymphoma; Abecma was expanded to triple-class–exposed multiple myeloma after two prior lines of therapy. Commercial performance strengthened: in full-year 2024, worldwide sales reached $747 million for Breyanzi (+105% year over year) and $406 million for Abecma (−14% year over year). Momentum continued into 2Q25, when Breyanzi delivered $344 million (+125% YoY) while Abecma recorded $87 million (−8% YoY). Risk management evolved: in April 2024 the FDA required a class boxed warning highlighting the rare risk of T-cell malignancies across CD19- and BCMA-directed CAR-Ts, while in June 2025 the FDA removed REMS requirements for approved CAR-Ts, which may ease treatment access. Overall, portfolio growth was supported by wider indications and rising adoption, while manufacturing capacity, safety monitoring, and real-world evidence generation remained core execution priorities in 2024–2025.

Gilead Sciences Inc.

Gilead Sciences operates CAR-T therapy through Kite Pharma, led by Yescarta (DLBCL and related LBCL) and Tecartus (MCL, adult B-ALL). In 2024, Kite’s cell-therapy franchise generated about $2.0 billion in sales and treated more than 7,000 patients globally, underscoring leadership in this category. Yescarta alone recorded approximately $1.6 billion in 2024 global sales. Manufacturing efficiency improved after FDA clearance of a process change that reduced U.S. median turnaround time for Yescarta from 16 to 14 days, supporting earlier treatment in aggressive disease. In 2025, performance has been mixed: Q1 2025 Yescarta sales were $386 million (+2% year over year) while Tecartus declined to $78 million (–22%); Q2 2025 Yescarta reached $393 million (–5% YoY) and Tecartus $92 million (–14% YoY), reflecting competitive and demand pressures despite price/mix support. Regulatory risk management also evolved; in June 2025 the FDA removed REMS requirements for Yescarta, easing program obligations at treatment centers. Overall, Gilead’s CAR-T position remains strong, supported by scale, real-world experience, and faster manufacturing, while near-term growth is expected to be shaped by market competition and the pace of adoption across eligible hematologic indications.

Merck & Co. Inc.

Merck & Co., Inc. did not disclose an in-house CAR-T program in 2024–2025; the firm’s published pipeline (updated Aug. 1, 2025) lists 50+ Phase 2 and 30+ Phase 3 programs, with no CAR-T modality shown. Instead, Merck positioned itself around the CAR-T ecosystem. In January 2024, Merck agreed to acquire Harpoon Therapeutics for ~$680 million to add HPN328, a DLL3-targeting T-cell engager, expanding immuno-oncology assets that can compete in settings overlapping with CAR-T use. In August 2024, Merck announced a $700 million upfront deal to acquire CN201 (later MK-1045), a CD3×CD19 bispecific with potential in B-cell diseases where CAR-T therapies are standard of care, signaling a strategy to address patients across and beyond CAR-T lines of therapy. In 2024, Artiva Biotherapeutics publicly noted that Merck had ended their earlier cell-therapy alliance, underscoring a shift away from direct cell-therapy development. Merck also supported combinations relevant to post-CAR-T care; for example, an NCI study launched in 2024 is evaluating pembrolizumab-based regimens in patients previously treated with CAR-T or autologous transplant. Overall, Merck’s 2024–2025 activity in the CAR-T sector was characterized by investment in T-cell engagers and supportive immunotherapies rather than proprietary CAR-T products.

Pfizer Inc.

During 2024–2025, Pfizer’s activity in CAR-T was advanced mainly through investments rather than in-house products. Pfizer Ventures supported Capstan Therapeutics, which raised $175 million in March 2024 to progress CPTX2309, an in-vivo CAR-T program toward first-in-human testing. A Pfizer Ventures overview in early 2025 indicated that a Phase 1 study for a CD19 in-vivo CAR-T was planned for 2025, reinforcing near-term clinical intent. Strategic value was further signaled when AbbVie agreed on June 30, 2025 to acquire Capstan for up to $2.1 billion; Capstan’s backers include Pfizer Ventures, underscoring Pfizer’s exposure to next-generation CAR-T approaches. Communications from Pfizer in November 2024 continued to frame CAR-T as a key element of modern cancer care, aligning corporate narratives with this modality’s clinical momentum. Taken together, Pfizer’s position in CAR-T during 2024–2025 can be characterized as capital-efficient participation in emerging in-vivo technologies with potential reach beyond oncology (e.g., autoimmune uses), while avoiding near-term commercial risk. Short-term watch items for 2025 include initiation and early readouts from Capstan’s Phase 1 program, which are expected to inform the feasibility and scalability of in-vivo CAR-T within Pfizer’s broader oncology strategy.

Conclusion

CAR-T cell therapies are moving from niche options to a core pillar in oncology care. Demand is being lifted by rising cancer prevalence, stronger clinical outcomes in hard-to-treat blood cancers, and quicker regulatory pathways across major regions. A broad pipeline, including dual-targeting, armored, and off-the-shelf approaches, is addressing safety, access, and manufacturing constraints. Strategic alliances among biopharma leaders, hospitals, and manufacturing partners are improving logistics, turnaround, and reimbursement readiness. Policy support, including accelerated approvals and coverage models, is further widening patient access. While safety monitoring and capacity remain watch points, the outlook is positive. Continued innovation and real-world evidence are expected to extend benefits into new indications and care settings.

View More:

Stem Cell Therapy Market || Autologous Cell Therapy Market || Cell Therapy Monitoring Kits Market || Allogeneic Cell Therapy Devices Market || Personalized Cell Therapy Market || Cell Therapy Market || Automated and Closed Cell Therapy Processing Systems Market || Cell Therapy Manufacturing Market || Cell Therapy Raw Materials Market

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)