Table of Contents

Overview

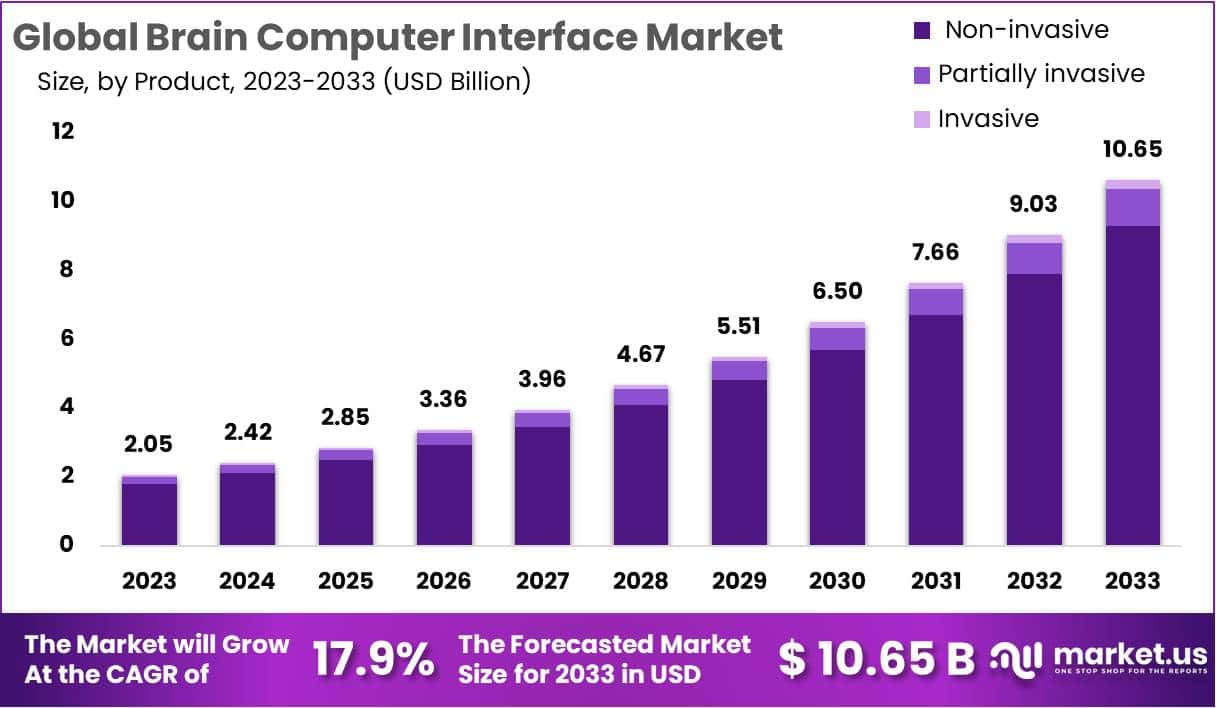

The Global Brain Computer Interface Market is projected to reach USD 10.65 billion by 2033 from USD 2.05 billion in 2023. Growth has been supported by steady advances in neuroscience, computing power, and sensor design. These improvements have strengthened the ability of systems to capture and interpret neural signals with higher precision. As a result, BCIs are being viewed as practical interface tools. The rising focus on human–machine interaction has reinforced the shift toward wider commercial readiness.

Demand in healthcare has increased as providers seek advanced assistive solutions. Adoption has been driven by the rising prevalence of neurological disorders, paralysis, and communication impairments. Noninvasive technologies have gained preference because they offer improved comfort, portability, and user-friendly operation. Better clinical outcomes and faster rehabilitation cycles have strengthened confidence in medical use cases. This trend is expected to support continued integration of BCIs into patient-care pathways worldwide.

Growth has also been influenced by rising interest in consumer technology. Companies are exploring BCI-enabled functions for wearables, immersive gaming, and interactive digital environments. Investment has focused on lightweight sensor systems, wireless designs, and software platforms that convert neural activity into digital responses. These developments have strengthened the commercial potential of BCIs. Broader uptake is expected as device accuracy increases and system costs decline over time.

Investment activity from technology firms and research institutions has further supported progress. Funding has accelerated work on advanced algorithms, machine-learning models, and neural-signal processors. These developments have improved system efficiency and lowered operational barriers. Collaboration among hardware manufacturers, software developers, and medical institutions has also contributed to faster innovation cycles. This integrated ecosystem has created favorable conditions for scalable product development.

Awareness of mental health and cognitive performance has opened additional opportunities. BCIs are being used to monitor attention, stress, and cognitive load in real time. These capabilities have expanded the market into workplace productivity, wellness, and training applications. Regulatory frameworks have also improved, offering clearer guidance on data protection and ethical use. Strengthened standards are expected to reduce entry barriers. Overall, sustained technological innovation and rising cross-industry demand continue to support a positive long-term market outlook.

Key Takeaways

- The global Brain Computer Interface market was described as reaching USD 2.05 billion and projected to surpass USD 10.65 billion, driven by a 17.9% CAGR.

- Non-invasive BCI technologies were reported as the dominant product category in 2023, accounting for 87.5% of total market revenue.

- Healthcare applications were identified as the primary contributors to market demand, representing a 63.3% share across all application segments.

- Medical end-use was highlighted as the largest segment, capturing 47.0% of the overall Brain Computer Interface market.

- North America was recognized as the leading regional market in 2023, supported by a 40.8% share of global revenue.

Regional Analysis

North America accounted for the largest share of revenue in the Brain Computer Interface Market in 2023. Its share reached 40.8 percent. This position was supported by strong investments in research and development. A high number of clinical trials on brain devices also strengthened the regional market. The presence of advanced healthcare systems created steady demand for BCI solutions. The widespread use of neurotechnology across research institutions further supported overall market expansion.

The growth of the North American market has been influenced by the increasing burden of neurodegenerative diseases. Conditions such as Parkinson’s, Alzheimer’s, and Huntington’s disease created higher demand for BCI-based interventions. Healthcare providers in the region continued to adopt advanced technologies. This adoption improved patient monitoring and rehabilitation. The rise of digital health strategies also contributed to stronger acceptance of brain interface systems. The environment encouraged continuous innovation in therapeutic and assistive applications.

Demand for immersive digital environments has also supported BCI adoption in North America. The trend toward advanced gaming experiences encouraged the development of augmented brain-computer interfaces. Developers in the region expanded their focus on interactive and intuitive systems. The availability of strong technological infrastructure accelerated these innovations. As a result, consumer interest in enhanced human–machine interaction increased. This shift created new opportunities for companies working on next-generation BCI technologies.

Asia Pacific is projected to record the highest CAGR during the forecast period. The region holds substantial untapped potential in healthcare and technology markets. Rising healthcare spending has encouraged the adoption of BCI solutions. Growing patient awareness has also supported early interest in these technologies. The availability of low-cost manufacturing sites strengthened regional competitiveness. Favorable taxation policies further attracted foreign investments. These conditions enabled companies to introduce innovative BCI products supported by continuous research and development efforts.

Segmentation Analysis

The Brain Computer Interface market has been segmented by product type into invasive, partially invasive, and non-invasive systems. In 2023, non-invasive BCI accounted for an 87.5 percent revenue share. Its dominance was supported by broad use in headsets, amplifiers, and gaming devices. Safety advantages were also noted, as these systems do not require surgical procedures. Active research programs continued to support adoption. The market outlook for non-invasive BCI remained positive, although invasive systems were projected to grow at a faster pace due to advanced clinical applications.

Invasive BCI solutions were expected to record the fastest CAGR during the forecast period. Their growth was attributed to support for critical functions such as brain-controlled robotic limbs and the restoration of vision through brain-camera integration. These devices interact with grey matter, which may cause scar tissue formation, yet clinical benefits continued to drive interest. Partially invasive systems were also projected to expand at a steady rate. Their adaptability and ongoing technological improvements were seen as key factors supporting market opportunities.

The market was also segmented by application into healthcare, smart home control, communication and control, and entertainment and gaming. Healthcare held a 63.3 percent share in 2023, driven by rising use in neurological care and patient assistance. Smart home control was expected to show strong growth due to demand for lifestyle enhancement and convenience. By end user, the medical segment held a 47.0 percent share. Military applications were projected to grow rapidly as BCI-enabled robots and communication tools gained adoption in defense operations.

Key Market Segments

By Product

- Invasive

- Partially invasive

- Non-invasive

By Application

- Healthcare

- Disabilities Restoration

- Brain Function Repair

- Smart Home Control

- Communication and Control

- Entertainment and Gaming

By End-use

- Medical

- Military

- Others

Key Players Analysis

The market share landscape of the Brain Computer Interface market is defined by strong competition among global and regional manufacturers. Growth in the market is driven by the rising adoption of advanced neurotechnology systems. Strategic initiatives are being prioritized to secure a larger customer base. The focus on mergers and acquisitions is increasing. These actions help companies combine strengths and extend technological capabilities. Broader portfolios are created through such actions. Market presence is also expanded. This approach supports stronger positioning in the evolving BCI ecosystem.

Product innovation continues to play a central role in strengthening competitiveness. Companies are launching new solutions to address changing customer demands. Advancements in sensors, software, and neural processing systems support this trend. New product introductions help manufacturers create differentiation. This approach also assists in targeting new application areas. The emphasis on technology upgrades improves performance and reliability. This strategy supports higher adoption across industries. Continuous innovation is expected to maintain steady growth.

Partnerships and collaborations remain important growth enablers for BCI manufacturers. Companies are partnering to enter new markets. Joint development projects support knowledge exchange and faster innovation cycles. Shared expertise improves the development of high precision systems. Resource sharing helps reduce operational pressure. This process supports better cost structures. Collaborative work also accelerates product testing and validation. These business strategies enhance competitiveness. Broader market coverage is achieved.

Key players shaping the Brain Computer Interface market include Natus Medical, Medtronic, Neuralink, Compumedics Neuroscan, and Brain Products GmbH. Other active participants include Advanced Brain Monitoring, NeuroSky, ANT Neuro, Ripple Neuro, and Neuroelectrics. Companies like OpenBCI and tec medical engineering also contribute to market development. Their efforts support innovation and wider adoption. Continuous investment in neuroscience solutions strengthens market activity. The presence of multiple players increases product diversity. This structure contributes to steady market expansion.

Top Key Players in Brain Computer Interface Market

- Natus Medical Incorporated

- tec medical engineering GmbH

- Medtronic

- Compumedics Neuroscan

- Neuralink

- Brain Products GmbH

- Advanced Brain Monitoring, Inc.

- NeuroSky

- ANT Neuro

- Neuroelectrics

- Ripple Neuro

- OpenBCI

- Other Key Players

Challenges

1) Signal quality and reliability

Non-invasive systems such as EEG often produce weak signals. Noise levels remain high, which reduces accuracy during real-time use. Stability over long periods is also limited. These issues lower user satisfaction and restrict broader adoption. Even with improved algorithms, consistent decoding across diverse users is difficult. The challenge continues to limit performance in daily environments. As a result, reliability remains a core barrier for commercial and clinical growth.

2) Surgical risk, durability, and long-term performance

Implantable BCIs must show strong safety and durability. Regulatory bodies expect detailed testing and long-term evidence. The devices must work for years without failure. Concerns include infection, hardware breakdown, and possible removal surgeries. These issues make approval processes slow and costly. Biocompatibility requirements are strict and complex. Companies must prove that benefits outweigh risks. Long-term performance remains a significant challenge for market expansion.

3) Clinical evidence and reimbursement readiness

Healthcare systems require solid proof of patient benefit. Trials must show gains in communication, independence, and quality of life. Many studies remain small or early-stage. As a result, evidence for reimbursement is still limited. Payers expect clear outcomes before supporting broader coverage. Regulatory pathways such as IDE exist, but pivotal data are still scarce. Stronger clinical validation is needed to improve adoption and support commercial growth.

4) Data governance and privacy

Neural data can reveal sensitive health and behavioral information. Current privacy laws do not fully address these signal types. This creates gaps for both consumer and medical neurotechnology. Cross-border data use adds further complexity. Policymakers and researchers have called for clearer rules. Stronger safeguards are required to protect neural information. Until these issues are addressed, privacy concerns will influence adoption and regulatory compliance across markets.

5) Cybersecurity and safety-by-design

BCI systems introduce new cybersecurity risks across hardware, firmware, and cloud platforms. Threats include data theft, model corruption, and unsafe stimulation. Security practices remain uneven and continue to evolve. Strong threat modeling and secure update processes are required. Continuous monitoring is also needed to prevent harmful breaches. The development of safety-by-design frameworks is still early. These gaps increase operational risk and limit user trust.

6) Ethics and global policy uncertainty

Countries are creating new rules for neurotechnology. These policies aim to support ethical use and improve public trust. However, they also increase compliance needs for companies. Regulations may shift quickly as the field evolves. Firms must track regional and global standards to avoid delays. The growing number of frameworks adds complexity for market entry. Uncertain policies continue to shape strategic planning in the BCI sector.

7) User experience and training burden

Many BCIs require long calibration sessions. Users face fatigue, drift, and setup challenges during daily use. These issues reduce convenience and limit long-term engagement. Achieving simple “plug-and-play” performance remains difficult across different settings. Homes, clinics, and workplaces create varying conditions that affect accuracy. Improving ease of use is essential for wider adoption. Better design and adaptive algorithms are needed to support consistent performance.

Opportunities

1) Restoring communication and control

Implantable BCIs are creating strong value for patients with severe paralysis, ALS, or brainstem stroke. These systems help users regain communication and basic control. Speech decoding and cursor or typing functions have advanced quickly. The clinical benefits support early use in hospitals. Payers are also showing interest because the impact on quality of life is clear. This combination strengthens early adoption and long-term market potential.

2) Less-invasive implantation routes

Endovascular BCIs reduce the need for open-brain surgery. These devices use blood vessels to place electrodes, which lowers medical risk. The method can expand patient eligibility and ease hospital concerns. U.S. feasibility studies show encouraging outcomes. Several devices have received breakthrough designations that indicate regulatory support. This progress suggests a faster path to adoption. It also positions less-invasive implants as a major growth area in the market.

3) AI-enhanced decoding and personalization

AI-driven models are improving decoding accuracy in both invasive and non-invasive BCIs. These tools can read fine motor intentions with higher precision. They also adapt to each user’s unique neural signals. This personalization increases ease of use and lowers training time. Better performance with simpler hardware creates new openings in rehabilitation and consumer-adjacent applications. As systems become more reliable, wider market appeal is expected.

4) Structured U.S. regulatory pathways

The U.S. FDA has created clearer guidelines for implanted BCIs. The Breakthrough Devices Program also offers support for technologies that meet unmet needs. These frameworks reduce development uncertainty for companies. They can also shorten review timelines. Clearer requirements make planning easier for clinical and commercial teams. As a result, firms can move more confidently through trials. This structure supports stronger investment and faster market entry.

5) Safety, fatigue, and risk management in workplaces

Non-invasive BCIs are being tested for monitoring fatigue and improving workplace safety. Neuroergonomics tools help track attention, stress, and performance. These systems can support training and reduce operational risks. Early enterprise pilots suggest growing interest outside healthcare. Adoption depends on strong privacy and consent protections. With clear safeguards, companies may use these tools to enhance workforce performance. This creates a new category of market demand.

6) Rising governance frameworks that build trust

New global guidelines are shaping responsible BCI development. Health and ethics groups are focusing on mental privacy and neural data protection. These rules create clearer expectations for companies and users. Strong governance reduces public concerns about misuse. It also lowers reputational risk for early adopters. As standards become more consistent, confidence in BCI technologies is expected to rise. This trust can support long-term market growth.

7) Expanding innovation pipeline

More companies are entering the BCI field with new electrodes, materials, and software. Early human tests show rapid progress in multiple areas. Advances in decoding, signal quality, and surgical tools are strengthening the supply chain. This broader base encourages partnerships and licensing opportunities. Component makers and research groups are also gaining traction. A larger innovation ecosystem supports market resilience and accelerates product development.

Conclusion

The global brain computer interface market is expected to grow at a steady pace as advancements in neuroscience, sensors, and software continue to strengthen system performance. Broader use in healthcare, consumer electronics, and workplace applications is being supported by higher accuracy and better user comfort. Progress in less-invasive implant options and clearer regulatory pathways is improving adoption prospects. Strong investment from technology firms and research institutions is helping accelerate innovation and expand commercial readiness. Although challenges remain in signal reliability, safety, and data governance, ongoing improvements suggest that brain interface technologies will gain wider acceptance across medical and non-medical sectors in the years ahead.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)