Table of Contents

Overview

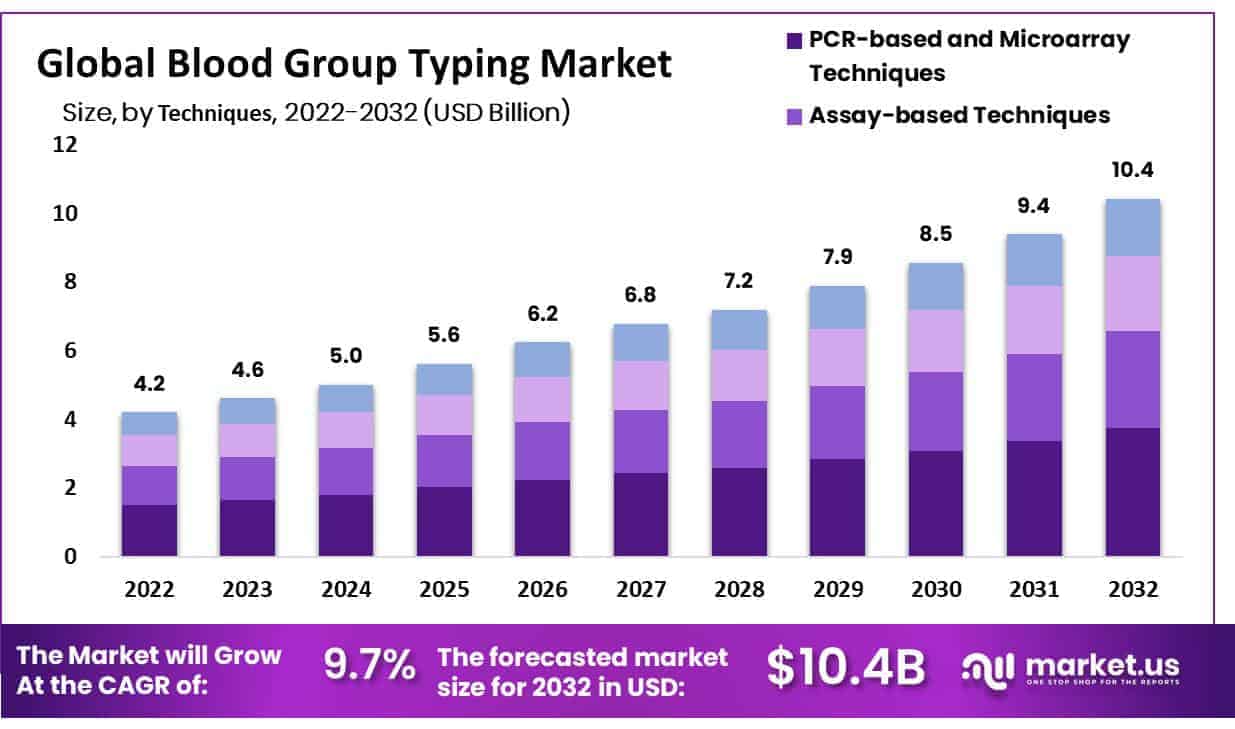

New York, NY – Sep 04, 2025 – Global Blood Group Typing Market accounted for USD 5.0 Billion in 2024 and is expected to reach around USD 10 Billion in 2032. Between 2025 and 2032, this market is estimated to register a CAGR of 9.76%.

Blood group typing has emerged as a vital component of modern healthcare, ensuring accuracy and safety in blood transfusions, organ transplantation, and maternal care. The classification of blood is primarily based on the ABO system and the Rh factor, which together determine compatibility between donors and recipients. Any mismatch can result in severe and life-threatening reactions, highlighting the importance of precise testing.

The growth in the use of advanced diagnostic technologies has significantly enhanced the speed and reliability of blood group typing. Automated analyzers, molecular typing techniques, and point-of-care testing are now increasingly utilized in hospitals and laboratories. These innovations minimize errors, improve efficiency, and contribute to timely medical interventions.

Blood group typing is also critical in prenatal care, as it helps detect Rh incompatibility between mother and fetus. Early identification allows for preventive treatments, reducing the risk of hemolytic disease of the newborn. Moreover, increasing awareness regarding blood donation drives has emphasized the importance of maintaining accurate donor records through proper blood typing.

Market trends indicate a rising demand for rapid, cost-effective, and portable blood typing solutions, particularly in developing regions where access to healthcare facilities is limited. This growth is further supported by government initiatives and investments in healthcare infrastructure. The role of blood group typing in ensuring patient safety and supporting medical advancements remains indispensable. Its continued evolution is expected to strengthen global healthcare systems in the years ahead.

Key Takeaways

- The global blood group typing market was valued at USD 5.0 billion in 2024 and is projected to reach USD 10 billion by 2032, expanding at a CAGR of 9.76% from 2025 to 2032.

- The consumables segment accounted for the largest share in 2022, representing 46% of the total market.

- PCR-based and microarray techniques collectively captured a 38% share in 2022, highlighting their growing adoption in diagnostic applications.

- The antibody screening segment generated the highest revenue in 2022 and is expected to record a profitable growth trajectory throughout the forecast period.

- Blood banks and hospitals remain the leading end-users of blood typing products and services, driving consistent demand.

- Geographically, North America dominated the market in 2022, holding a 42% share, attributed to advanced healthcare infrastructure and high diagnostic adoption rates.

- In Europe, major markets include the United Kingdom, Germany, and France, reflecting strong investments in healthcare and diagnostics.

- The Asia Pacific region, particularly China, India, and Japan, is witnessing rapid market expansion, driven by rising healthcare needs and improving diagnostic capabilities.

- In Latin America, Brazil and Mexico stand out as key markets, supported by growing awareness of blood safety and expanding healthcare services.

Regional Analysis

North America represents the largest market for blood typing, supported by the high prevalence of chronic diseases and the rising demand for blood transfusions and organ transplantations. The United States dominates the regional market due to its well-established healthcare infrastructure and the widespread adoption of advanced blood typing technologies.

Europe holds a significant share of the global market, driven by increasing awareness regarding the importance of blood typing and substantial investments in healthcare systems. Among European countries, the United Kingdom, Germany, and France are the leading contributors to market growth.

The Asia Pacific region is experiencing rapid expansion, propelled by the rising incidence of chronic diseases, growing demand for transfusions and organ transplantations, and increasing healthcare investments. China, India, and Japan are among the most prominent markets in this region.

Latin America also exhibits strong growth potential, supported by favorable government initiatives aimed at strengthening healthcare infrastructure and meeting the rising demand for blood transfusions. Brazil and Mexico remain the largest markets in this region.

The Middle East and Africa are emerging markets for blood typing, where demand is being fueled by growing transplantation and transfusion needs, alongside improvements in healthcare delivery systems. Saudi Arabia, South Africa, and the United Arab Emirates are leading countries in this region.

Overall, the global blood typing market is expected to register sustained growth across all regions, driven by the increasing need for transfusions and organ transplants, rising awareness of blood safety, and ongoing healthcare infrastructure development.

Frequently Asked Questions On Blood Group Typing

- What is blood group typing?

Blood group typing is a laboratory process used to determine an individual’s blood type based on the ABO system and Rh factor. It ensures compatibility for safe blood transfusions, organ transplantation, and maternal-fetal healthcare management. - Why is blood group typing important?

Blood group typing is vital to avoid adverse reactions during transfusions and transplants. Accurate typing prevents hemolytic reactions, supports prenatal care by identifying Rh incompatibility, and ensures patient safety in emergency and surgical medical procedures. - What are the main methods used in blood group typing?

Common methods include serological techniques, PCR-based testing, and microarray analysis. These approaches detect antigens and antibodies accurately, allowing laboratories and hospitals to minimize errors, accelerate diagnosis, and provide reliable compatibility results for critical healthcare interventions. - Who needs blood group typing?

Blood group typing is required for patients undergoing surgeries, emergency transfusions, or organ transplants. Pregnant women need testing to identify Rh incompatibility, while blood donors undergo typing to maintain reliable blood bank records for safe transfusion practices. - Which segment dominates the market?

The consumables segment accounted for the largest share in 2022 at 46%. Antibody screening generated the highest revenue, while PCR-based and microarray techniques collectively captured 38%, highlighting their strong adoption in modern diagnostic and laboratory practices. - Who are the major end-users of blood group typing?

Blood banks and hospitals represent the largest end-users of blood typing technologies. They rely heavily on accurate typing products and services to manage high volumes of transfusions, transplants, and donor screening for healthcare system efficiency. - Which regions lead the blood group typing market?

North America dominates the global market with a 42% share, led by the United States. Europe follows with major markets in Germany, the United Kingdom, and France. Asia Pacific, particularly China, India, and Japan, shows rapid expansion.

Conclusion

The global blood group typing market is positioned for strong growth, driven by increasing demand for transfusions, organ transplantations, and prenatal care. Advancements in molecular techniques, automated analyzers, and consumable-based solutions continue to enhance accuracy and efficiency in testing.

North America and Europe maintain market leadership, supported by advanced healthcare systems, while Asia Pacific is emerging as a high-growth region due to rising healthcare needs and investments. Latin America, the Middle East, and Africa also present expanding opportunities. Overall, blood group typing remains indispensable to modern healthcare, with its evolution set to strengthen global patient safety and healthcare outcomes.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)