Table of Contents

Overview

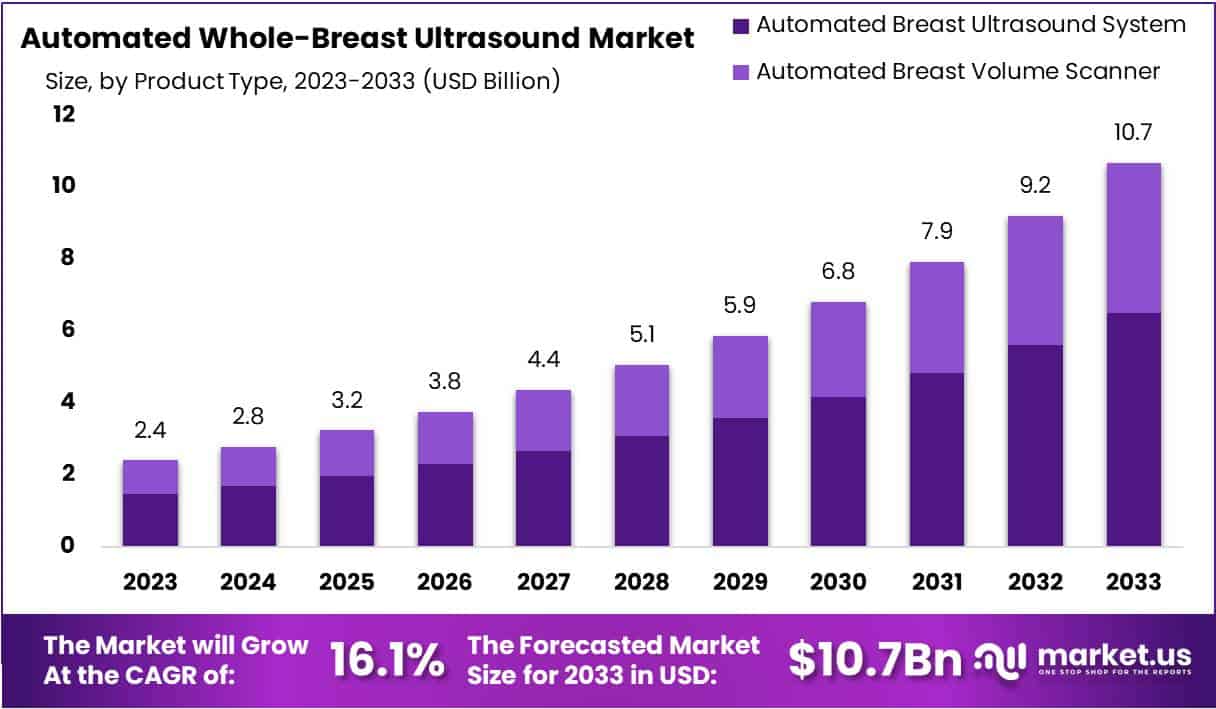

The Global Automated Whole-Breast Ultrasound (AWBUS) Market is projected to reach USD 10.7 billion by 2033, rising from USD 2.4 billion in 2023, at a CAGR of 16.1% from 2024 to 2033. Market expansion is driven by the increasing burden of breast cancer worldwide. Breast cancer remains the most diagnosed cancer among women. The growing screening population, along with unmet needs for accurate detection, continues to strengthen demand for automated ultrasound systems.

The limitation of conventional mammography in evaluating dense breast tissues is accelerating the use of AWBUS. Dense breast tissue reduces mammographic sensitivity and creates the risk of missed cancers. Automated systems improve visualization and support early detection of small lesions. As a result, the adoption of AWBUS as a supplemental tool in screening programs is rising in hospitals and diagnostic centers across key markets.

Technological advancements are contributing significantly to market growth. Automation ensures improved workflow efficiency and reduced operator dependency compared to handheld ultrasound. Advanced imaging features, including 3D scanning and artificial intelligence–based analysis, enhance diagnostic accuracy. These innovations are expected to improve screening outcomes, increase clinician confidence, and support higher utilization rates.

Government initiatives for early diagnosis and preventive healthcare also play a vital role. Awareness campaigns, reimbursement improvements, and cancer screening guidelines are promoting the integration of multimodal imaging solutions. Regulatory approvals for automated breast ultrasound in high-risk populations further support system procurement. Improved access to structured screening pathways is anticipated to maintain positive adoption trends.

Rising geriatric female populations and greater investments in healthcare infrastructure continue to expand market opportunities. The age-related risk of breast cancer increases the demand for dependable diagnostics. Developing regions are upgrading their imaging capabilities and establishing specialized breast cancer care facilities. These factors are expected to contribute to stable growth and extend the geographic reach of automated ultrasound technology throughout the forecast period.

Key Takeaways

- The global Automated Whole-Breast Ultrasound market is expected to reach USD 10.7 billion by 2033, supported by a strong 16.1% CAGR from 2024.

- Automated Breast Ultrasound Systems achieved dominant positioning in 2023, securing more than 61% of total market share across product categories.

- The evaluation application segment maintained leading status in 2023, holding over 49% market share in Automated Whole-Breast Ultrasound adoption worldwide.

- Hospitals remained the primary end-use setting in 2023, accounting for more than 52% of installations and usage within the Automated Whole-Breast Ultrasound sector.

- North America sustained leading market presence in 2023, representing over 45.8% share with approximately USD 1.1 billion valuation.

Regional Analysis

In 2023, North America secured a dominant share in the Automated Whole-Breast Ultrasound (AWBU) market. It captured more than 45.8% of the total revenue. The market value reached USD 1.1 Billion in the same year. This strong position can be attributed to advanced healthcare systems. High adoption of innovative screening technologies also supported growth. Rising awareness about breast cancer enhanced demand for automated screening tools. The region benefits from skilled medical professionals. These elements collectively strengthened the overall market presence. Growth remains supported by strong diagnostic capabilities.

The presence of major industry players has contributed to market expansion. Companies are investing in research and development activities. These efforts improve product performance and workflow efficiency. Supportive reimbursement structures enhance patient accessibility. Awareness campaigns promote early breast cancer detection. This increases utilization of AWBU systems. Strong collaborations between hospitals and technology providers drive innovation. Healthcare facilities focus on improved screening accuracy. These factors ensure the region continues to attract strategic investments. Market growth is stable and supported by positive industry initiatives.

A well-structured regulatory environment ensures product safety. Approval processes help build consumer trust. Standardized guidelines improve device quality. These systems boost purchasing confidence for hospitals and clinics. The region also benefits from continuous digital transformation. Healthcare providers adopt advanced imaging solutions. Market acceptance rises as product reliability strengthens. The regulatory support encourages new product launches. This results in more diagnostic options for patients. These conditions create a favorable business climate. It enhances opportunities for key market stakeholders.

North America is expected to maintain its leadership position. Growth will be driven by rapid technology improvements. Healthcare spending continues to increase every year. Preventive healthcare receives higher policy focus. This supports wider adoption of automated screening systems. However, cost containment remains a key challenge. Manufacturers must improve affordability and access. Evolving regulatory requirements demand careful compliance. Addressing these issues will sustain future growth. Market players must adopt competitive strategies. A strong outlook for the AWBU sector remains evident.

Segmentation Analysis

The Automated Breast Ultrasound System (ABUS) segment held the largest share of the Automated Whole-Breast Ultrasound Market in 2023. It accounted for more than 61% of total revenue. The growth of this segment is driven by the rising global burden of breast cancer. ABUS is effective for screening dense breast tissue where mammography has limitations. Continuous technological improvements have enhanced image quality. The system supports early detection and better clinical outcomes. Its reliability and precision have strengthened its preference in diagnostic workflows.

The Automated Breast Volume Scanner (ABVS) segment is experiencing steady growth. Its ability to generate detailed 3D volumetric images improves breast tissue assessment. The integration of advanced algorithms aims to increase detection accuracy and clinical decision-making. However, adoption is affected by high equipment costs and training requirements. Despite these barriers, ABVS is expected to expand as healthcare facilities prioritize advanced diagnostic capabilities. Continuous innovation is likely to reduce operational challenges and enhance diagnostic confidence for complex breast cases.

In 2023, the Evaluation segment led the market by application with more than 49% share. Automated systems support detailed assessments for early detection of abnormalities. Breast cancer screening applications also gained momentum. Growing awareness of screening benefits and the need to address dense breast tissue drive this rise. Other applications like lesion detection, monitoring, and follow-up play key roles in patient management. These systems are valued for high accuracy and their non-invasive approach. They help avoid radiation exposure while improving diagnostic effectiveness.

Hospitals dominated the end-use segment in 2023 with over 52% share. The adoption of automated ultrasound systems enhances early diagnosis and treatment planning in clinical environments. Diagnostic imaging centers contribute significantly by offering specialized services using advanced technologies. Breast health clinics are also expanding due to their focus on targeted breast care and improved detection precision. Other healthcare providers are increasingly integrating these systems. Advances in infrastructure and rising investments support wider usage. Personalized healthcare trends are expected to sustain market growth across all end-use categories.

Key Market Segments

Product Type

- Automated Breast Ultrasound System

- Automated Breast Volume Scanner

Application

- Evaluation

- Breast Cancer Screening

- Breast Lesion Detection

- Monitoring and Follow-up

- Others

End-Use

- Hospitals

- DIagnostic Imaging Centres

- Breast Health Clinics

- Others

Key Players Analysis

The automated whole-breast ultrasound market is driven by companies focused on advanced imaging technologies and better diagnostic accuracy. The growth of this market is supported by rising breast cancer cases and the need for early detection systems. Leading manufacturers invest in innovative approaches to improve workflow efficiency. Hitachi Ltd. demonstrates consistent progress in automated ultrasound technology. Its strong research and development activities support enhanced screening accuracy and patient convenience. The company’s wide product range strengthens its market presence and adoption in healthcare facilities focused on improving clinical outcomes.

Technological integration has become a key strategy among leading competitors. Siemens Healthcare GmbH focuses on artificial intelligence in ultrasound imaging. Its solutions aim to provide improved visualization and more accurate breast cancer detection. The company emphasizes automation to reduce operator dependency. This enhances consistency in screening results. Siemens continues to expand its presence across global markets. Its advanced product offerings support hospitals and diagnostic centers in delivering high-quality breast screening services while reducing examination time.

Reliability and strong brand recognition support further market penetration. Canon Medical Systems Corporation continues to refine its advanced imaging portfolio. Product development prioritizes image clarity and operational simplicity. This supports effective screening in diverse clinical settings. Canon’s automated systems are designed for efficient workflows and improved patient comfort. Ongoing innovation contributes to improved diagnostic performance. This positions the company as a key contributor to global adoption. Canon leverages long-term expertise in medical imaging to strengthen its competitive edge and market reach.

The market also benefits from contributions by major medical technology providers. General Electric Company offers advanced breast imaging equipment integrated with digital capabilities. Koninklijke Philips N.V. focuses on ergonomic design and improved clinical decision support. Hologic Inc. expands its automated ultrasound offerings through strategic initiatives. These companies support wider access to high-quality breast imaging devices. Their strong distribution networks and healthcare partnerships help expand market adoption. Together, they maintain a competitive landscape that encourages continuous innovation and improved patient outcomes.

Market Key Players

- Hitachi Ltd.

- Siemens Healthcare Gmbh

- Canon Medical Systems Corporation

- General Electric Company

- Koninklijke Philips N.V.

- Hologic Inc.

Conclusion

The Automated Whole-Breast Ultrasound market is expected to show strong and steady expansion. Growth is supported by rising breast cancer cases and the need for better detection in dense breast tissues. Automated systems are being chosen because they improve accuracy, reduce operator dependency, and support early diagnosis. Hospitals, diagnostic centers, and breast care facilities are increasing their use of this technology. Supportive government programs and continuous improvements in imaging further enhance adoption. Major companies are investing in innovation to deliver more reliable and efficient solutions. With better awareness and improved access to screening services, the market is positioned for long-term success and wider global availability.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)