Table of Contents

Overview

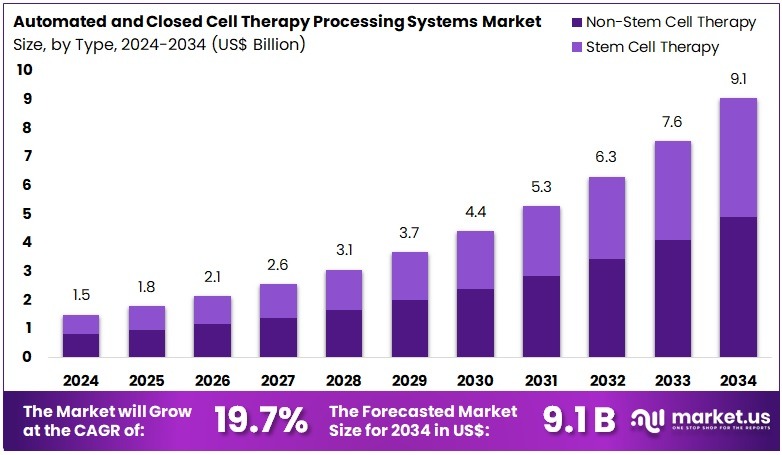

New York, NY – Aug 04, 2025: The Global Automated and Closed Cell Therapy Processing Systems Market is projected to reach US$ 9.1 Billion by 2034, up from US$ 1.5 Billion in 2024. This reflects a robust CAGR of 19.7% during the forecast period from 2025 to 2034. North America currently dominates the market with over 42.4% share, translating to a market value of US$ 0.6 billion. The region benefits from strong healthcare infrastructure, significant investments in biotechnology, and a favorable regulatory landscape that supports innovation in cell therapy manufacturing.

The market growth is driven by the rising demand for personalized medicine and advancements in cell and gene therapies. Automated and closed systems ensure accurate, sterile, and consistent production of complex cell-based treatments. These systems significantly reduce the risk of contamination and human error. With the increasing adoption of these technologies, manufacturers can meet stringent quality standards. The push for standardized and scalable solutions is leading to growing investments in automated bioprocessing tools worldwide, especially in clinical and commercial production environments.

In October 2024, Cellular Origins partnered with Fresenius Kabi to revolutionize cell therapy manufacturing. The partnership aims to merge innovative technologies with Cellular Origins’ advanced Constellation CGT robotic platform. This collaboration is expected to streamline production and enhance scalability. As demand rises, strategic alliances like this will play a pivotal role in boosting throughput while maintaining high safety and efficiency standards. These developments are helping shape the next phase of the cell and gene therapy (CGT) industry.

Regenerative medicine is gaining traction globally, creating vast opportunities for automated systems. These systems enable cost-effective, large-scale production of cell therapies. Closed systems are particularly important in reducing cross-contamination risks and maintaining product consistency. The market is witnessing increasing investment from pharmaceutical companies, startups, and academic institutions. Such interest is fueled by the potential of cell therapies to treat a range of conditions, including neurological disorders, cancer, and rare genetic diseases.

Government support and regulatory approvals are also playing a vital role in the market’s expansion. Agencies like the FDA and EMA are working to fast-track the approval process for cell-based treatments. This, in turn, is encouraging companies to develop efficient and safe processing platforms. As research progresses, automated and closed systems will remain essential in ensuring scalable, compliant, and high-quality manufacturing workflows. Their continued adoption is set to propel the cell therapy market to new heights by 2034.

Key Takeaways

- In 2023, the automated and closed cell therapy processing systems market earned US$ 1.5 billion, growing at a strong 19.7% CAGR.

- By 2033, the market is projected to hit US$ 9.1 billion, driven by increasing demand for advanced cell therapy manufacturing solutions.

- Non-stem cell therapy led the type segment in 2023, accounting for 54.3% of the total market share due to broader application areas.

- Within workflow categories, expansion processes dominated in 2023, contributing a notable 43.7% share to the overall market performance.

- On the basis of scale, the R&D scale segment captured the largest revenue share at 57.8%, indicating strong focus on early-stage development.

- North America was the leading regional market in 2023, securing a dominant 42.4% share thanks to strong biotech infrastructure and investment.

Regional Analysis

North America leads the automated and closed cell therapy processing systems market, holding a substantial 42.4% revenue share. This dominance is supported by a strong biopharmaceutical industry and a highly active cell therapy research ecosystem. The U.S. National Institutes of Health (NIH) allocated over US$ 6 billion to cell and gene therapy research in 2024, fueling innovation and new therapy development. Additionally, with the FDA approving more than 20 cell and gene therapies since 2017 many of them post-2021 the need for scalable, automated manufacturing systems has significantly increased. Venture capital investment of over US$ 10 billion in 2023 further boosted the adoption of advanced processing systems among biotech firms and academic institutions.

Asia Pacific is projected to witness the highest CAGR during the forecast period due to rising investments in biotechnology and focused efforts in cell therapy R&D. China alone has increased its biotech R&D spending by over 18% annually between 2021 and 2024. This surge is reflected in a 30% rise in cell therapy clinical trials across the region since 2021. Additionally, growing disease prevalence and strong government support for the biopharmaceutical sector are propelling the adoption of automated and closed systems to meet the anticipated demand for commercial-scale cell therapy production.

Segmentation Analysis

The non-stem cell therapy segment led the automated and closed cell therapy processing systems market with a 54.3% share. This dominance is largely attributed to the rapid progress and commercialization of non-stem cell therapies, especially CAR T-cell therapies used in cancer immunotherapy. These therapies have benefited from more established manufacturing protocols and a higher number of regulatory approvals compared to stem cell-based treatments. Their growing clinical success and expanding use in treating hematological malignancies and solid tumors have further fueled demand for advanced processing systems tailored to these cell types.

From a workflow perspective, the expansion segment held the largest share at 43.7%. Cell expansion is a vital step in most cell therapy production processes, involving the in vitro multiplication of therapeutic cells to meet dosage requirements. Automated and closed expansion systems are preferred over manual methods due to their scalability, process consistency, and minimized contamination risk. As clinical trials and commercial therapies require increasingly larger volumes of therapeutic cells, the demand for high-efficiency, automated expansion technologies continues to grow, solidifying this workflow’s dominance in the market.

Regarding scale, the R&D scale segment captured a leading 57.8% revenue share. This strong performance is driven by intensive research and development activities aimed at discovering and refining new cell therapy approaches. Closed and adaptable systems are essential for early-stage development, where small-batch production and flexible workflows are crucial. The increasing number of therapies in preclinical and early clinical phases underscores the need for robust R&D-scale platforms that support process optimization and smooth clinical translation, reinforcing the segment’s leadership position.

Key Players Analysis

Key players in the automated and closed cell therapy processing systems market are actively focused on delivering integrated, customizable solutions tailored to the evolving needs of cell therapy manufacturing. Their product offerings range from automated cell culture systems to closed-loop separation technologies and automated fill-finish platforms. To stay competitive, these companies frequently engage in strategic collaborations with cell therapy developers and contract manufacturing organizations (CMOs), allowing them to align their technologies with real-world production requirements and improve system adaptability.

Continuous innovation remains a core strategy, with a strong emphasis on enhancing scalability, process efficiency, and cost-effectiveness. One notable player is Lonza Group AG, based in Basel, Switzerland, a leading CDMO that also develops advanced cell therapy processing systems. With extensive experience in manufacturing cell therapies, Lonza is well-positioned to design solutions that address complex manufacturing challenges. Their integrated service model and technical expertise make them a significant contributor to the development and deployment of automated and closed systems in the market.

Emerging Trends

- Shift Toward End-to-End Automation: Companies are moving from partially automated tools to fully automated systems. This trend reduces the need for human handling and lowers the chances of contamination. End-to-end automation helps speed up production, making the process more efficient. It also ensures better consistency and reliability. These systems can run entire workflows, from cell collection to final formulation. As a result, manufacturers can improve turnaround times. This is especially helpful in commercial-scale production. It also supports clinical trial processes with tighter deadlines. The shift toward automation is now a key priority across the industry.

- Customization for Specific Cell Types: Modern systems are being designed to handle specific cell types like T-cells, NK cells, and dendritic cells. This customization improves the performance of therapies such as CAR-T, which are used to treat blood cancers. Tailored systems allow for better cell viability, growth, and recovery. They also help in maintaining the functionality of each unique cell type. Manufacturers now focus on flexible platforms that can adapt to different cell therapy protocols. This ensures higher success rates in both clinical trials and commercial batches. As a result, patient outcomes are also improving.

- Miniaturization and Portability: Smaller, modular systems are becoming more popular. These compact platforms are easy to use in small labs or hospital-based cleanrooms. They reduce the need for large infrastructure and allow localized production. This helps with on-site therapy preparation, especially in emergency or point-of-care settings. Portable systems also reduce transportation time and costs. They improve patient access in remote or underserved areas. This trend supports decentralized manufacturing. It makes it easier for hospitals and research centers to adopt cell therapies without major facility upgrades.

- AI-Driven Process Optimization: Artificial intelligence (AI) and machine learning are now being used in cell therapy systems. These tools help track data in real time. They also detect errors quickly and suggest solutions. AI can predict outcomes and improve overall process control. This leads to better quality and fewer failed batches. Automated alerts can reduce system downtime. AI integration supports better decision-making during production. It also makes the systems smarter with each batch processed. Over time, this results in higher efficiency and cost savings.

- Increased Focus on Regulatory Readiness: Companies are designing systems that meet strict global standards. These include GMP and other regulatory requirements. Having built-in compliance features helps reduce delays during approvals. It also builds trust with health authorities. Pre-validated systems speed up the path from clinical trials to commercial use. This trend ensures safety, consistency, and transparency in the manufacturing process. More companies are now prioritizing “compliance by design.” This makes it easier to scale up therapies while staying within legal frameworks. Regulatory readiness is now a critical part of system development.

Use Cases

- CAR-T Cell Therapy Manufacturing: Automated and closed systems are widely used in the production of CAR-T cell therapies. These systems can process over 10 patient samples in a single batch. They manage steps like cell expansion and gene transduction with precision. This reduces turnaround time from several weeks to just a few days. It also improves batch consistency and lowers contamination risks. Automation helps meet the urgent demand for cancer treatment. Many hospitals and biotech companies now rely on these systems to streamline CAR-T workflows. As the use of CAR-T expands, so does the need for efficient, closed manufacturing platforms.

- Allogeneic Cell Therapy Production: For donor-based therapies, also known as allogeneic therapies, these systems offer scalable production. One automated unit can expand donor cells into more than 1,000 doses. This allows for off-the-shelf treatments that are ready when needed. The closed nature of these systems reduces contamination risk and ensures product consistency. They also help lower costs and support large-scale clinical trials or commercial rollout. These platforms are essential for treating diseases like leukemia and autoimmune disorders. Their ability to maintain cell quality across high-volume production is a key advantage for therapy developers.

- Clinical Trial Sample Processing: In early-phase clinical trials, flexibility and safety are crucial. Automated and closed systems allow for small-batch production with minimal cross-contamination. One unit can manage up to 15 different trials at the same time using configurable settings. This allows researchers to test multiple cell therapy approaches under one platform. These systems also reduce manual steps, making the process more consistent. For studies in Phase I or II, this setup supports faster iteration and better results. It also saves time and reduces the risk of delays due to contamination or batch failure.

- Hospital-Based Point-of-Care Manufacturing: Hospitals are now using compact, closed systems directly in cleanroom facilities. These setups enable on-site preparation of therapies for patients. In many cases, treatment can happen on the same day. This is particularly helpful for urgent conditions like graft-versus-host disease. It eliminates the need for transportation and external manufacturing. The systems are small, easy to install, and designed for fast processing. By reducing logistics and waiting times, hospitals can treat patients faster and more effectively. This use case supports personalized medicine right at the point of care.

- Gene Editing Workflow Integration: Automated systems are also used in gene-edited cell therapy production. They can integrate CRISPR and other editing tools into the workflow. These platforms handle critical steps like washing, cell concentration, and formulation automatically. This reduces human error by over 80% and improves process consistency. These systems also track and document each step, which is vital for regulatory approval. Developers use them to produce gene-edited cells for both rare diseases and cancer. Their efficiency and precision make them ideal for next-generation therapies that require genetic modifications.

FAQs Automated and Closed Cell Therapy Processing Systems

1. What are automated and closed cell therapy processing systems?

Ans:- These are advanced manufacturing platforms used to produce cell therapies. They automate steps like cell separation, expansion, gene modification, and fill-finish. Being closed systems, they minimize contamination risk and reduce the need for manual handling.

2. Why are these systems important in cell therapy production?

Ans:- They ensure consistent product quality, reduce human error, and improve process efficiency. This is especially important in personalized or high-volume cell therapy manufacturing where sterility and accuracy are critical.

3. What types of cell therapies use these systems?

Ans:- They are commonly used for CAR-T therapies, stem cell therapies, dendritic cell therapies, NK cell-based treatments, and other immune cell therapies.

4. How do these systems help reduce manufacturing time?

Ans:- Automation speeds up processes like cell expansion and gene modification. What once took weeks can now be completed in days, allowing faster delivery of therapies to patients.

5. Are these systems suitable for hospitals or just industrial labs?

Ans:- Yes, compact versions are now available for hospital cleanrooms. They allow point-of-care manufacturing, enabling same-day treatment in some clinical scenarios.

6. Do these systems support gene editing workflows like CRISPR?

Ans:- Yes, many platforms integrate CRISPR and other gene-editing tools into their workflows. They offer automated washing, concentration, and formulation steps post-editing.

7. Are they compliant with regulatory requirements?

Ans:- Most modern systems are designed to meet GMP and other regulatory standards. They often include data tracking, validation support, and quality control features.

6. What is the current size of the automated and closed cell therapy processing systems market?

Ans:- As of 2024, the market is valued at approximately US$ 1.5 billion. It is expected to grow rapidly due to increased demand for personalized medicine and cell-based treatments.

7. What is the expected growth rate of this market?

Ans:- The market is projected to grow at a CAGR of 19.7% from 2025 to 2034, reaching around US$ 9.1 billion by 2034.

8. Which region holds the largest market share?

Ans:- North America currently leads with over 42% market share. This is due to strong biotech infrastructure, funding, and regulatory support.

9. Which segment dominates the market by therapy type?

Ans:- Non-stem cell therapy dominates, accounting for over 54% share. These include CAR-T and other immune cell therapies with established protocols.

10. What workflow segment holds the highest share?

Ans:- The expansion segment leads with over 43% share. This step is essential for producing enough therapeutic cells for treatment.

Conclusion

The automated and closed cell therapy processing systems market is poised for remarkable growth, projected to reach US$ 9.1 billion by 2034, driven by the rising demand for personalized and scalable cell-based treatments. With a strong CAGR of 19.7%, the market is fueled by advancements in automation, increasing clinical success of therapies like CAR-T, and growing regulatory support worldwide.

North America currently leads the market, but Asia Pacific is emerging rapidly due to significant R&D investments. As the need for precision, consistency, and contamination-free manufacturing rises, automated and closed systems are becoming essential in both clinical and commercial cell therapy production, reshaping the future of regenerative medicine.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)