Table of Contents

Overview

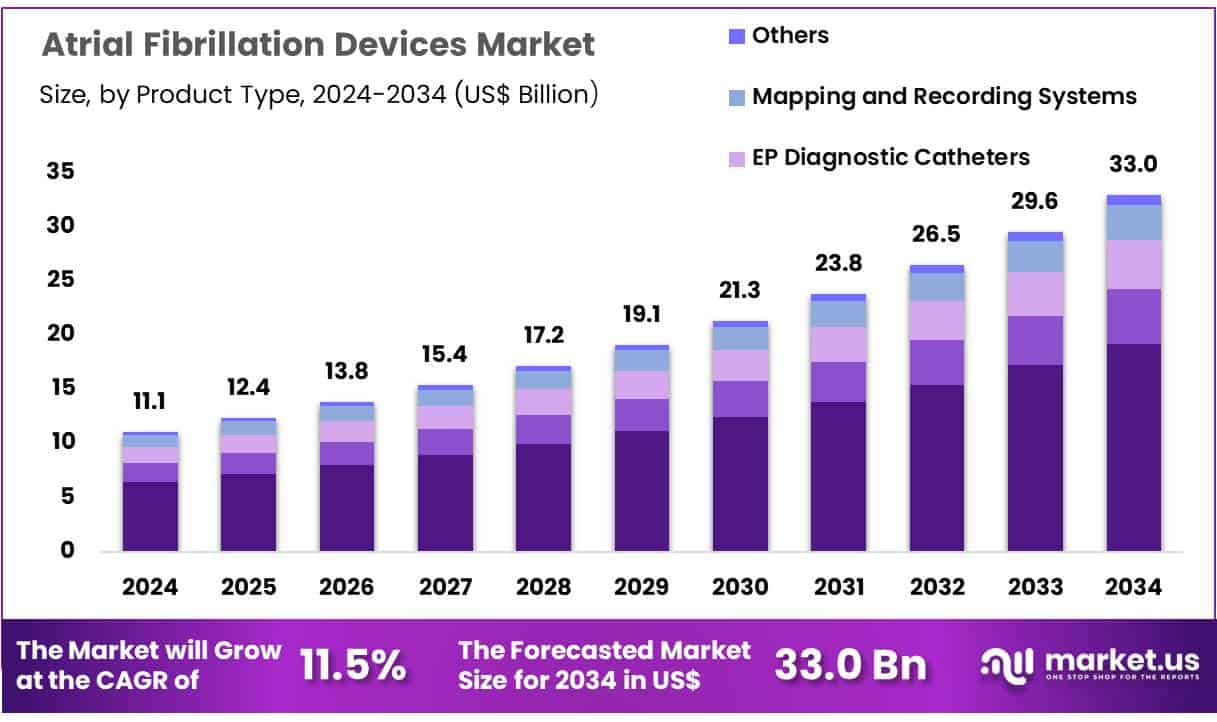

New York, NY – June 25, 2025 – Global Atrial Fibrillation Devices Market size is expected to be worth around US$ 33.0 Billion by 2034 from US$ 11.1 Billion in 2024, growing at a CAGR of 11.5% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 42.2% share with a revenue of US$ 4.7 Billion.

The atrial fibrillation (AF) devices market is experiencing steady growth, driven by the rising global incidence of atrial fibrillation and increasing adoption of advanced cardiac rhythm management technologies. Atrial fibrillation, the most common sustained cardiac arrhythmia, affects millions of people worldwide and is associated with a significantly elevated risk of stroke and heart failure. This has led to heightened demand for effective intervention and monitoring solutions.

The market is segmented by product into ablation devices, pacemakers, implantable cardiac monitors, and diagnostic devices. Ablation devices dominate the segment due to their effectiveness in correcting abnormal electrical pathways in the heart. Cryoablation and radiofrequency ablation technologies are increasingly used in minimally invasive procedures. Diagnostic devices, such as electrocardiographs and wearable ECG monitors, are also gaining traction with the rise in outpatient monitoring.

Geographically, North America holds the largest share, supported by a high prevalence of cardiovascular diseases and access to advanced healthcare infrastructure. Meanwhile, Asia-Pacific is expected to witness rapid growth due to rising awareness, expanding healthcare systems, and aging populations.

Furthermore, advancements in AI-powered arrhythmia detection and catheter-based therapies are reshaping treatment strategies. Increasing investments in cardiac care, along with favorable reimbursement policies in developed regions, are also contributing to market expansion. As healthcare systems focus on early detection and personalized treatment, the AF devices market is expected to see sustained demand globally.

Key Takeaways

- In 2024, the global atrial fibrillation devices market was valued at US$ 11.1 billion and is projected to reach US$ 33.0 billion by 2033, expanding at a compound annual growth rate (CAGR) of 11.5% over the forecast period.

- By product type, the market is segmented into EP ablation catheters, cardiac monitors or implantable loop recorders, EP diagnostic catheters, mapping and recording systems, and others. Among these, EP ablation catheters emerged as the dominant category in 2023, accounting for a 58.2% share of the total market.

- In terms of end-users, the market is categorized into hospitals & cardiac centers, ambulatory surgical centers, and others. Hospitals & cardiac centers led this segment, contributing 62.3% of the global revenue in 2023, owing to their advanced infrastructure and higher patient volume.

- Regionally, North America held the leading position in the atrial fibrillation devices market, securing a 42.2% share in 2023. The dominance of the region is attributed to the high prevalence of atrial fibrillation, well-established healthcare facilities, and favorable reimbursement frameworks.

Segmentation Analysis

- Product Type Analysis: In 2023, the EP ablation catheters segment dominated the atrial fibrillation devices market with a 58.2% share. This growth is attributed to the rising adoption of catheter ablation as a first-line or second-line treatment for symptomatic atrial fibrillation. Advancements in radiofrequency and cryoablation technologies have improved procedural outcomes. The growing preference for minimally invasive interventions and the proven long-term benefits of ablation are further supporting the segment’s continued market leadership.

- End-User Analysis: Hospitals and cardiac centers accounted for 62.3% of the market in 2023, maintaining the largest share among end-users. These institutions are equipped with specialized electrophysiology labs and skilled personnel necessary for conducting complex AFib diagnostics and interventions. The high patient volume, combined with the availability of advanced technologies and infrastructure, supports the segment’s dominance. Moreover, their role in clinical research and early adoption of innovative AFib therapies reinforces their importance in the global market landscape.

Market Segments

Product Type

- EP Ablation Catheters

- Radiofrequency (RF)

- Ultrasound

- Microwave

- Laser

- Cryoablation

- Others

- Cardiac Monitors or Implantable Loop Recorder

- EP Diagnostic Catheters

- Steerable Catheters

- Fixed Curve Catheters

- Advanced Mapping Catheters

- Mapping and Recording Systems

- Others

End-user

- Hospitals & Cardiac Centers

- Ambulatory Surgical Centers

- Others

Regional Analysis

North America led the global atrial fibrillation devices market in 2023, capturing a revenue share of 42.2%. This dominance is primarily attributed to the high prevalence of atrial fibrillation (AFib) and the region’s advanced healthcare infrastructure. According to the CDC, approximately 12.1 million U.S. adults are projected to have AFib by 2030.

Well-established electrophysiology (EP) labs, performing over 200,000 catheter ablation procedures annually (American College of Cardiology, 2022), along with favorable reimbursement policies, contribute to the region’s leading position. Furthermore, the presence of major device manufacturers, strong R&D initiatives, and the FDA’s approval of innovative ablation technologies since 2021 are accelerating market expansion. The rising use of implantable loop recorders for early arrhythmia detection further supports growth.

Meanwhile, Asia Pacific is projected to exhibit the highest compound annual growth rate (CAGR) during the forecast period. Factors such as a growing elderly population, increased awareness of cardiovascular conditions, and expanding healthcare investments are driving the market. In China alone, over 10 million AFib cases were reported in 2021, and more than 50 EP labs were established between 2021 and 2023. Government initiatives in countries like India and the rising adoption of remote cardiac monitoring solutions in Australia are also contributing to the region’s rapid market development.

Emerging Trends

- Widespread Adoption of Wearable ECG Monitors: Ambulatory ECG patches and wearable devices have been increasingly adopted as a standard of care for AFib diagnosis. In recent years, 14-day adhesive ECG patches have demonstrated significantly higher arrhythmia detection rates compared to traditional 24-hour Holter monitors, improving early identification of AF episodes in outpatients.

- Integration of Artificial Intelligence and Machine Learning: Advanced algorithms are now routinely applied to large volumes of wearable sensor data to enhance AF detection. AI-driven models can identify subtle rhythm irregularities and predict patient subgroups missed by conventional tools, thereby increasing diagnostic yield through automated analysis of photoplethysmography and ECG signals.

- Proliferation of Software-Only Medical Applications: Over-the-counter mobile applications, such as the FDA-cleared AFib History Feature for Apple Watch (K213971) and similar Samsung smartphone-linked SaMDs, have been introduced. These software tools analyze pulse-rate data to notify users of irregular rhythms suggestive of AF, expanding access without additional hardware.

- Telemedicine and Remote Monitoring Integration: AF devices are increasingly connected to cloud platforms and smartphone applications, enabling real-time data sharing with clinicians. This integration supports continuous surveillance, timely interventions, and enhanced patient engagement through remote follow-up workflows, which have been evaluated in recent FDA post-market studies.

Use Cases

- At-Home Population Screening: Wearable smartwatches equipped with AF detection software have been employed for broad population screening. In the Fitbit Heart Study involving over 450,000 participants, the Irregular Rhythm Notifications feature achieved 98% accuracy in identifying irregular heart rhythms, prompting medical follow-up in asymptomatic individuals.

- Post-Stroke Arrhythmia Surveillance: Extended external loop recorders have been used to detect AF in patients with cryptogenic stroke. In a landmark trial, 30-day monitoring identified AF in 16.1% of patients versus only 3.3% with repeat 24-hour Holter monitoring, enabling earlier initiation of anticoagulant therapy to reduce recurrent stroke risk.

- Extended Holter Monitoring in Cryptogenic Stroke Survivors: Seven-day Holter recordings after cryptogenic stroke revealed AF in 9% of patients at baseline. Continued monitoring over 36 months increased cumulative detection to 36%, guiding long-term management and anticoagulation decisions in high-risk cohorts.

- Prescription-Based Remote ECG Monitoring: Prescription wearable systems, such as the Verily Study Watch with Irregular Pulse Monitor, are utilized by adult patients diagnosed with or at risk for AF. Daily single-channel ECG recordings are transmitted to healthcare providers, facilitating timely clinical decision-making and personalized care plans.

Conclusion

The global atrial fibrillation devices market is poised for significant growth, driven by rising AFib prevalence, technological advancements, and increasing demand for early diagnosis and personalized care. With a projected CAGR of 11.5% from 2025 to 2034, the market is expected to reach US$ 33.0 billion by 2034.

North America remains the leading region, while Asia Pacific shows the fastest growth potential. Innovations in AI-powered detection, wearable monitors, and remote care platforms are reshaping patient management. Expanding access to advanced treatment and monitoring solutions will continue to drive adoption and enhance outcomes across global healthcare systems.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)