Table of Contents

Introduction

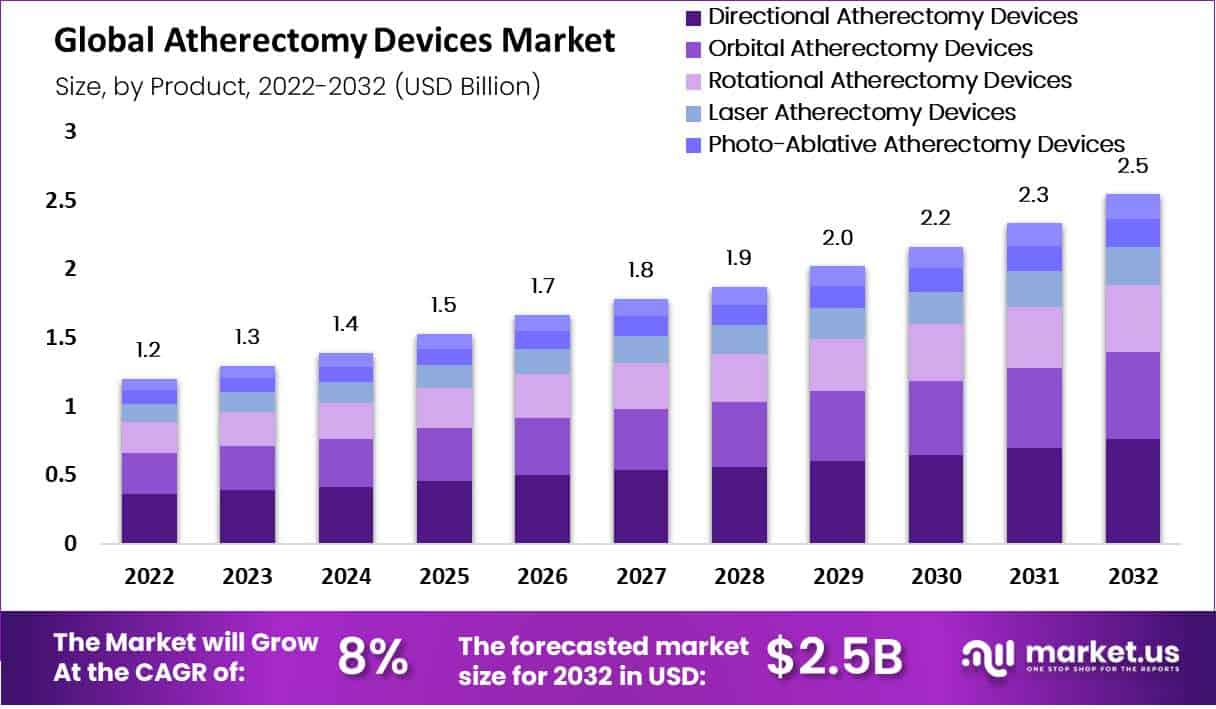

The Atherectomy Devices Market experienced notable growth, valued at USD 1.2 billion in 2022, with projections to reach USD 2.5 billion by 2032. This market is anticipated to expand at a compound annual growth rate (CAGR) of 8% from 2023 to 2032. This growth trajectory is primarily driven by continual advancements in medical technology and significant changes in healthcare policies.

One of the pivotal drivers of this market is the increased adoption of atherectomy devices in office-based labs (OBLs), fueled by policy reforms that facilitate outpatient procedures to curtail healthcare expenses. Despite the benefits, this transition has sparked concerns regarding the adequacy of clinical oversight and the risk of procedure overutilization in these less regulated settings.

Reimbursement strategies also play a critical role in the market dynamics. Since the revision of reimbursement rates by the Centers for Medicare and Medicaid Services (CMS) in 2011, there has been a surge in the number of atherectomy procedures. These procedures now fetch higher reimbursement rates compared to traditional methods such as balloon angioplasty, thus promoting the broader utilization of atherectomy devices.

Technological advancements have significantly contributed to the sector’s expansion. The market has seen the development and approval of diverse atherectomy devices, including directional, rotational, and orbital types, each designed to address specific lesion characteristics. This variety enables personalized treatment plans that can potentially reduce complications such as vessel trauma and the need for further interventions.

However, the sector faces challenges concerning clinical outcomes and safety. The absence of comprehensive comparative studies among the various FDA-approved atherectomy devices often leaves medical professionals reliant on clinical judgment rather than empirical evidence. This highlights the urgent need for rigorous clinical trials to establish effective and cost-efficient treatment protocols that integrate atherectomy with other innovative technologies like drug-coated balloons and bioabsorbable stents. Such studies are crucial for ensuring that the procedures are applied effectively and judiciously.

Key Takeaways

- Atherectomy Devices Market is projected to reach USD 2.5 billion by 2032, from a valuation of USD 1.2 billion in 2022.

- This market is expected to grow at a compound annual growth rate (CAGR) of 8% from 2023 to 2032.

- In 2022, directional atherectomy was the leading segment by product, generating the most revenue.

- Peripheral vascular applications held a 45% market share in the atherectomy devices market.

- North America led the market with a 36% revenue share in 2022.

- The Asia-Pacific region is anticipated to experience the fastest growth in this market.

- The American Heart Association reported that cardiovascular diseases caused 18.6 million deaths worldwide in 2019.

- It is estimated that over 200 million people worldwide suffer from peripheral artery disease (PAD).

- A study by the American Heart Association found a 94.7% success rate for atherectomy devices.

- The restenosis rate following atherectomy procedures stands at 37.7%.

- Atherectomy Devices Market Key Players: Abbott Laboratories, Boston Scientific Corporation, Medtronic, Becton Dickinson and Company (BD Interventional), Koninklijke Philips N.V., Avinger Inc., Rex Medical, AngioDynamics, Cardiovascular Systems Inc., Bard Peripheral Vascular Inc., Spectranetics St., Jude Medical Inc., Straub Medical AG, Terumo IS, Volcano Corporation, and Others Key Players

Emerging Trends

- Technological Advancements: Atherectomy devices have undergone significant innovations, introducing mechanisms that can cut, shave, sand, or vaporize arterial plaque. This technological progression allows for personalized treatment plans tailored to the specific needs of each patient. These advancements not only improve the effectiveness of procedures but also enhance the scope of atherectomy in treating arterial diseases.

- Minimally Invasive Procedures: Atherectomy provides a minimally invasive alternative to traditional surgical approaches. This method significantly reduces recovery time and lowers the risk of complications. It is particularly advantageous for patients who are not suitable candidates for open surgery, offering a safer and more efficient treatment option.

- Expanded Applications: Initially developed for peripheral artery disease, the use of atherectomy has now expanded to include the treatment of coronary artery disease. This broadening of applications extends the clinical utility of atherectomy devices, making them a versatile tool in the management of various arterial conditions.

- Integration with Imaging Technologies: The integration of atherectomy devices with advanced imaging technologies, like optical coherence tomography, has revolutionized procedural accuracy. This synergy enhances the precision of atherectomy procedures, significantly improving outcomes for patients by providing real-time visual guidance during the treatment.

Use Cases

- Peripheral Artery Disease (PAD) Use in the U.S.: In the United States, an estimated 6.5 million individuals aged 40 and above suffer from Peripheral Artery Disease (PAD). Atherectomy devices play a crucial role in this context by removing plaque from leg arteries. This treatment helps alleviate symptoms such as pain and difficulties with mobility. It provides a significant relief for patients, improving their quality of life and daily functioning.

- Coronary Artery Disease (CAD) Treatment: Atherectomy devices are particularly valuable for patients with severely calcified coronary arteries. These devices assist in modifying or eliminating hardened plaque. This process is critical as it facilitates the successful placement of stents, which are essential for maintaining open, functional arteries and ensuring effective blood flow to the heart.

- Addressing In-Stent Restenosis: Atherectomy is also effective in cases of in-stent restenosis, where arteries with previously placed stents become narrowed again due to new tissue growth. By using atherectomy devices, physicians can remove this blockage and restore the artery’s openness, ensuring the stent continues to function as intended.

- Management of Complex Lesions: For complex arterial lesions that involve significant calcification or complete blockages, atherectomy offers a beneficial treatment option. Traditional angioplasty might not always be effective in these cases. Atherectomy devices provide an alternative method by directly removing the blockages, which helps in managing these challenging medical scenarios effectively.

Regional Analysis

The Atherectomy Devices Market is experiencing robust growth, driven largely by the increasing acceptance of atherectomy systems among healthcare professionals. North America, particularly the United States, holds the dominant market share of 36%. This region benefits from a large patient base suffering from peripheral and coronary artery diseases and the presence of numerous FDA-approved devices. The extensive clinical trials being conducted further strengthen market prospects.

Cardiovascular diseases (CVD) remain a critical concern globally, with the American Heart Association reporting 18.6 million deaths in 2019. This has spurred the demand for atherectomy devices, which are essential in managing CVD. The stress on healthcare systems worldwide is expected to boost the demand for these devices during the forecast period.

In terms of support factors, the market benefits significantly from favorable reimbursement policies in North America. These policies enhance patient access to necessary surgical interventions, making advanced treatments like atherectomy more available. The variety of devices that have received FDA approval also contributes to the growth and trust in these medical solutions across the region.

Geographically, the market extends beyond North America to include Western Europe, Eastern Europe, Asia-Pacific (APAC), Latin America, and the Middle East and Africa (MEA). Each region presents unique growth opportunities and challenges, influenced by local healthcare infrastructures, regulatory environments, and economic conditions. Countries such as Germany, France, China, and Brazil are pivotal in driving regional market dynamics.

Key Players Analysis

Abbott Laboratories

Abbott Laboratories is a key player in the atherectomy devices market, which is expected to grow significantly. Their involvement includes offering various types of atherectomy systems such as directional, orbital, and laser atherectomy devices, catering to a range of applications from peripheral to cardiovascular treatments. The market is driven by the growing demand for minimally invasive surgeries and a favorable reimbursement scenario in developed markets. Despite facing challenges like stringent regulations and the need for highly trained surgeons, Abbott continues to innovate in this sector, contributing to its expansion. North America remains a dominant region for this market due to substantial investments in healthcare research and development.

Boston Scientific Corporation

Boston Scientific Corporation is a leading provider in the atherectomy devices sector, offering advanced solutions for the treatment of arterial blockages. Their Jetstream™ Atherectomy System is engineered to treat various lesion types, including calcium, plaque, and thrombus, commonly found in total occlusions. This system features active aspiration to minimize the risk of distal embolization. Additionally, the ROTAPRO™ Rotational Atherectomy System utilizes a diamond-tipped burr rotating at high speeds to effectively modify vessel compliance in calcified lesions. These devices are designed to enhance procedural efficiency and improve patient outcomes in the management of peripheral artery disease.

Medtronic

Medtronic is a leading company in the atherectomy devices sector, focusing on treating peripheral arterial disease (PAD). Their HawkOne™ Directional Atherectomy System is designed to remove plaque from arteries both above and below the knee, effectively restoring blood flow. This device is capable of treating various types of plaque, including severe calcium deposits, and features quick and easy cleaning to enhance procedural efficiency. Additionally, Medtronic’s SilverHawk™ Peripheral Plaque Excision System offers a method to remove plaque without leaving any implants behind, preserving the native vessel and maintaining future treatment options.

Becton, Dickinson, and Company (BD Interventional)

Becton, Dickinson, and Company’s (BD) Interventional segment offers the Rotarex™ Rotational Excisional Atherectomy System, designed to efficiently remove both plaque and thrombus from peripheral arteries. This device employs three distinct mechanisms to modify, excise, and aspirate complex lesions, including in-stent restenosis. The system is user-friendly, featuring a simple setup with a small plug-and-play component and a reusable handle. However, recent reports have highlighted safety concerns, with 30 serious injuries and 4 deaths associated with device breakage during use. In response, BD has updated the device’s instructions to enhance safety protocols.

Koninklijke Philips N.V.

Koninklijke Philips N.V. is a key player in the atherectomy devices market, offering innovative solutions for treating peripheral artery disease (PAD). Their Phoenix atherectomy system is designed to cut, capture, and clear diseased tissue in a single insertion, effectively addressing various plaque types in arteries. Additionally, Philips’ Turbo-Elite laser atherectomy catheter utilizes ultraviolet light to treat complex lesions, providing a versatile tool for healthcare professionals. Notably, Philips laser systems have been used in over one million procedures, underscoring their significant impact in this sector.

Conclusion

The Atherectomy Devices Market is experiencing steady growth due to advancements in medical technology, increased demand for minimally invasive procedures, and supportive healthcare policies. The rising prevalence of peripheral and coronary artery diseases is driving the need for effective treatment options, with atherectomy offering a precise method to remove arterial plaque. The integration of advanced imaging technologies has further enhanced procedural accuracy and patient outcomes. North America remains a key region due to its well-established healthcare infrastructure, while the Asia-Pacific region is witnessing rapid adoption. Despite challenges such as procedural risks and regulatory concerns, continuous innovation and clinical research will strengthen the market, making atherectomy devices a crucial solution for arterial disease management.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)