Table of Contents

Overview

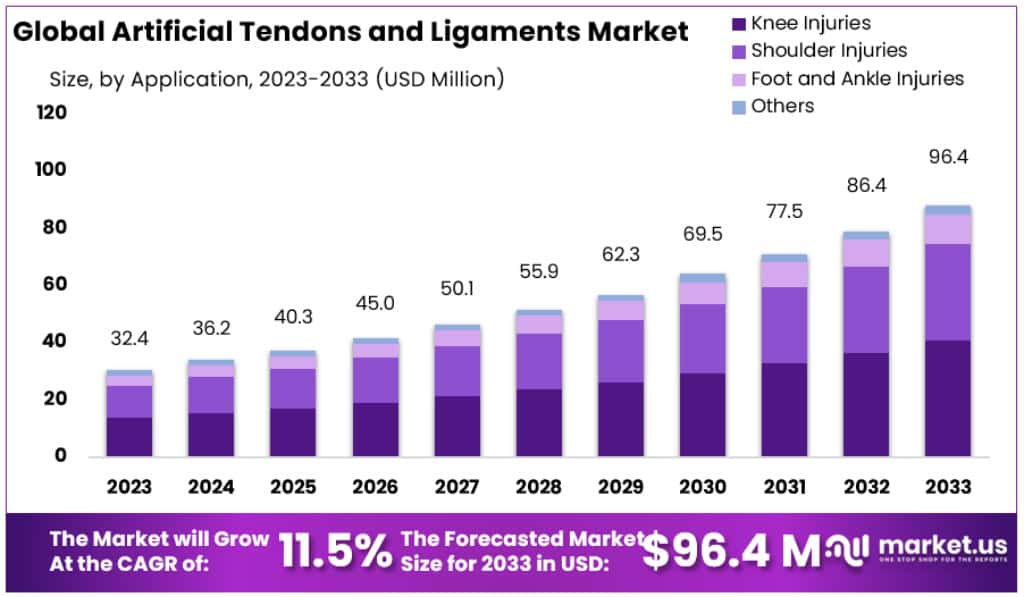

New York, NY – Jan 15, 2026 – The Global Artificial Tendons and Ligaments Market size is expected to be worth around USD 96.4 Million by 2033, from USD 32.4 Million in 2023, growing at a CAGR of 11.5% during the forecast period from 2024 to 2033.

Artificial tendons and ligaments are engineered medical implants designed to restore or replace damaged connective tissues that support joint movement and stability. Their development is driven by the rising incidence of sports injuries, trauma cases, age-related degeneration, and orthopedic disorders worldwide.

The basic formation of artificial tendons and ligaments involves the use of biocompatible materials that can replicate the strength, flexibility, and load-bearing properties of natural tissues. Commonly used materials include synthetic polymers such as polyethylene terephthalate (PET), polytetrafluoroethylene (PTFE), and biodegradable composites, as well as biological scaffolds derived from collagen or decellularized tissues. These materials are selected to ensure mechanical durability, minimal immune response, and long-term functionality.

Advanced manufacturing techniques such as fiber weaving, braiding, knitting, and 3D scaffold fabrication are applied to mimic the hierarchical structure of natural tendons and ligaments. Surface modification and coating technologies are increasingly used to improve cell adhesion and promote tissue integration. In many cases, bioactive agents or growth factors are incorporated to support healing and accelerate regeneration at the implantation site.

Artificial tendons and ligaments are primarily used in orthopedic and sports medicine procedures, including anterior cruciate ligament (ACL) reconstruction, shoulder stabilization, and tendon repair surgeries. Continuous research and development activities are focused on improving biomechanical performance, reducing failure rates, and enhancing biological compatibility.

Overall, the formation of artificial tendons and ligaments represents a critical advancement in regenerative medicine and orthopedic care, supporting improved patient outcomes and faster recovery timelines.

Key Takeaways

- Market Size: The Artificial Tendons and Ligaments Market is forecast to reach a valuation of USD 96.4 million by 2033, rising from USD 32.4 million in 2023.

- Market Growth: The market is anticipated to expand at a CAGR of 11.5% during the period from 2024 to 2033.

- Application Analysis: Knee injury applications accounted for the largest share in 2023, representing more than 42.5% of total market revenue.

- End-use Analysis: Hospitals and clinics emerged as the leading end users in 2023, capturing over 64% of the market share.

- Regional Analysis: Europe led the global market in 2023, with a market value of approximately USD 12.5 million.

- Technological Advancements: Ongoing developments in biomaterials and tissue engineering are improving product longevity, performance, and biocompatibility.

- Challenges and Opportunities: Elevated treatment costs and post-operative complications continue to restrain growth, while opportunities are being created through affordable innovations and expansion in emerging economies.

- Aging Population Impact: The growing global elderly population is contributing to increased demand, driven by a higher incidence of musculoskeletal disorders and injury-related conditions.

Regional Analysis

Europe is dominating the artificial tendons and ligaments market, with a market value of USD 12.5 million recorded in 2023. This dominance can be attributed to increasing consumer acceptance and improved awareness regarding the use of artificial grafts for the treatment of sports-related injuries. In addition, the strong presence of established regional manufacturers is supporting technological advancement and contributing to sustained market growth.

France, Germany, and the United Kingdom represent the largest markets within Europe and collectively accounted for more than 59% of total regional revenue in 2018. High participation rates in recreational and professional sports across the region have led to a growing number of sports injuries, particularly anterior cruciate ligament (ACL) ruptures. According to a 2017 *Health Economics Review* study, approximately 30,000 ACL rupture cases are treated annually in Germany alone, resulting in hospital costs estimated at USD 129.61 million.

The Asia-Pacific (APAC) region is projected to witness substantial market expansion during the forecast period. Growth in this region is supported by rising investments in research and development by global market players and increasing public awareness of artificial tendons, ligaments, and ACL reconstruction procedures. China and India are expected to register rapid growth, while Australia and Japan represent comparatively mature markets. Despite widespread use of LARS artificial ligaments in Europe and Canada, regulatory approval in the United States remains pending.

Emerging Trends

- Biomimetic Scaffold Development: Recent progress has focused on the design of scaffolds that closely replicate the hierarchical structure of native tendons and ligaments. These scaffolds, commonly fabricated using fiber-reinforced hydrogels, provide enhanced mechanical integrity while supporting collagen fiber alignment and tissue maturation. Such designs are increasingly aligned with the body’s natural biological and biomechanical responses.

- Integration of Stem Cell Technologies: The use of human induced pluripotent stem cells (hiPSCs) has demonstrated significant potential in tendon tissue engineering. By inducing the expression of tendon-specific transcription factors such as Mohawk (Mkx) and applying controlled mechanical stimulation during in-vitro cultivation, engineered tissues have been shown to exhibit structural and functional characteristics comparable to native tendons, supporting future regenerative therapy applications.

- Advancement of Smart Hydrogel Systems: Smart hydrogels are being developed to overcome persistent challenges in tendon and ligament regeneration. These materials are engineered to respond dynamically to physiological conditions, thereby promoting cell adhesion, proliferation, and extracellular matrix formation. As a result, improved tissue integration and accelerated healing outcomes are being reported.

Key Use Cases

- Management of Sports-Related Injuries: Tendon and ligament injuries, including anterior cruciate ligament (ACL) tears, are prevalent among athletes. Synthetic and bioengineered scaffolds are increasingly utilized to support tissue regeneration, with the objective of reducing recovery periods and enhancing functional restoration.

- Treatment of Degenerative Tendon Disorders: In chronic conditions such as tendinopathy, where progressive tissue degeneration occurs, artificial tendon constructs can provide mechanical reinforcement and stimulate biological repair processes, contributing to improved patient mobility and quality of life.

- Tendon and Ligament Surgical Reconstruction: For patients requiring reconstructive surgery due to severe tendon or ligament rupture, artificial grafts present a viable alternative to autografts and allografts. This approach reduces donor-site complications and minimizes the risk of immune-related adverse responses.

Frequently Asked Questions on Artificial Tendons and Ligaments

- What are artificial tendons and ligaments?

Artificial tendons and ligaments are biomedical implants designed to replace or reinforce damaged connective tissues. They restore joint stability and mobility by mimicking natural tensile strength, elasticity, and load-bearing behavior of human tendons and ligaments. - In which medical conditions are artificial tendons and ligaments used?

They are commonly used in orthopedic and sports medicine surgeries, including anterior cruciate ligament reconstruction, Achilles tendon repair, and severe trauma cases. Usage is considered when autografts or allografts are unsuitable or limited. - What materials are used to manufacture artificial tendons and ligaments?

Artificial tendons and ligaments are typically manufactured from polymers such as polyethylene terephthalate, polytetrafluoroethylene, or polyester fibers. These materials are selected for high strength, fatigue resistance, biocompatibility, and long-term mechanical stability. - What are the key benefits and risks associated with artificial tendons and ligaments?

Key benefits include reduced surgery time, consistent quality, and elimination of donor-site morbidity. However, risks such as infection, implant loosening, and long-term wear exist, requiring careful patient selection and post-surgical monitoring. - How long do artificial tendons and ligaments typically last?

The lifespan of artificial tendons and ligaments varies by material and patient activity. Many devices demonstrate functional durability for ten to twenty years, although long-term outcomes depend on surgical technique, rehabilitation quality, and biomechanical loading. - What are the major factors driving market growth?

Market growth is primarily driven by rising sports injuries, increasing geriatric population, and higher incidence of orthopedic disorders. Advancements in minimally invasive surgery and improved implant performance further support sustained demand across developed and emerging regions. - What is the future outlook for the artificial tendons and ligaments market?

The market outlook remains cautiously optimistic, supported by continuous R&D investment and growing acceptance of synthetic grafts. Emerging economies are expected to offer attractive growth opportunities as healthcare infrastructure improves and access to advanced orthopedic care expands.

Conclusion

In conclusion, artificial tendons and ligaments represent a significant advancement in orthopedic and regenerative medicine, addressing the growing burden of sports injuries, trauma, and age-related musculoskeletal disorders. The market is being supported by continuous innovation in biomaterials, scaffold design, and tissue engineering technologies, which are improving biomechanical performance and biological integration.

Strong demand from knee injury and hospital-based applications, along with Europe’s established adoption, underpins current growth. While cost and post-operative risks remain challenges, expanding awareness, aging populations, and technological progress are expected to sustain long-term market expansion globally.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)